What NPK International (NPKI)'s Shift From Russell Value To Growth Indexes Means For Shareholders

NPK International Inc. NPKI | 0.00 |

- On 27 June 2026, NPK International Inc. (NYSE:NPKI) was reclassified across the Russell index family, joining several growth-focused benchmarks while exiting a range of value-oriented indexes, including the Russell 2000 Value and Russell 3000 Value benchmarks.

- This broad shift from value to growth classifications signals that index providers now see NPK International’s profile as more aligned with growth characteristics, which can influence how both passive and active investors categorize and assess the company.

- We’ll now examine how NPK International’s broad migration into growth-oriented Russell indexes could reshape its investment narrative for investors.

Outshine the giants: these 15 early-stage AI stocks could fund your retirement.

NPK International Investment Narrative Recap

To own NPK International, you need to believe its rental focused, infrastructure and utility oriented model can justify a premium valuation despite exposure to project timing and sector cyclicality. The broad shift into growth focused Russell indexes may support trading liquidity and visibility, but does not materially change the near term dependence on large project pipelines or the risk that more volatile product sales and elevated SG&A could pressure margins if demand cools.

Among recent announcements, the raised full year 2026 revenue guidance to US$310 million to US$325 million stands out alongside the Russell reclassification, because it underpins the current growth oriented narrative while also increasing the stakes if infrastructure related or utility projects are delayed, which remains one of the core execution risks around NPK International’s enlarged rental fleet and concentrated customer exposure.

Yet behind NPK International’s growth label, one risk investors should be aware of is the company’s reliance on large utility and infrastructure customers, where...

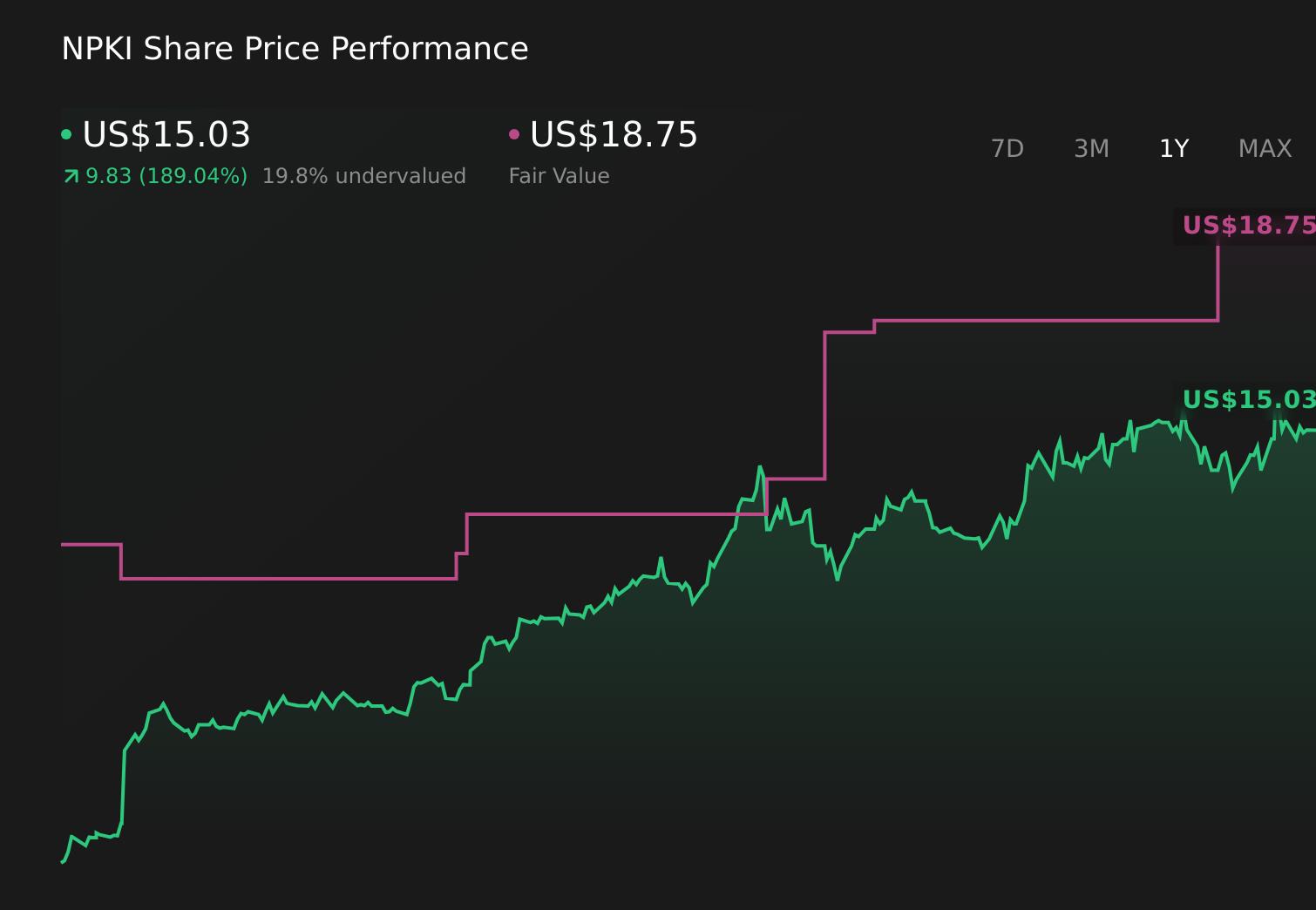

NPK International's narrative projects $405.8 million revenue and $70.0 million earnings by 2029.

Uncover how NPK International's forecasts yield a $20.33 fair value, a 28% upside to its current price.

Exploring Other Perspectives

Two fair value estimates from the Simply Wall St Community cluster between US$18.45 and US$20.33 per share, underlining how differently individual investors can assess the same stock. Against this backdrop, the shift of NPK International into multiple growth oriented Russell indexes may influence how you weigh its project timing risk and exposure to infrastructure cycles, so it is worth exploring several alternative viewpoints before forming your own stance.

Explore 2 other fair value estimates on NPK International - why the stock might be worth as much as 28% more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your NPK International research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free NPK International research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate NPK International's overall financial health at a glance.

Seeking Other Investments?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Find 44 companies with promising cash flow potential yet trading below their fair value.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.