What Williams Companies (WMB)'s Fee-Based Midstream Strategy Amid Volatile Energy Markets Means For Shareholders

Williams Companies, Inc. WMB | 0.00 |

- Recently, commentary highlighted that Williams Companies and other midstream peers are benefiting from long-term, fee-based contracts that help steady revenues amid heightened energy-market volatility tied to geopolitical tensions.

- An important angle is how Williams’ focus on transporting and processing natural gas positions it to participate in growing clean energy demand while still relying on conventional infrastructure.

- Next, we’ll examine how this emphasis on fee-based midstream stability could influence Williams Companies’ existing investment narrative and risk profile.

Capitalize on the AI infrastructure supercycle with our selection of the 48 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Williams Companies Investment Narrative Recap

To own Williams Companies, you have to believe in the durability of fee-based, natural-gas infrastructure as a cornerstone of the U.S. energy mix. The recent focus on geopolitical volatility underscores why stable, long-term contracts can matter, but it does not fundamentally change the near term story: the key catalyst remains executing growth projects on time and on budget, while the biggest risk is that permitting or policy shifts slow expansion and raise the threat of future stranded assets.

In that context, the recent groundbreaking of the Northeast Supply Enhancement project stands out. Expanding Transco’s capacity into the constrained Northeast directly ties into Williams’ fee-based growth narrative, but it also sits at the intersection of regulatory and decarbonization risk. How efficiently Williams manages projects like NESE, amid shifting policy and ESG scrutiny, could shape both its cash flow stability and its exposure to long term volume and asset utilization risk.

Yet investors should also be aware that if permitting momentum stalls or energy transition policies accelerate, the resilience of those long term contracts could...

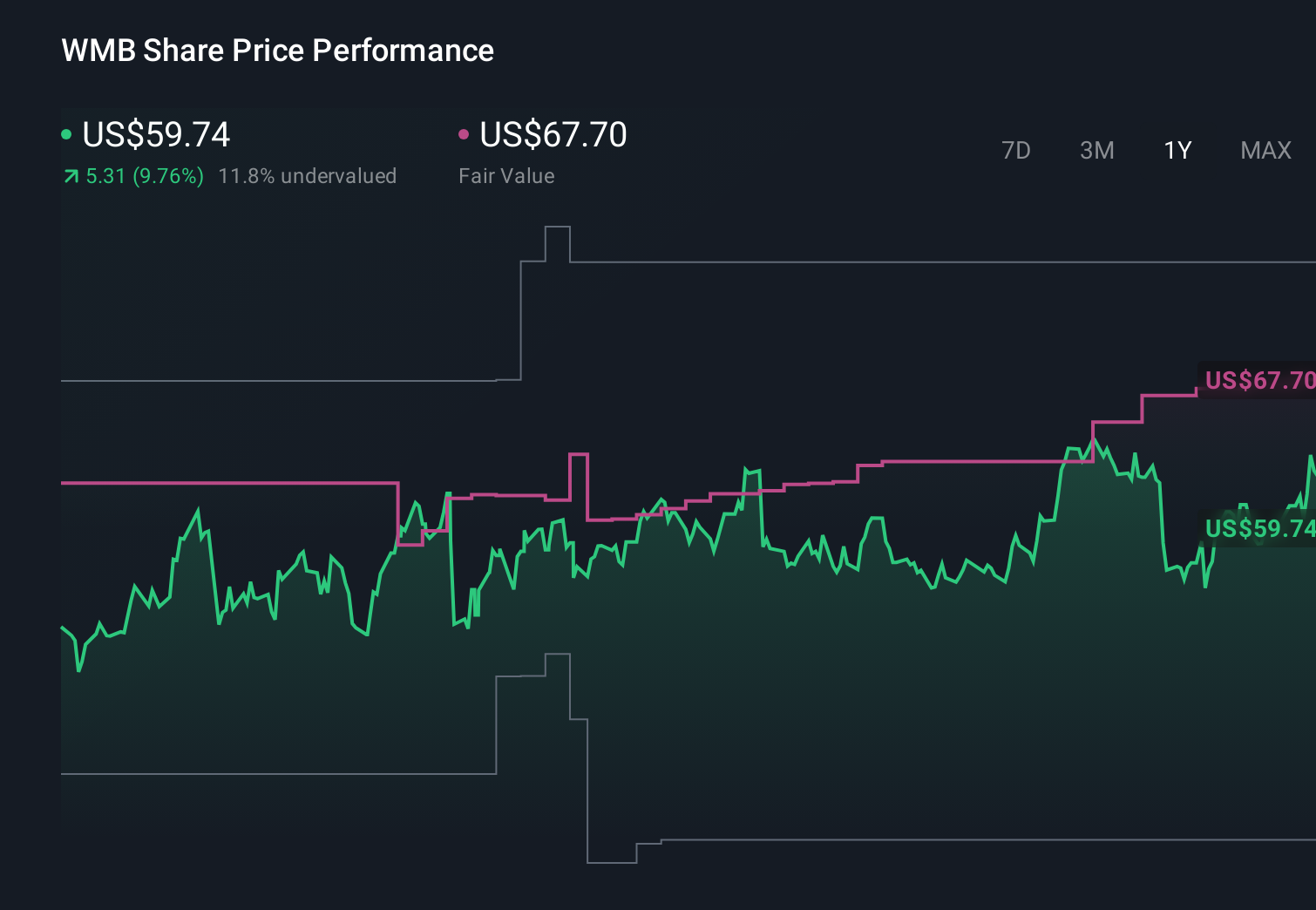

Williams Companies' narrative projects $16.3 billion revenue and $3.9 billion earnings by 2029. This requires 11.3% yearly revenue growth and about a $1.3 billion earnings increase from $2.6 billion today.

Uncover how Williams Companies' forecasts yield a $80.07 fair value, a 11% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts already saw Williams’ gas network supporting revenue of about US$17,800,000,000 and earnings near US$4,800,000,000 by 2029, so this latest focus on fee based resilience may either reinforce that upbeat view or prompt you to rethink how energy transition risks could alter those assumptions.

Explore 5 other fair value estimates on Williams Companies - why the stock might be worth 7% less than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Williams Companies research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Williams Companies research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Williams Companies' overall financial health at a glance.

Looking For Alternative Opportunities?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Find 44 companies with promising cash flow potential yet trading below their fair value.

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 29 companies in the world exploring or producing it. Find the list for free.

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.