Why Aspen Aerogels (ASPN) Is Down 13.3% After Impairment-Driven Loss And Strategic Review News

Aspen Aerogels Inc ASPN | 3.69 | +6.34% |

- In February 2026, Aspen Aerogels reported fourth-quarter 2025 sales of US$41.34 million versus US$123.09 million a year earlier, swung to a net loss of US$72.91 million, recorded an impairment charge on property, plant and equipment, and launched a broad review of options for its business and capital structure.

- An important insight is that management characterizes this strategic review as coming from a position of financial strength and operational progress, even as the company posts a full-year 2025 net loss of US$389.55 million and guides to a further net loss of US$20 million to US$23 million for the first quarter of 2026.

- We’ll now examine how the sizeable impairment charge and ongoing strategic review may reshape Aspen Aerogels’ previously optimistic investment narrative.

Explore 23 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

Aspen Aerogels Investment Narrative Recap

To own Aspen Aerogels today, you have to believe its aerogel platform can support a sustainable business despite sharp revenue contraction and sizeable losses. The near term catalyst is whether the ongoing review of “commercial growth plans” and “capital structure” produces a credible path to stabilizing cash burn. The biggest current risk is that prolonged weakness in EV related demand and Energy Industrial projects keeps revenues low relative to Aspen’s fixed cost base.

The most relevant update is Aspen’s new Q1 2026 guidance for revenue of US$35 million to US$40 million and a net loss of US$20 million to US$23 million. This outlook, paired with the Statesboro related impairment and broad strategic review, reframes earlier expectations that cost cuts alone could quickly restore profitability and makes the timing and quality of any demand recovery even more important for the investment case.

Yet while the story can still sound attractive on paper, investors should be aware that...

Aspen Aerogels' narrative projects $513.3 million revenue and $62.9 million earnings by 2028. This requires 8.9% yearly revenue growth and a $374.8 million earnings increase from -$311.9 million today.

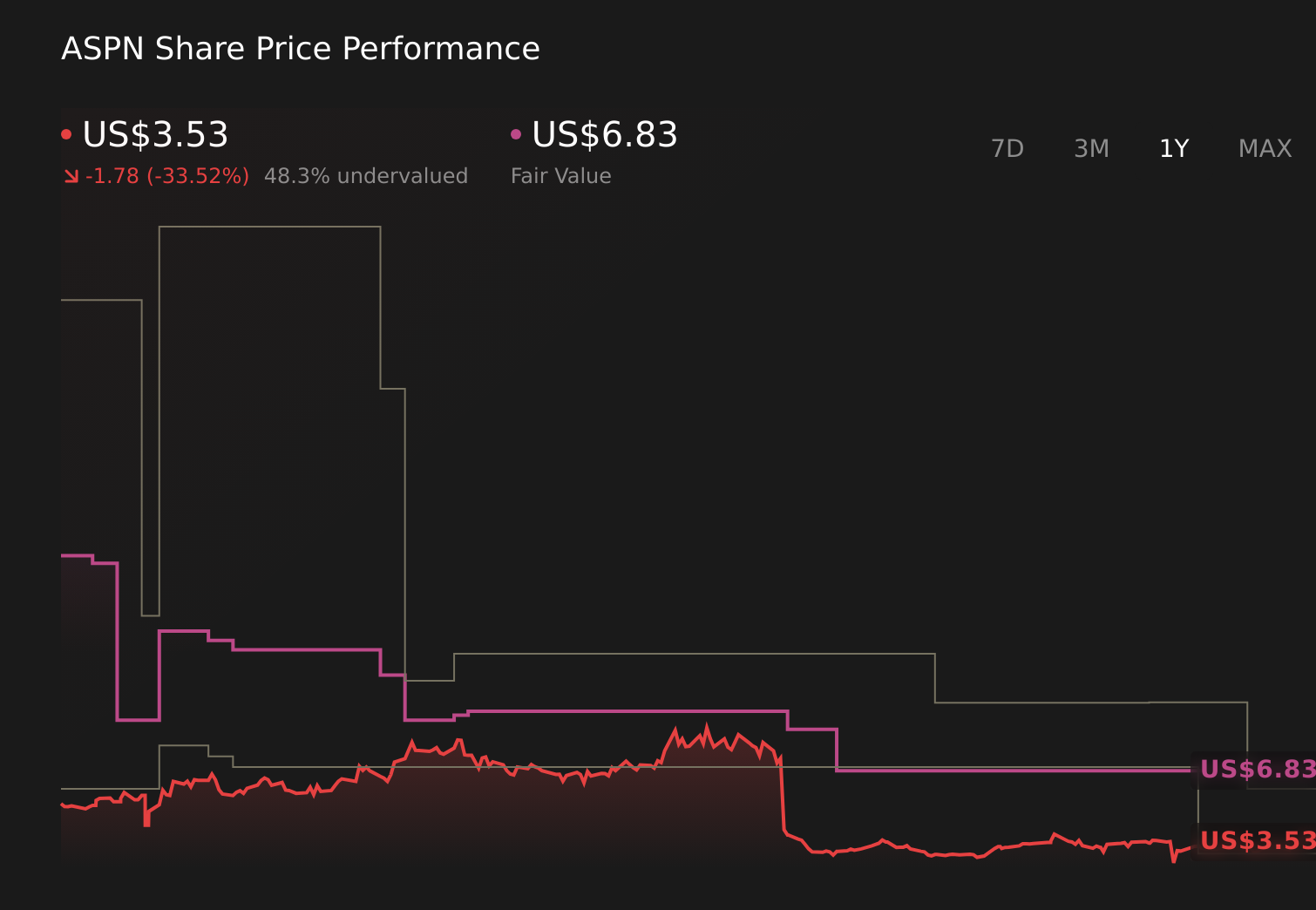

Uncover how Aspen Aerogels' forecasts yield a $6.83 fair value, a 118% upside to its current price.

Exploring Other Perspectives

Before this impairment driven reset, the most optimistic analysts were assuming Aspen could reach about US$563 million in revenue and US$106 million in earnings by 2028, but events like the Statesboro write down and rising concern about heavy EV exposure show how quickly those upbeat assumptions may need to be revisited and why your view might differ sharply from theirs.

Explore 10 other fair value estimates on Aspen Aerogels - why the stock might be worth just $6.00!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Aspen Aerogels research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Aspen Aerogels research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Aspen Aerogels' overall financial health at a glance.

Ready For A Different Approach?

Our top stock finds are flying under the radar-for now. Get in early:

- Outshine the giants: these 23 early-stage AI stocks could fund your retirement.

- AI is about to change healthcare. These 29 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The future of work is here. Discover the 29 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.