What Marqeta (MQ)'s In-Line Revenue Growth And Earnings Report Means For Shareholders

Marqeta, Inc. MQ | 0.00 |

- Payment technology company Marqeta (NASDAQ: MQ) recently reported earnings after the bell, following market expectations for around 18.2% year-on-year revenue growth, roughly in line with the prior year’s pace.

- Investors have been particularly focused on Marqeta’s history of outperforming Wall Street forecasts, which has heightened interest in how this latest report compares with past surprises.

- We’ll now examine how anticipation around Marqeta’s expected revenue growth and earnings surprise potential may influence the company’s broader investment narrative.

AI is about to change healthcare. These 35 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Marqeta Investment Narrative Recap

To own Marqeta, you need to believe that its open API card issuing platform can keep attracting large fintech and embedded finance customers, while gradually improving profitability. The upcoming earnings, with expectations for about 18.2% year on year revenue growth, are a key short term catalyst for sentiment, but they do not fundamentally change the biggest risk right now, which remains Marqeta’s reliance on a handful of major clients for a large share of revenue.

The most relevant recent announcement to this earnings setup is Marqeta’s guidance on 2026 net revenue and gross profit growth in the low-teens range. This guidance frames how investors may interpret any upside or downside to the current quarter’s expected growth. It also sits alongside the company’s ongoing share buybacks and continued investment in risk tools and platform capabilities, which many shareholders watch closely as potential support for the growth and margin story if revenue expectations shift.

However, against that backdrop, investors should also be aware of the concentration risk if a key customer were to change course...

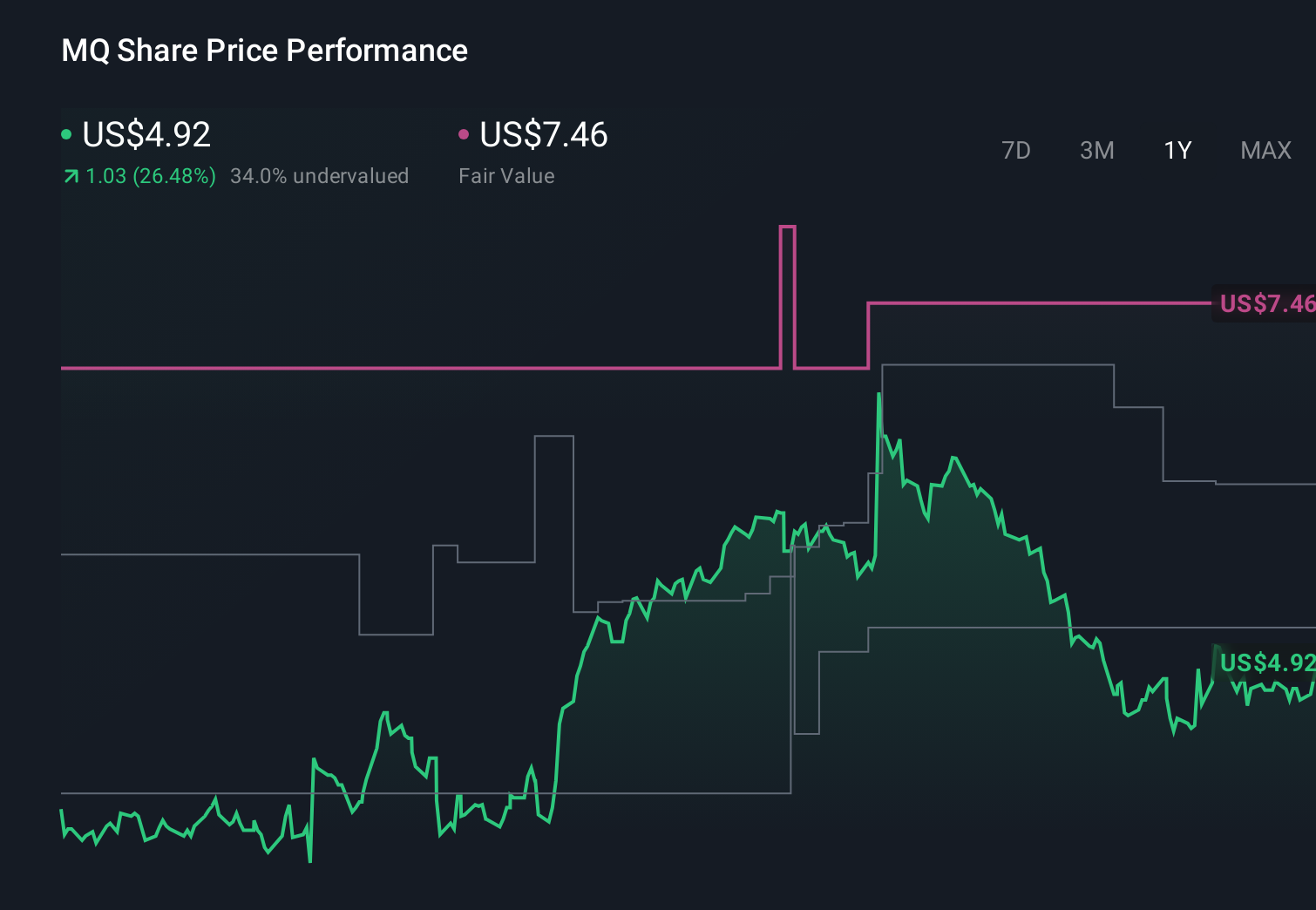

Marqeta's narrative projects $955.7 million revenue and $59.4 million earnings by 2029. This requires 15.2% yearly revenue growth and a $73.3 million earnings increase from -$13.9 million today.

Uncover how Marqeta's forecasts yield a $5.18 fair value, a 16% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were assuming Marqeta could reach about US$1.0 billion of revenue and US$194.5 million of earnings by 2028, which is far more upbeat than the baseline view tied to upcoming earnings, especially given the ongoing concern about heavy reliance on a few major clients.

Explore 4 other fair value estimates on Marqeta - why the stock might be worth as much as 52% more than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Marqeta research is our analysis highlighting 1 key reward that could impact your investment decision.

- Our free Marqeta research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Marqeta's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

- We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Invest in the nuclear renaissance through our list of 91 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.