What UnitedHealth Group (UNH)'s Upbeat 2026 Outlook and Margin Narrative Means For Shareholders

UnitedHealth Group Incorporated UNH | 0.00 |

- In recent weeks, UnitedHealth Group has attracted renewed attention after delivering stronger-than-expected first-quarter results and raising its full-year 2026 adjusted earnings outlook, prompting several major brokers to highlight improved margin prospects despite ongoing medical cost and regulatory pressures.

- At the same time, hedge fund interest and inclusion on select “high quality” and dividend-focused lists have underlined how investors view UnitedHealth’s scale, Medicare Advantage exposure and technology investments, such as AI-enabled cost controls, as central to its long-term role in the managed care industry.

- We’ll now examine how this upbeat earnings guidance and margin-recovery commentary may influence UnitedHealth Group’s existing investment narrative and risk profile.

Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

UnitedHealth Group Investment Narrative Recap

To own UnitedHealth Group, you need to believe its scale, Medicare Advantage footprint and Optum capabilities can still support attractive margins despite policy and medical cost pressures. The latest earnings beat and higher 2026 adjusted EPS guidance reinforce that margin recovery is the key near term catalyst, while the biggest current risk remains further shocks to medical costs or reimbursement in government programs. The recent news appears supportive of the narrative rather than changing it.

Among the recent developments, management’s move to lift full year 2026 adjusted EPS guidance to above US$18.25 per share is most relevant. It ties directly to broker upgrades that cite easing medical loss ratio pressures and confidence in returning toward target margins. For investors focused on near term catalysts, this guidance sits at the heart of the debate over whether UnitedHealth’s earnings power can improve without being undermined by the next round of regulatory or cost surprises.

But against this improved outlook, the risk of further Medicare Advantage rule changes is something investors should be aware of...

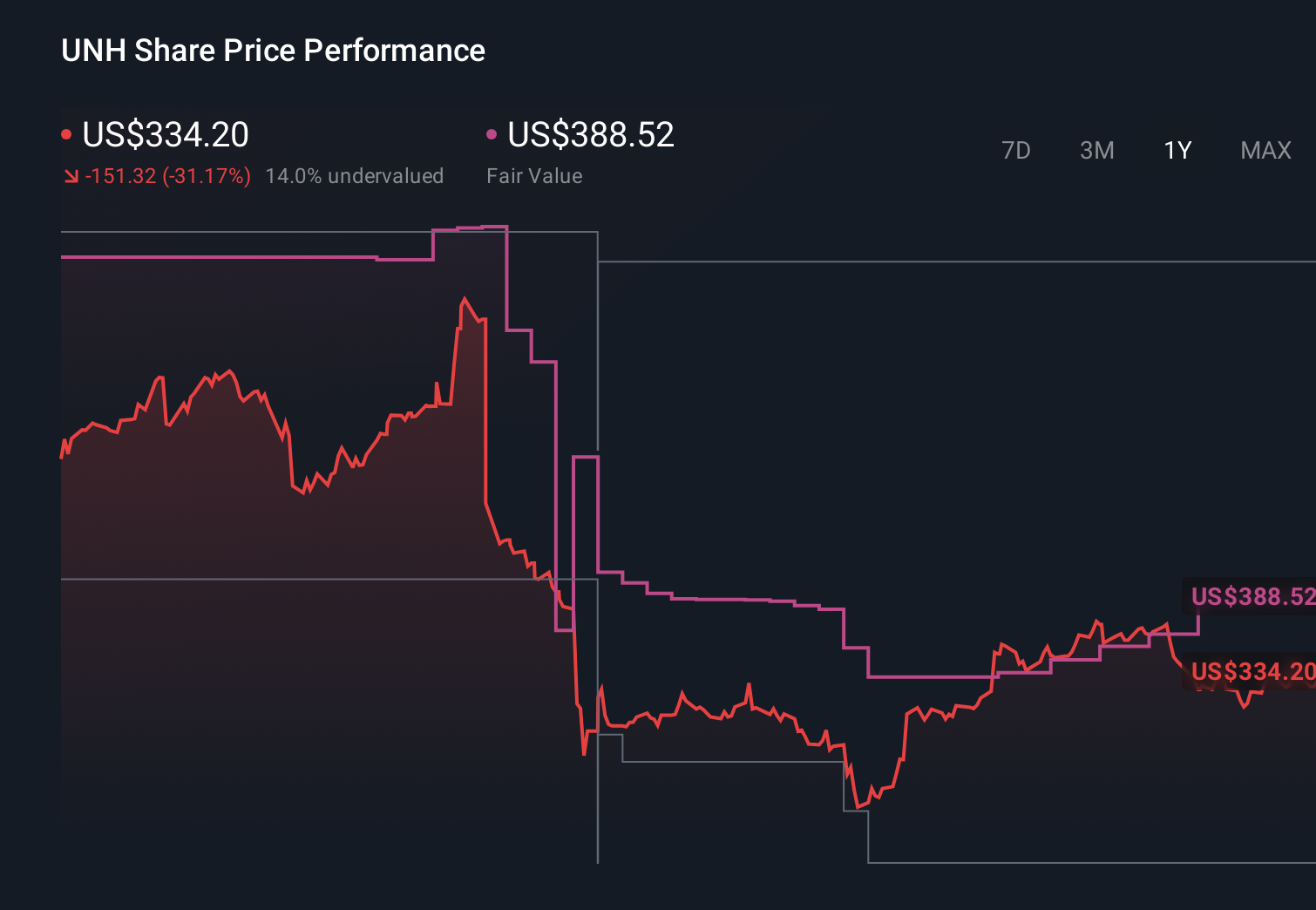

UnitedHealth Group's narrative projects $492.0 billion revenue and $21.1 billion earnings by 2029. This requires 3.0% yearly revenue growth and about a $9.1 billion earnings increase from $12.0 billion today.

Uncover how UnitedHealth Group's forecasts yield a $386.08 fair value, in line with its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were already cautious, assuming roughly flat revenue around US$460 billion and earnings of about US$20 billion by 2029, so if you are relying on margin recovery while worrying about government program risk, it is worth knowing that their more pessimistic narrative could shift again as this new guidance and regulatory backdrop evolve.

Explore 68 other fair value estimates on UnitedHealth Group - why the stock might be worth 21% less than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your UnitedHealth Group research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free UnitedHealth Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate UnitedHealth Group's overall financial health at a glance.

Looking For Alternative Opportunities?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Outshine the giants: these 13 early-stage AI stocks could fund your retirement.

- The future of work is here. Discover the 35 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- This technology could replace computers: discover 28 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.