White House Pushes Fannie Mae Deeper Into MBS Market And Policy Risk

FEDERAL NATIONAL MORTGAGE ASSOC FNMA | 6.89 | -2.61% |

- White House directs Federal National Mortgage Association (OTCPK:FNMA) to inject US$200b into the mortgage backed securities market.

- Policy move targets lower borrowing costs and expanded liquidity for homebuyers and lenders.

- Initial effects include a surge in mortgage applications and reduced mortgage rates across parts of the market.

- Intervention raises questions about long term implications for housing finance and Fannie Mae's operating model.

Fannie Mae sits at the core of the US housing finance system, buying mortgages from lenders and packaging them into mortgage backed securities. This new US$200b directive significantly expands that role in a single step, at a time when affordability, credit standards, and liquidity are front of mind for borrowers and lenders. For you as an investor, it puts policy risk and government influence squarely in focus for OTCPK:FNMA.

Looking ahead, market participants are likely to watch how this intervention affects credit quality, capital needs, and funding costs for Fannie Mae. You may also want to track whether this becomes a one off response or a template for future government actions in the housing market.

Stay updated on the most important news stories for Federal National Mortgage Association by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on Federal National Mortgage Association.

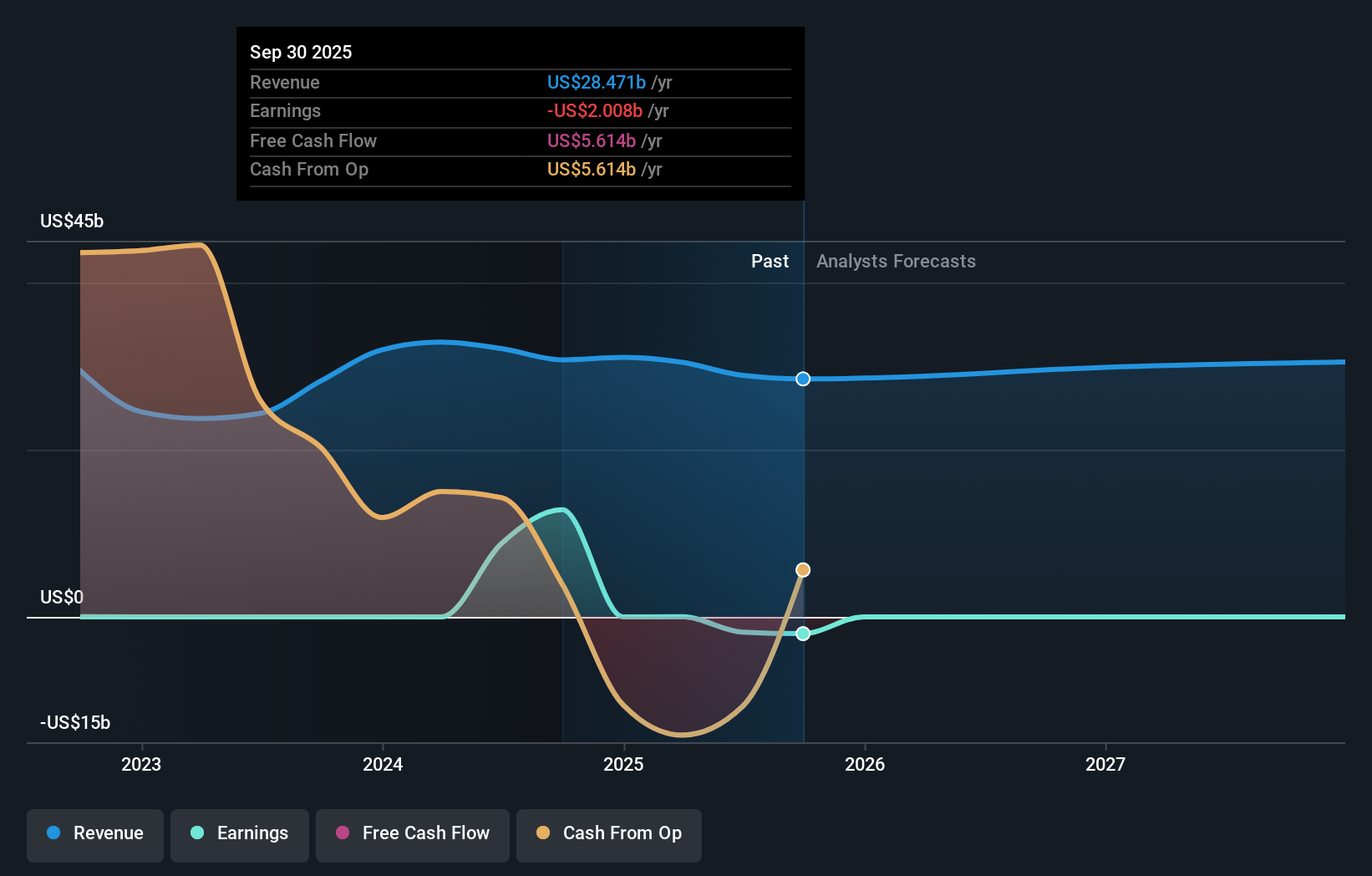

The White House directive effectively asks Fannie Mae to lean further into its core role as a liquidity provider, at the same time it is reporting full year 2025 net income of US$14,364m compared to US$16,978m a year earlier and highlighting a US$22b capital deficit in its 10 K. Increasing agency MBS investments on this scale could lift balance sheet size and risk exposure, while earnings and capital remain key discussion points in the 10 K and earnings call. For you, the question is how this policy driven expansion interacts with Fannie Mae’s conservatorship status, capital requirements, and use of credit risk transfer programs such as CIRT, which are already used to distribute mortgage credit risk to private investors.

The Risks and Rewards Investors Should Consider

- ⚠️ Capital adequacy remains a concern, with the 10 K pointing to a US$22b capital deficit that could limit flexibility if losses increase or regulatory expectations change.

- ⚠️ Debt is not well covered by operating cash flow, and the US$200b directive may increase funding needs and execution risk if market conditions become less favorable.

- 🎁 Fannie Mae holds roughly 24% of US residential mortgage debt, so deeper MBS activity could reinforce its position as a key liquidity provider in housing finance.

- 🎁 Credit risk transfer programs and securitization expertise may give Fannie Mae tools to manage some of the additional risk tied to larger MBS purchases.

What To Watch Going Forward

From here, it is worth watching how the US$200b injection shows up in Fannie Mae’s future financial statements, including the size and mix of its MBS portfolio, credit performance, and capital position. Updates from the Federal Housing Finance Agency on conservatorship terms and capital rules will be important, because they frame how far Fannie Mae can extend this policy driven role. You may also want to compare how Fannie Mae’s approach to credit risk transfer, earnings resilience, and capital management stacks up against Freddie Mac and large private mortgage lenders that package or hold mortgage backed securities.

To ensure you're always in the loop on how the latest news impacts the investment narrative for Federal National Mortgage Association, head to the community page for Federal National Mortgage Association to never miss an update on the top community narratives.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.