What Talen Energy (TLN)'s AWS Nuclear Deal and $4 Billion Refinancing Move Means For Shareholders

Talen Energy Corp TLN | 0.00 |

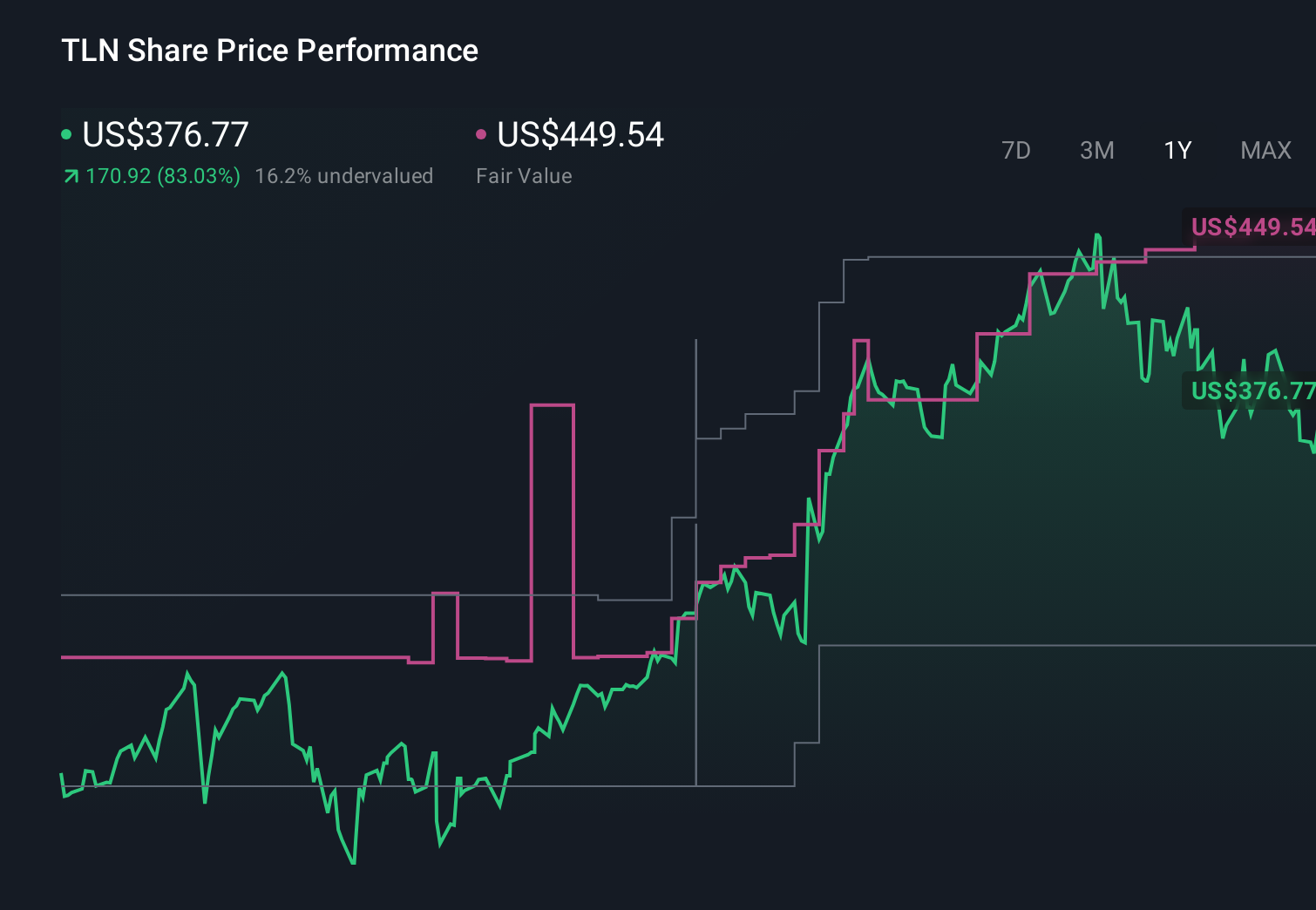

- Talen Energy’s subsidiary recently completed a private placement of US$4.00 billion in senior notes to help fund the acquisition of 2,451 megawatts of power capacity and redeem higher-interest debt due in 2030, while also expanding a 17-year agreement to supply up to 1,920 MW of carbon-free nuclear power to Amazon Web Services from its Susquehanna plant.

- This long-term AWS contract, expected to generate roughly US$18.00 billion in revenue, alongside debt refinancing and capacity growth, could reshape Talen’s revenue visibility and balance sheet profile for years to come.

- Next, we’ll examine how this expanded long-term AWS nuclear agreement may influence Talen Energy’s investment narrative and future cash flows.

The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Talen Energy Investment Narrative Recap

To own Talen Energy, you need to believe it can convert rising data center power demand into steadier, long-duration cash flows while managing fossil-heavy assets and high leverage. The expanded 17‑year AWS nuclear contract and US$4.00 billion notes issue directly touch both the key near term catalyst (contracted, carbon free revenues) and the biggest risk (balance sheet strain), by boosting long term visibility but also increasing gross debt and execution pressure around integration and refinancing.

Within recent announcements, the agreement to acquire roughly 2.6 GW of gas generation from Energy Capital Partners is especially relevant here. Combined with the new 2,451 MW acquisition funded by the notes, it deepens Talen’s exposure to fossil-fired capacity at the same time AWS is locking in carbon free supply, sharpening the contrast between the clean energy catalyst and the risk that future policy or market shifts could challenge these gas assets and the deleveraging plan.

Yet beneath this stronger AWS anchor, investors should still be aware that Talen’s growing dependence on fossil generation leaves it exposed if decarbonization policies accelerate and...

Talen Energy's narrative projects $4.2 billion revenue and $1.1 billion earnings by 2028.

Uncover how Talen Energy's forecasts yield a $462.97 fair value, a 32% upside to its current price.

Exploring Other Perspectives

While consensus focuses on balance sheet risk and fossil exposure, the most optimistic analysts see the AWS link and Susquehanna upgrades as a springboard, with some once projecting revenue near US$6.3 billion and earnings around US$1.6 billion by 2029, so you should weigh how this new contract and financing might shift both that bullish scenario and the concerns about centralized, fossil heavy generation.

Explore 6 other fair value estimates on Talen Energy - why the stock might be worth over 2x more than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Talen Energy research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Talen Energy research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Talen Energy's overall financial health at a glance.

Seeking Other Investments?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 30 companies in the world exploring or producing it. Find the list for free.

- Outshine the giants: these 16 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.