What Li Auto (LI)'s Softer June Deliveries and New L8 Launch Mean For Shareholders

LI Auto LI | 0.00 |

- In June 2026, Li Auto Inc. reported deliveries of 30,895 vehicles, bringing cumulative deliveries to 1.73 billion since inception, while also launching the new Li L8 flagship SUV in Ultra and Livis trims priced at RMB 369,800 and RMB 429,800 in late June.

- The combination of softer June volumes, fresh Li L8 orders still ramping, and an internal restructuring to speed product decisions raises questions about how effectively Li Auto can balance heavy technology investment with consistent execution in China’s crowded new energy vehicle market.

- We’ll now examine how June’s softer deliveries, despite the Li L8 launch, reshape Li Auto’s existing investment narrative and key assumptions.

We've uncovered the 7 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Li Auto Investment Narrative Recap

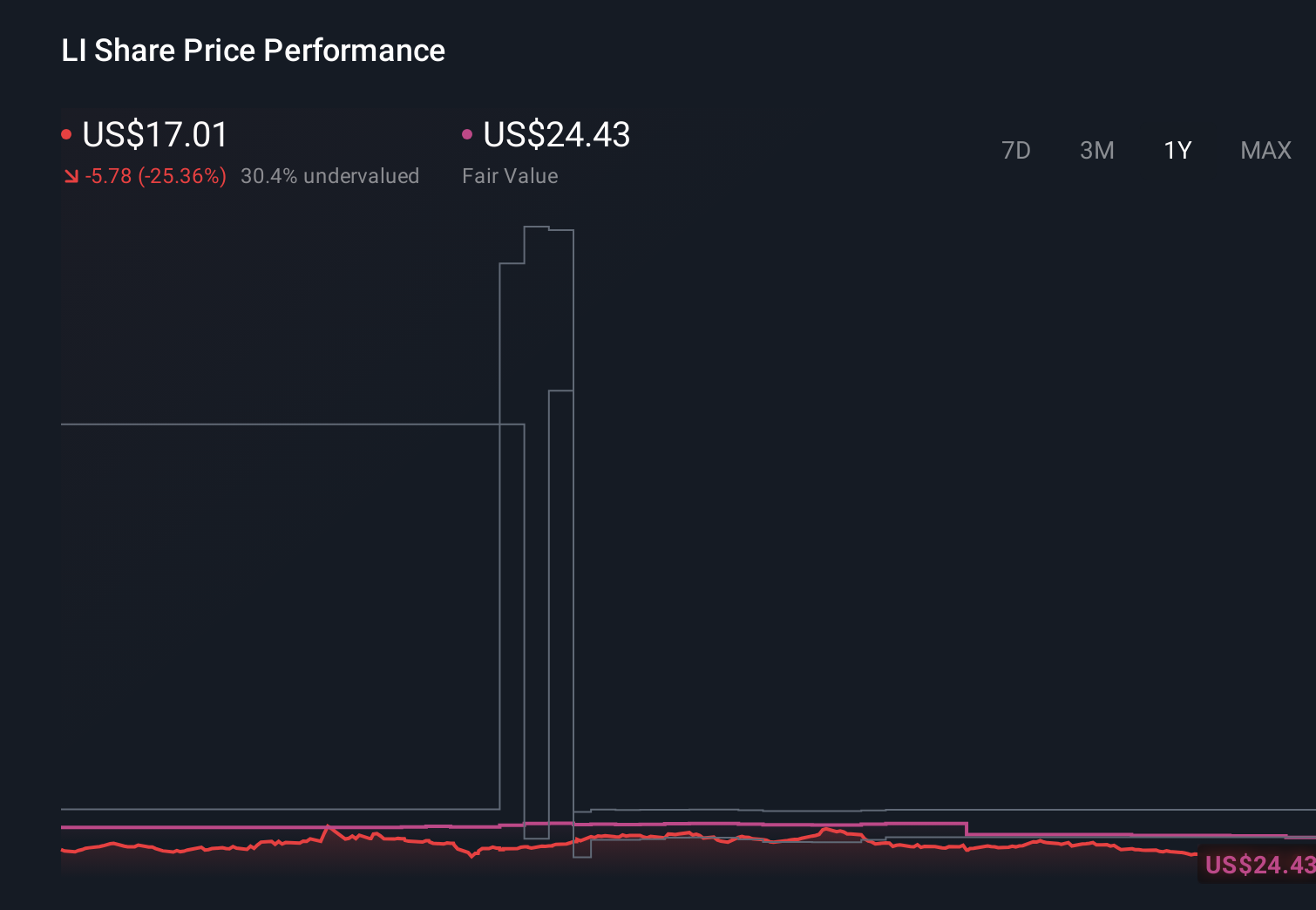

To own Li Auto today, you need to believe that its heavy spending on AI, BEVs, and charging can translate into sustainable demand and eventual profitability, despite recent share price weakness. June’s softer 30,895 deliveries, coming just as Li L8 launched, put more focus on the near term catalyst of stabilizing volumes and the key risk that high R&D and capex may outpace the company’s ability to grow revenue and protect margins. The June data meaningfully sharpens that tension.

Among recent updates, the most relevant here is Li Auto’s Q2 2026 guidance for a year on year decline in deliveries and revenue, which now sits against an even weaker June. When you pair that with the organizational restructuring to speed product decisions, it gives context for why execution around launches like the Li L8 matters so much to the existing catalyst of scaling BEVs and intelligent driving services without further eroding profitability.

Yet beneath the product launches and AI story, investors also need to be aware of rising technology and regulatory costs that could...

Li Auto's narrative projects CN¥170.4 billion revenue and CN¥8.0 billion earnings by 2029.

Uncover how Li Auto's forecasts yield a $21.18 fair value, a 76% upside to its current price.

Exploring Other Perspectives

Compared with the baseline view, the most bearish analysts were already assuming flat revenue near CN¥111.7 billion and only CN¥680.6 million in 2029 earnings, which frames June’s softer deliveries and rising regulatory compliance costs as potentially more concerning and shows how far opinions can differ before this latest news is fully reflected.

Explore 6 other fair value estimates on Li Auto - why the stock might be worth over 2x more than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Li Auto research is our analysis highlighting 2 key rewards that could impact your investment decision.

- Our free Li Auto research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Li Auto's overall financial health at a glance.

No Opportunity In Li Auto?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Find 44 companies with promising cash flow potential yet trading below their fair value.

- Uncover the next big thing with 20 elite penny stocks that balance risk and reward.

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.