What Ventas (VTR)'s Raised 2025 FFO Guidance and $600M Acquisition Mean for Shareholders

Ventas, Inc. VTR | 0.00 |

- Ventas, Inc. recently declared a quarterly dividend of US$0.48 per common share, payable on October 16, 2025, and presented at the BofA Securities 2025 Global Real Estate Conference in New York, featuring senior company leaders.

- Of particular note, Ventas raised its 2025 Funds From Operations (FFO) guidance and announced plans to acquire a US$600 million Long Island property, supporting its growth and portfolio expansion efforts.

- We'll examine how the raised FFO guidance and major property acquisition inform changes in Ventas' investment outlook.

Find companies with promising cash flow potential yet trading below their fair value.

Ventas Investment Narrative Recap

To be a shareholder in Ventas, Inc., you need to believe in the company’s ability to capitalize on demographic tailwinds, namely the aging population and sustained demand for senior housing and medical facilities. The recent dividend affirmation and raised FFO guidance reinforce the near-term growth catalyst of occupancy and revenue expansion, but the $600 million Long Island acquisition elevates execution risk, especially around achieving targeted integration and returns. At this stage, the news modestly emphasizes the balance between opportunity and risk rather than fundamentally shifting the risk profile.

Among the recent developments, Ventas’ announcement to acquire a US$600 million Long Island property is particularly relevant. This move supports its external growth strategy yet heightens execution and integration risk, the biggest potential headwind right now, as the company looks to deliver on revised upward FFO guidance and build on improved quarterly results. Despite the optimism, investors must also be mindful that an increased reliance on acquisitions can raise new challenges for…

Ventas’ outlook anticipates $6.9 billion in revenue and $443.6 million in earnings by 2028. Achieving these targets would require a 9.3% annual revenue growth rate and a $252.4 million increase in earnings from current levels of $191.2 million.

Uncover how Ventas' forecasts yield a $77.39 fair value, a 15% upside to its current price.

Exploring Other Perspectives

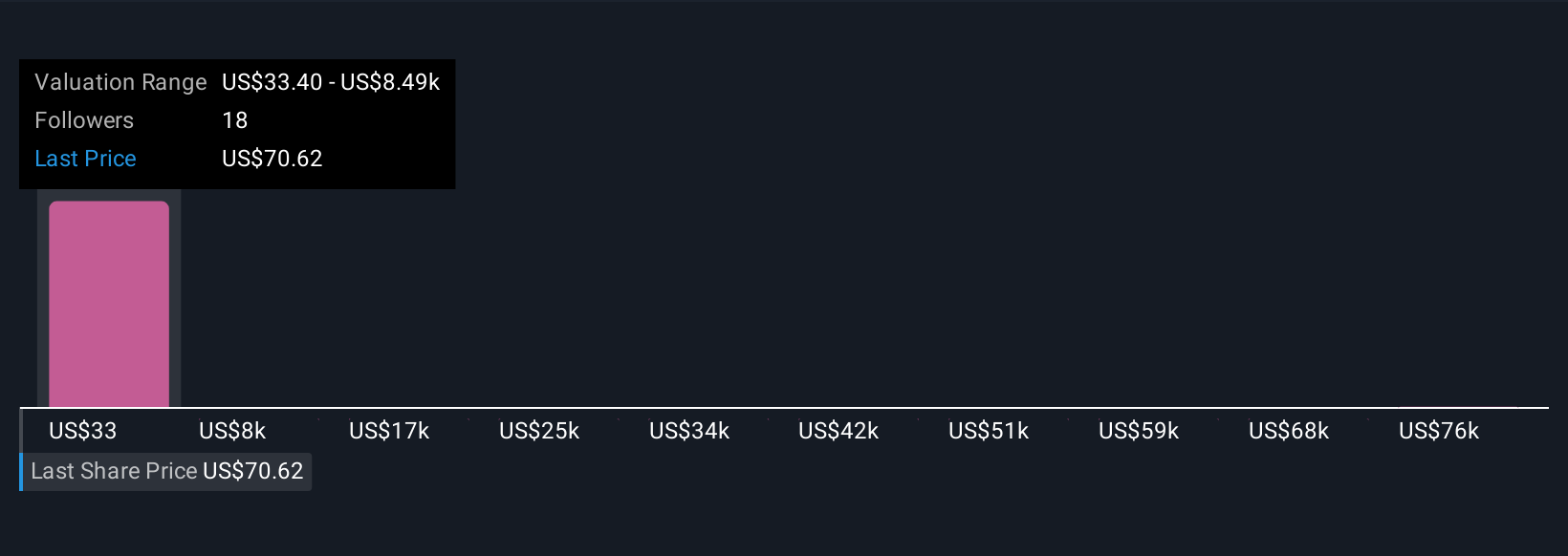

Simply Wall St Community members have published five fair value estimates for Ventas, ranging from US$33 to over US$84,000 per share. While the company’s external growth via acquisitions excites some, any setback in integration or operator performance could affect future returns, so exploring a range of market opinions is worthwhile.

Explore 5 other fair value estimates on Ventas - why the stock might be a potential multi-bagger!

Build Your Own Ventas Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Ventas research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Ventas research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Ventas' overall financial health at a glance.

Ready For A Different Approach?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- These 11 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 31 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.