What VinFast Auto (VFS)'s Global After-Sales Push Means For Shareholders

VinFast Auto VFS | 0.00 |

- In May 2026, VinFast expanded its global after-sales footprint by signing 29 new service MOUs and continued promoting its VF 9 and upgraded VF 8 EVs, highlighting long-range capability, family practicality, and extensive warranty support across key markets including Canada and Vietnam.

- This focus on service accessibility, app-enabled charging coverage, and long-duration warranties positions VinFast to compete on ownership experience as much as on vehicle hardware.

- We’ll now examine how VinFast’s push to build an extensive global after-sales network could influence its existing investment narrative and risks.

This technology could replace computers: discover 28 stocks that are working to make quantum computing a reality.

VinFast Auto Investment Narrative Recap

To own VinFast, you need to believe it can turn rapid EV volume growth and heavy upfront investment into a durable, service-led global brand despite ongoing losses, high cash burn and limited cash runway. The latest push to add 29 after-sales partners and highlight VF 9 and upgraded VF 8 ownership benefits supports the near term catalyst of improving customer perception but does not materially change the central risk around liquidity and persistent negative gross margins.

The April update showing 24,774 EVs delivered in Vietnam for the month and 78,458 year to date is the most relevant recent announcement here, because it underlines how much of VinFast’s story still rests on sustaining high domestic volumes while it spends heavily on international expansion and service coverage. That concentration keeps both the upside from scale and the downside from any demand wobble tightly linked to one market.

Yet behind the appeal of long warranties and growing service coverage, investors should be aware that VinFast’s heavy investment ahead of demand across multiple regions could...

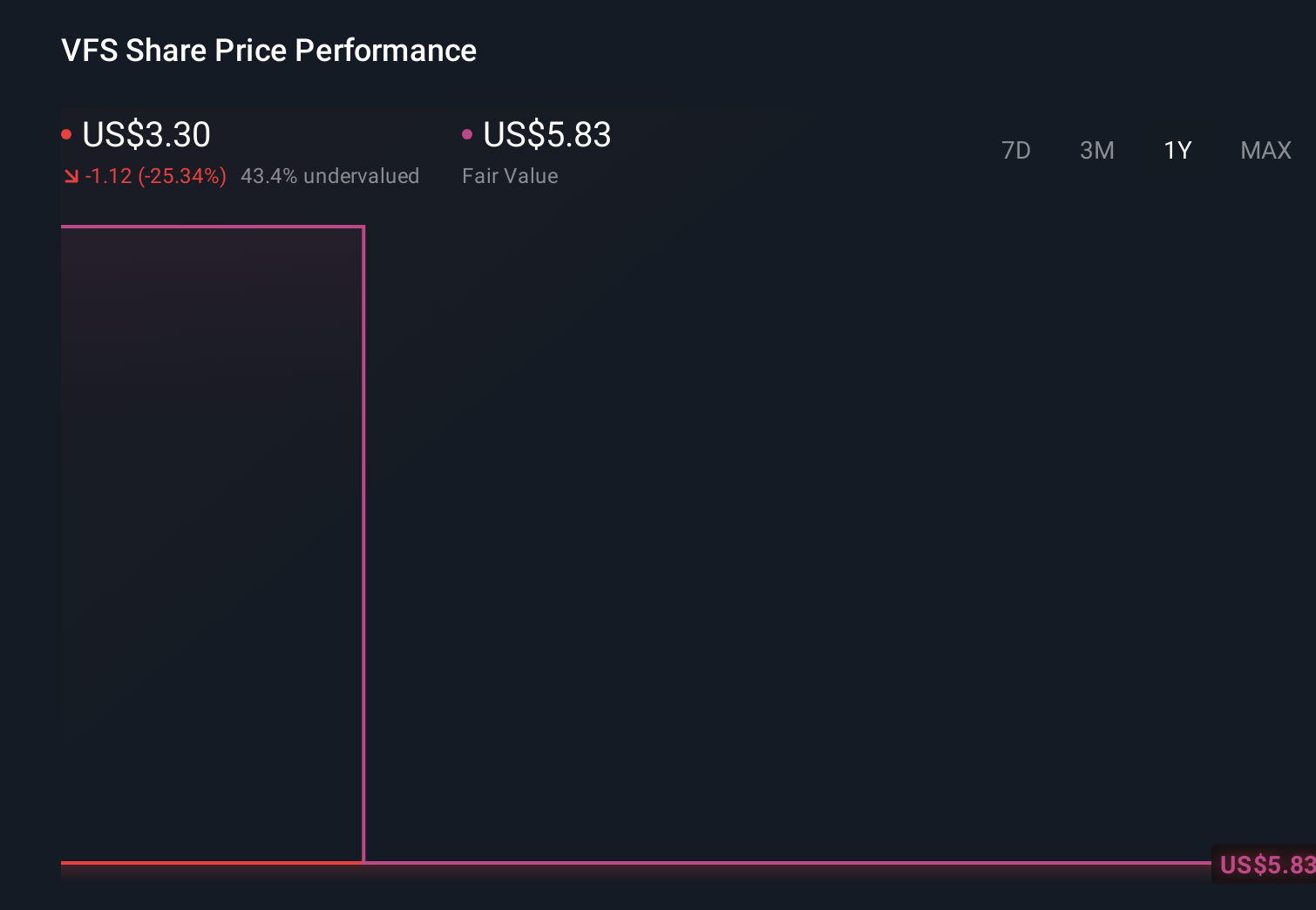

VinFast Auto's narrative projects ₫239006.9 billion in revenue and ₫5494.0 billion in earnings by 2029. This requires 38.3% yearly revenue growth and an earnings increase of about ₫102,536 billion from -₫97,041.9 billion today.

Uncover how VinFast Auto's forecasts yield a $6.30 fair value, a 76% upside to its current price.

Exploring Other Perspectives

While consensus already bakes in fast growth, the most pessimistic analysts were assuming revenue could still rise about 47% annually but with no profitability in sight, highlighting that even with news like the VF 9’s Canadian traction and VF 8 upgrades, you and those bearish forecasts about heavy investment ahead of demand may need to be revisited from very different starting points.

Explore 5 other fair value estimates on VinFast Auto - why the stock might be a potential multi-bagger!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your VinFast Auto research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free VinFast Auto research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate VinFast Auto's overall financial health at a glance.

Want Some Alternatives?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- The future of work is here. Discover the 35 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Rare earth metals are the new gold rush. Find out which 27 stocks are leading the charge.

- Uncover the next big thing with 25 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.