What Lumentum Holdings (LITE)'s AI-Fueled Q3 Beat and NVIDIA Deal Means For Shareholders

Lumentum Holdings, Inc. LITE | 0.00 |

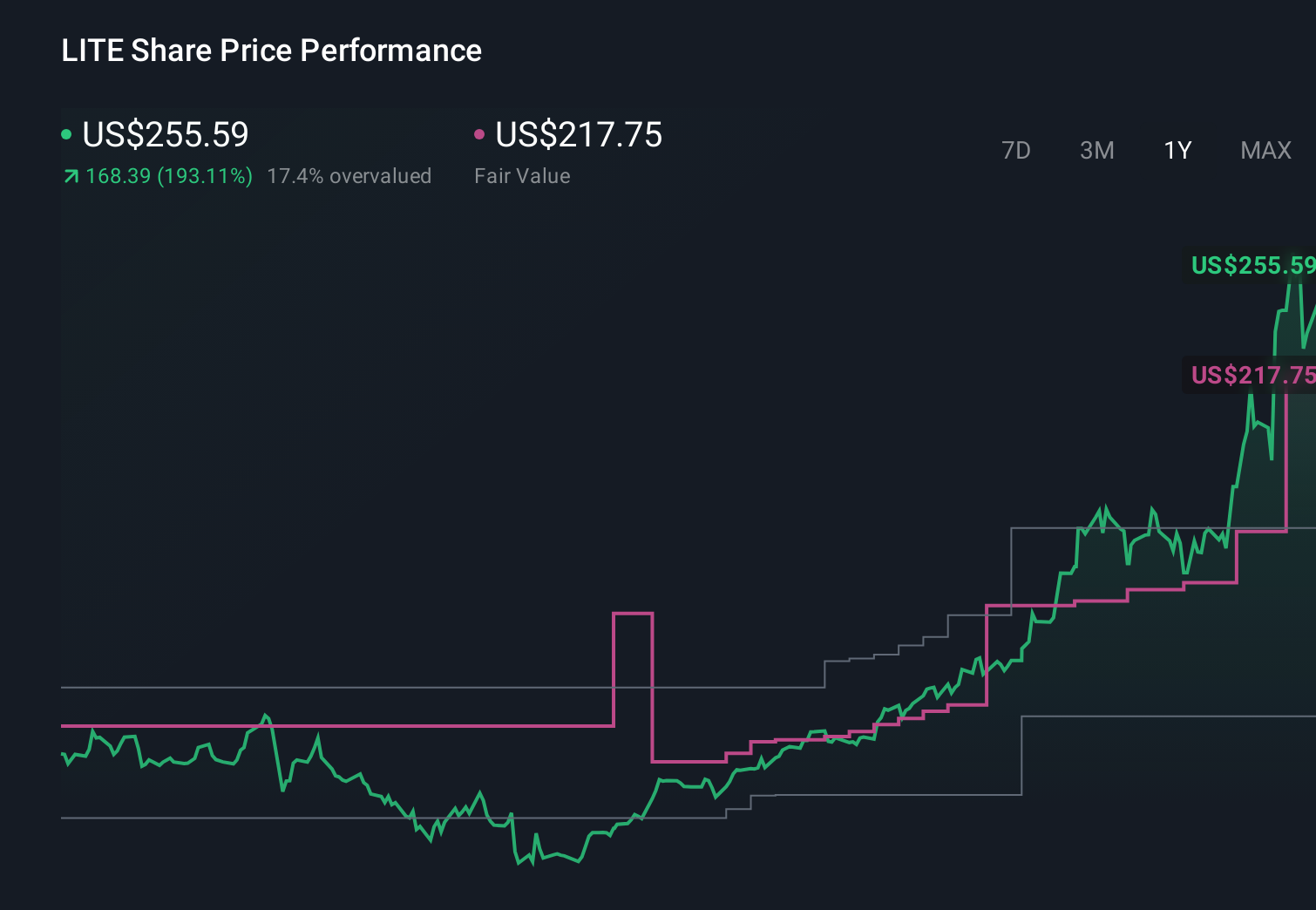

- Lumentum Holdings Inc. reported past fiscal third-quarter 2026 results with sales rising to US$808.4 million and net income to US$144.2 million, alongside strong guidance calling for fourth-quarter net revenue between US$960 million and US$1.01 billion.

- The surge in profitability was driven largely by demand for AI and cloud-related optical components, supported by expanded manufacturing capacity and a multiyear US$2.00 billion preferred equity investment and supply agreement with NVIDIA.

- Next, we'll examine how Lumentum's strong AI-driven revenue guidance and capacity expansion plans influence its existing investment narrative.

Find 51 companies with promising cash flow potential yet trading below their fair value.

Lumentum Holdings Investment Narrative Recap

To own Lumentum today, you need to believe its AI and cloud optics business can offset telecom softness while it executes on aggressive capacity expansion and manages customer concentration. The latest Q3 beat and strong Q4 revenue guidance keep the main near term catalyst intact: sustained AI hardware demand. However, they also highlight the biggest current risk, which is whether Lumentum can scale manufacturing fast enough without eroding margins or overextending its balance sheet.

The most relevant development here is NVIDIA’s multi‑year US$2.0 billion preferred equity investment and supply agreement, which underpins Lumentum’s AI optics positioning just as demand is running ahead of available capacity. That deal, alongside the new Greensboro, North Carolina fab, directly connects the upbeat guidance to a bigger capacity and product roadmap story, but it also tightens Lumentum’s dependence on a small group of hyperscale buyers for future growth.

Yet even with this momentum, investors should be aware that heavy reliance on a handful of hyperscale customers means that any shift in their ordering patterns could...

Lumentum Holdings' narrative projects $9.3 billion revenue and $2.9 billion earnings by 2029. This requires 64.1% yearly revenue growth and about a $2.6 billion earnings increase from $251.6 million today.

Uncover how Lumentum Holdings' forecasts yield a $904.89 fair value, in line with its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already projecting revenue near US$10.9 billion and earnings of about US$4.1 billion by 2029, assuming Lumentum’s AI optics capacity constraints simply ease over time, while also downplaying how sharply customer concentration could cut both ways; with results and guidance now in hand, you can see how their bullish view could strengthen or be tested depending on how you weigh that same risk.

Explore 11 other fair value estimates on Lumentum Holdings - why the stock might be worth as much as 79% more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Lumentum Holdings research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Lumentum Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Lumentum Holdings' overall financial health at a glance.

Interested In Other Possibilities?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Uncover the next big thing with 25 elite penny stocks that balance risk and reward.

- This technology could replace computers: discover 27 stocks that are working to make quantum computing a reality.

- The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.