What Philip Morris International (PM)'s Smoke‑Free Pivot and Dividend Move Means For Shareholders

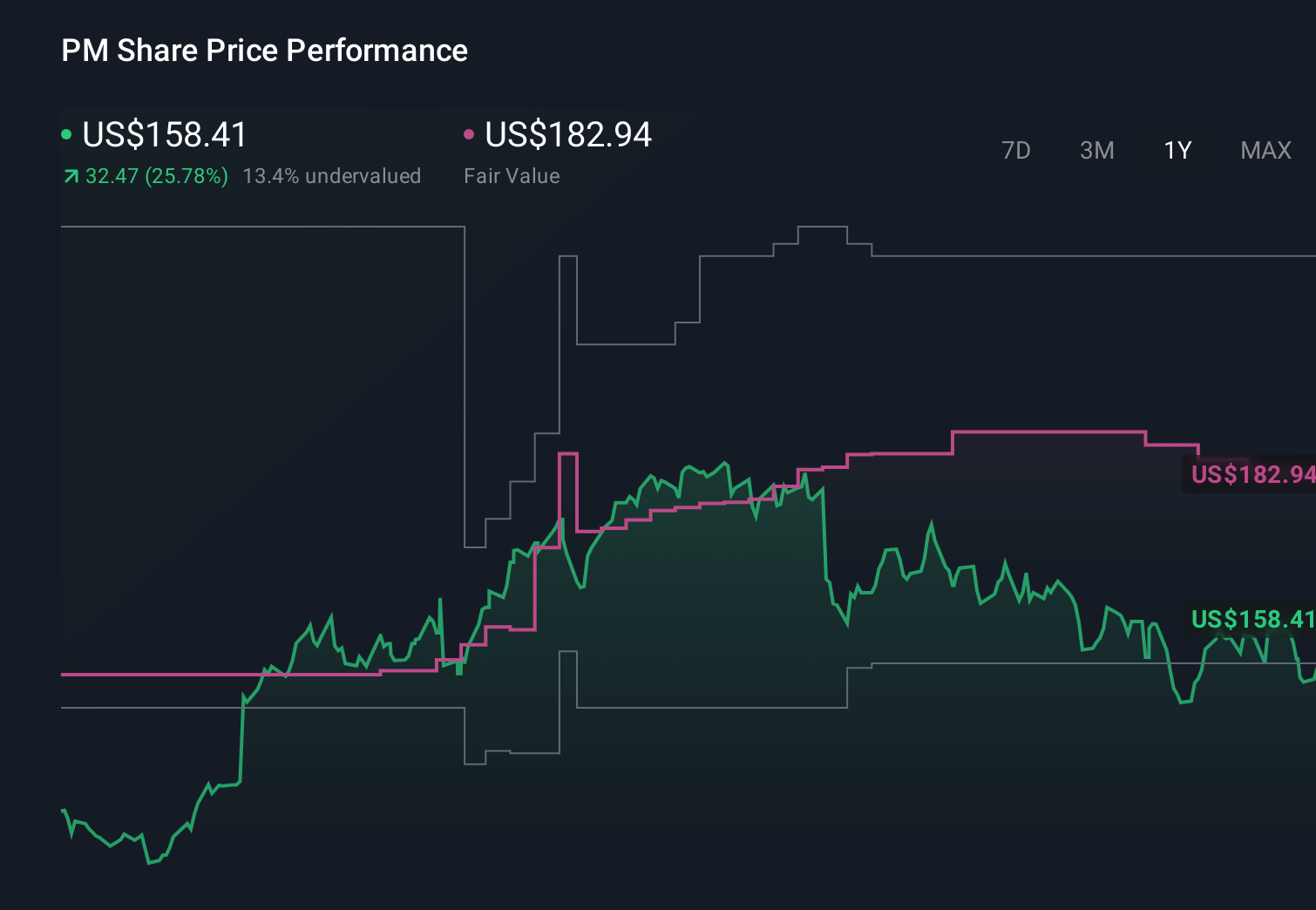

Philip Morris International Inc. PM | 158.10 | +0.49% |

- In recent months, Philip Morris International has been highlighted by Fundsmith Equity Fund and other commentators for its push into reduced-risk products such as IQOS heat‑not‑burn devices and nicotine pouches, while also declaring a regular quarterly dividend ahead of its fiscal Q4 2025 earnings release.

- An interesting angle is how institutional recognition of its smoke‑free innovation is coinciding with ongoing investment and regulatory scrutiny around the pace and profitability of its shift away from traditional cigarettes.

- With Philip Morris International’s smoke‑free innovation now in the spotlight, we’ll examine how this emphasis reshapes its existing investment narrative.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

Philip Morris International Investment Narrative Recap

To own Philip Morris International, you need to believe its smoke free products can more than compensate for declining cigarette volumes and regulatory pressure. The latest recognition from Fundsmith and others reinforces that IQOS and nicotine pouches are central to that thesis, but it does not materially change the near term catalyst of execution on smoke free growth or the key risk that regulation, taxes, and illicit trade slow the transition or squeeze margins.

The most immediately relevant update is the December 12 decision to declare a regular quarterly dividend of US$1.47 per share ahead of Q4 2025 results. That move underlines PMI’s focus on cash returns while it continues to invest heavily in smoke free innovation, which matters if you are weighing the dividend appeal against short term earnings sensitivity to regulation, currency swings, and the pace of reduced risk product adoption.

Yet beneath the smoke free story, one regulation related issue could still catch investors off guard and it is something you should be aware of...

Philip Morris International's narrative projects $49.4 billion revenue and $14.5 billion earnings by 2028. This requires 8.2% yearly revenue growth and a $6.3 billion earnings increase from $8.2 billion today.

Uncover how Philip Morris International's forecasts yield a $182.94 fair value, a 11% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts, who saw PMI’s 2028 revenue reaching about US$53.2 billion and earnings around US$15.7 billion, are effectively telling you that risks like tighter advertising bans or flavor restrictions may be less limiting than consensus assumes, but this new focus on smoke free profitability and regulation could challenge that view and is a reminder that informed investors look at several competing narratives before deciding what they believe.

Explore 11 other fair value estimates on Philip Morris International - why the stock might be worth as much as 30% more than the current price!

Build Your Own Philip Morris International Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Philip Morris International research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Philip Morris International research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Philip Morris International's overall financial health at a glance.

Ready For A Different Approach?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- We've found 12 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Find companies with promising cash flow potential yet trading below their fair value.

- Outshine the giants: these 26 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.