What RTX (RTX)'s NATO Electronic Warfare Contract Win Means For Shareholders

RAYTHEON TECHNOLOGIES CORPORATION RTX | 0.00 |

- Recently, Collins Aerospace, a unit of RTX Corporation, announced it was awarded a contract by NATO to provide its Electronic Warfare Planning and Battle Management (EWPBM) solution, enhancing the alliance’s electromagnetic warfare capabilities through advanced situational awareness software.

- This contract win underlines RTX’s growing presence in the international defense technology sector and supports its role in supplying critical defense solutions for multi-domain operations.

- We’ll examine how securing this NATO contract strengthens RTX’s investment narrative through expanded defense technology opportunities and international market visibility.

Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

RTX Investment Narrative Recap

To back RTX as a shareholder, it helps to believe that the company’s diversified defense and aerospace portfolio can turn robust contract wins and global security demand into recurring revenues, while successfully navigating risks tied to government budgets and operational challenges. The recent Collins Aerospace NATO contract showcases RTX's scale and defense technology ambitions but does not materially shift the near-term focus, which remains on reliability improvements and margin stability in its jet engine programs. One announcement with clear relevance is the NATO agreement itself. By providing advanced electronic warfare solutions, RTX expands its international defense technology presence, a core growth catalyst given the sector’s focus on cybersecurity and multi-domain operations, while reinforcing its exposure to the sometimes volatile defense procurement cycle. In contrast, some recent incidents illustrate that investors shouldn’t lose sight of operational risks such as...

RTX's outlook anticipates $97.7 billion in revenue and $8.9 billion in earnings by 2028. This assumes 5.3% annual revenue growth and a $2.8 billion increase in earnings from the current $6.1 billion.

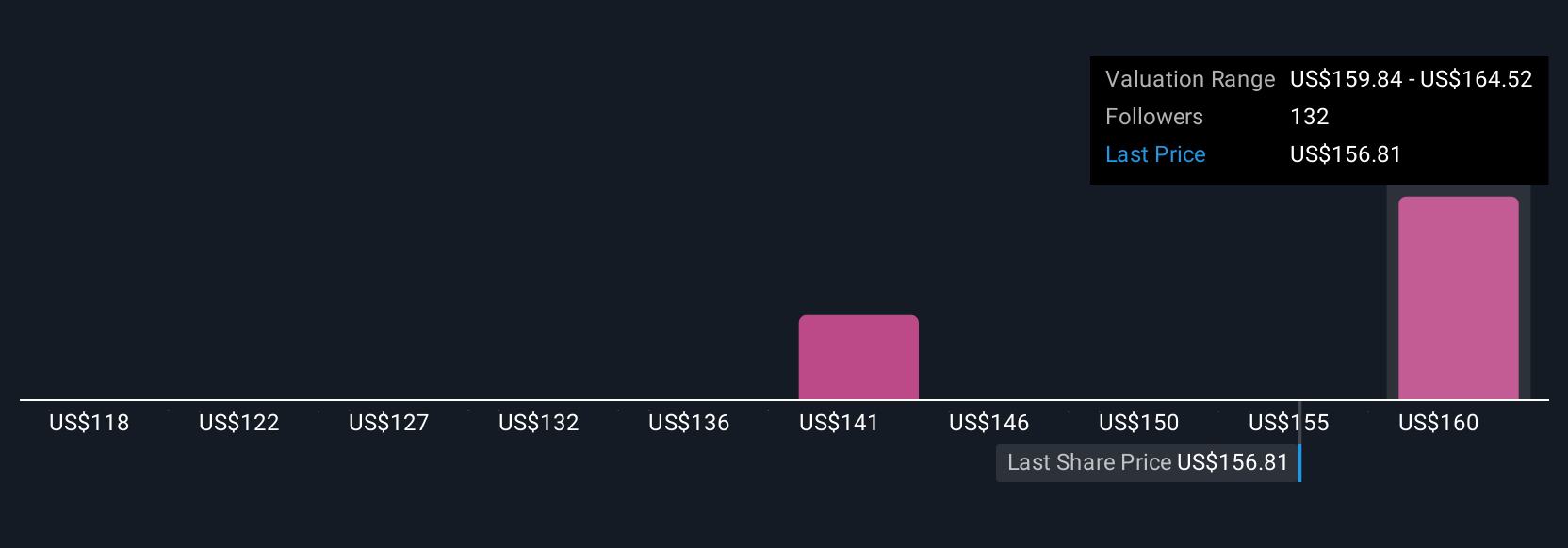

Uncover how RTX's forecasts yield a $164.58 fair value, a 3% upside to its current price.

Exploring Other Perspectives

Private fair value estimates from seven Simply Wall St Community members range from US$117.66 to US$164.58 per share. While global defense contracts support RTX’s growth story, participants suggest a broad spectrum of views about RTX’s prospects, your perspective may differ as well.

Explore 7 other fair value estimates on RTX - why the stock might be worth 26% less than the current price!

Build Your Own RTX Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your RTX research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free RTX research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate RTX's overall financial health at a glance.

Contemplating Other Strategies?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- These 11 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- We've found 19 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 25 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.