Whirlpool (WHR) Valuation Check After Steep Multi Month Share Price Slide

Whirlpool WHR | 0.00 |

Recent performance and what it might signal for Whirlpool (WHR)

Whirlpool (WHR) has drawn investor attention after a sharp share-price slide, with the stock down about 23% over the past month and roughly 32% over the past 3 months. This has prompted closer scrutiny of its fundamentals.

Looking beyond the recent slide, Whirlpool’s 1-year total shareholder return has fallen 42.38% and the 5-year total shareholder return has declined 76.12%. This points to sustained pressure on sentiment rather than just a short term setback in the share price.

If this has you reassessing where your capital works hardest, it could be worth widening your search with a curated list of 20 top founder-led companies

So with Whirlpool trading below some valuation estimates and coming off multi year share price pressure, is the stock now trading at a discount that offers potential upside, or is the market already pricing in its future growth?

Most Popular Narrative: 23.2% Undervalued

Whirlpool's latest narrative fair value of $56.55 sits well above the last close at $43.42, framing the current share price as a discount in that framework.

Introduction of over 100 new products, including innovations in space-saving and multifunctional appliances (like the new KitchenAid suite and JennAir downdraft induction cooktops), addresses rising consumer demand for efficient, customizable, and premium offerings. This supports future revenue and margin growth.

Want to see what kind of revenue path and profit uplift need to sit behind that product story to justify the fair value? The narrative leans on a gradual sales build, firmer margins, and a richer earnings multiple, a mix that only really makes sense once you see how the moving parts are stitched together.

Result: Fair Value of $56.55 (UNDERVALUED)

However, there are still clear pressure points, including softer appliance demand and higher leverage, that could quickly challenge the optimism baked into that fair value story.

Another way to look at Whirlpool’s value

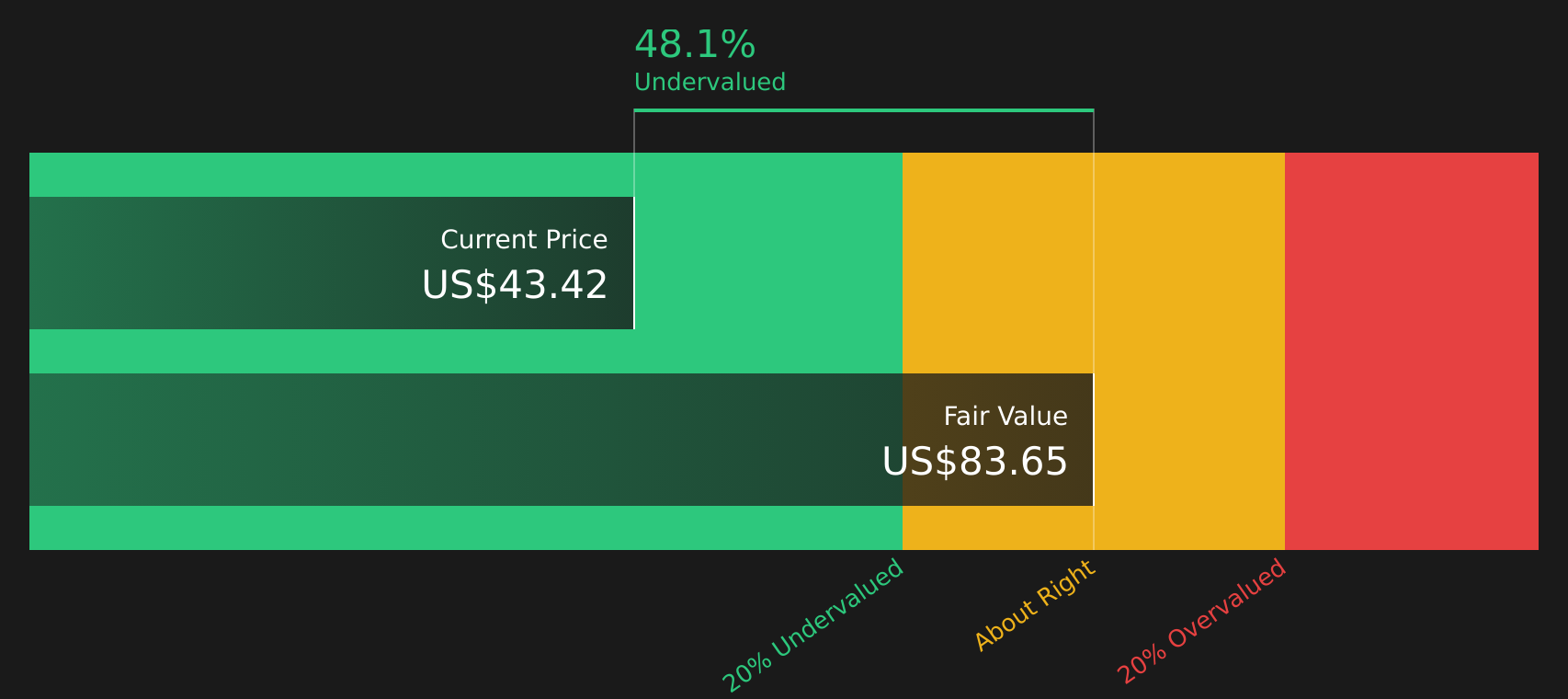

Our DCF model tells a different story to the $56.55 narrative fair value. On that framework, Whirlpool’s estimated future cash flow value is $83.65 per share, versus a current price of $43.42, which points to the stock being undervalued on this second method as well. The real question is which set of assumptions you trust more.

Next Steps

With mixed signals in the story so far, it is worth looking at the full picture for yourself and acting while sentiment is still in flux. You can start with 3 key rewards and 3 important warning signs.

Looking for more investment ideas?

If Whirlpool has you rethinking your portfolio mix, do not stop here. There are plenty of other stocks that could line up better with your goals.

- Target higher potential growth by scanning 23 elite penny stocks with strong financials that pair smaller size with relatively strong fundamentals.

- Hunt for potential bargains with the 46 high quality undervalued stocks that filters for quality companies trading below their estimated worth.

- Prioritize resilience by browsing the 63 resilient stocks with low risk scores focused on businesses with steadier risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.