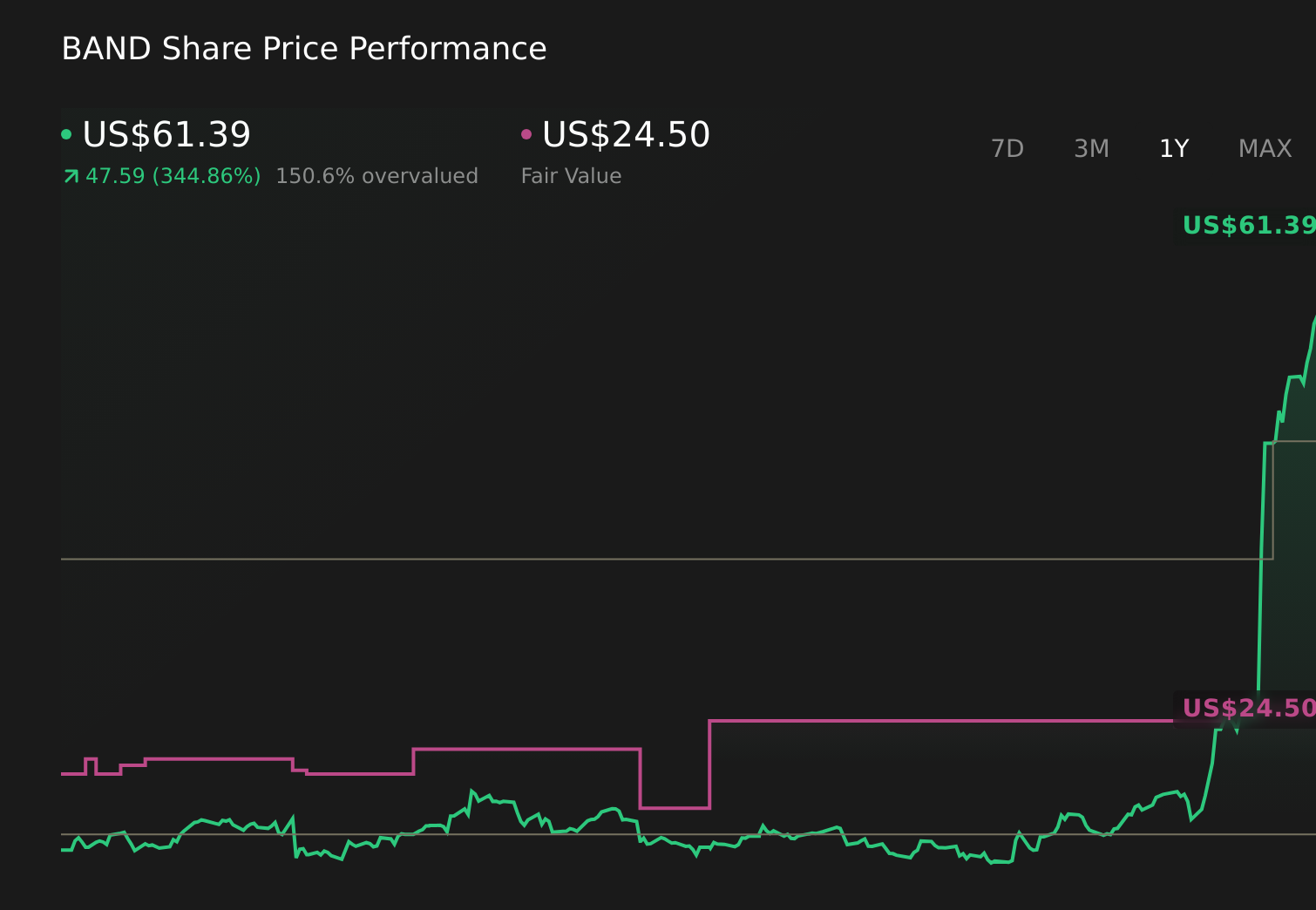

Why Bandwidth (BAND) Is Up 86.0% After Raising 2026 Guidance And Highlighting New AI Partnership

Bandwidth Inc. Class A BAND | 0.00 |

- In the first quarter of 2026, Bandwidth Inc. reported record revenue of US$208.78 million, moved from a net loss to US$4.12 million in net income, and raised its revenue guidance for both the June quarter and full year 2026.

- The company also spotlighted accelerating AI-driven usage of its communications platform and an expanded role powering Salesforce’s new Agentforce Contact Center, underscoring how AI integrations are reshaping its enterprise demand mix.

- We'll now examine how Bandwidth's upgraded 2026 guidance and AI-focused Salesforce partnership affect its existing investment narrative and risk profile.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 18 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Bandwidth Investment Narrative Recap

To own Bandwidth today, you need to believe its AI-infused communications cloud can deepen relationships with large enterprises fast enough to justify recent share price gains and ongoing investment needs. Q1 2026’s record US$208.78 million revenue and the guidance lift make the near term more about execution on AI usage and Salesforce-driven volume, while customer concentration and the cost of staying at the AI frontier still look like the most important risks.

The most relevant new data point is the upgraded 2026 revenue outlook to US$880–900 million, following Q1’s beat versus prior US$864–884 million guidance. This reinforces the idea that AI-heavy enterprise traffic is already flowing through Bandwidth’s platform, but it also raises the bar for future quarters and makes any slowdown in Salesforce-related volumes or large enterprise deals more consequential for the story investors are buying into.

Yet beneath the upbeat AI story, investors should also be aware of how concentrated enterprise relationships could quickly become a problem if...

Bandwidth's narrative projects $987.7 million revenue and $17.8 million earnings by 2028.

Uncover how Bandwidth's forecasts yield a $24.50 fair value, a 45% downside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were assuming only about 7.8 percent annual revenue growth to around US$950.2 million by 2028, which is much more cautious than the AI acceleration story and highlights how differently you and other investors might view the same Q1 beat and guidance raise.

Explore 3 other fair value estimates on Bandwidth - why the stock might be worth 45% less than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Bandwidth research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Bandwidth research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Bandwidth's overall financial health at a glance.

Curious About Other Options?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

- AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.