Why Boot Barn (BOOT) Is Down 9.4% After Raising Guidance And Expanding Store Growth Plans

Boot Barn Holdings, Inc. BOOT | 149.87 149.87 | +0.56% 0.00% Post |

- Boot Barn Holdings recently reported past quarterly results that exceeded revenue and earnings estimates, fueled by higher transaction volumes and continued new store openings, and raised its guidance for the coming fiscal year while outlining additional expansion plans.

- Despite these stronger-than-expected results, investor reactions have been mixed as some shareholders focus on the company’s cautious near-term outlook and the risk of slower growth ahead.

- Now we’ll examine how the stronger-than-expected earnings and cautious outlook could reshape Boot Barn’s investment narrative and risk profile.

Uncover the next big thing with 33 elite penny stocks that balance risk and reward.

Boot Barn Holdings Investment Narrative Recap

To own Boot Barn today, you need to believe its store led growth, western and workwear focus, and omni channel investments can keep attracting new customers without eroding returns. The upside catalyst is still successful new store openings and transaction growth, and this quarter’s earnings beat and higher guidance support that story. The biggest near term risk remains that expansion or price increases outpace demand; the latest results do not remove that concern, but they have not materially worsened it either.

The most relevant recent announcement is Boot Barn’s plan to open about 70 new stores, which sits at the center of both the bull case and the risk profile. Those openings amplify the primary catalyst of underpenetrated markets and cultural tailwinds for western and workwear styles, but they also heighten worries about overexpansion, cannibalization, and sensitivity to shifting fashion preferences if growth in newer regions proves harder to sustain.

But investors should also consider the risk that if new stores or price increases disappoint, the impact on margins and returns could be far larger than...

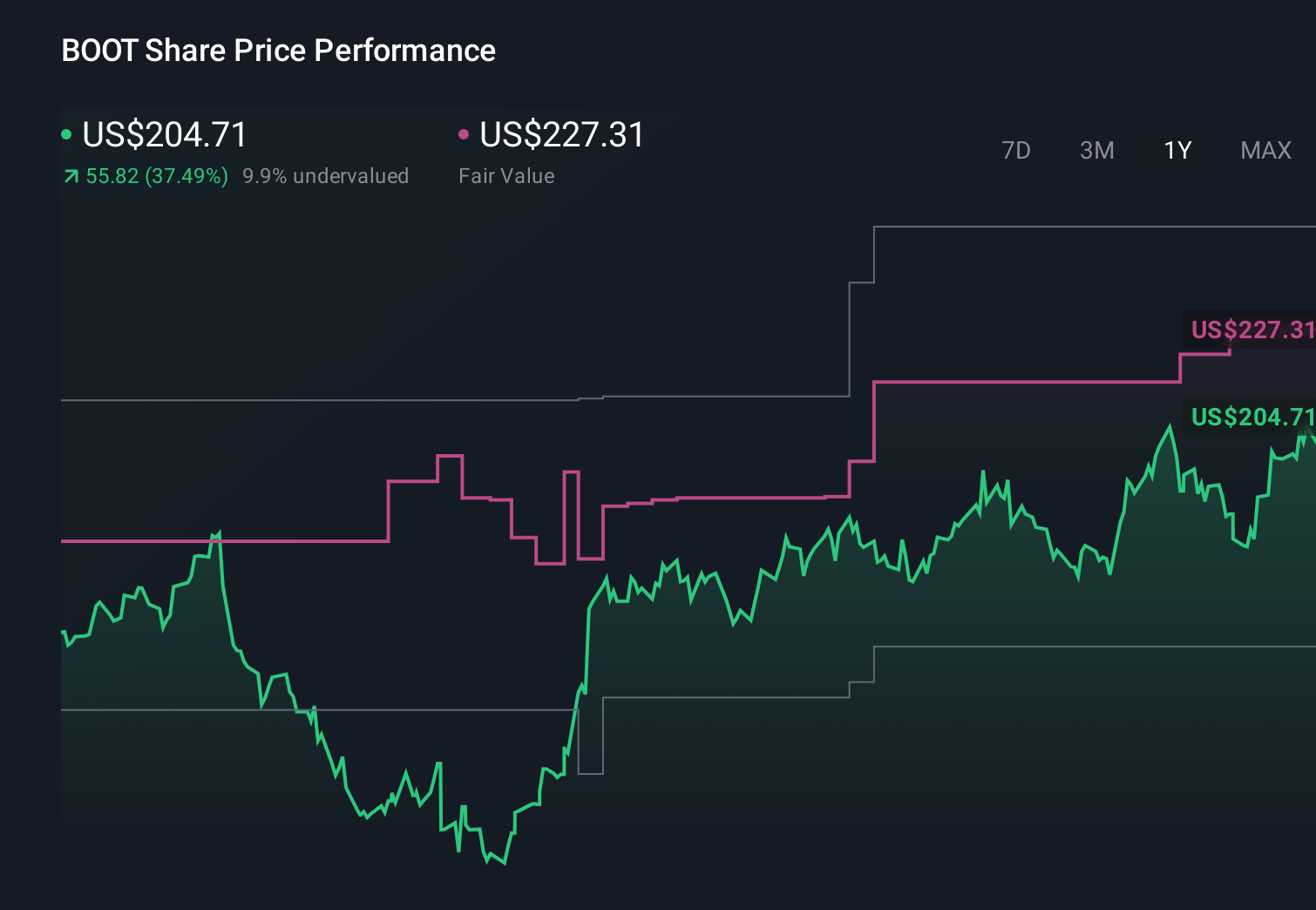

Boot Barn Holdings’ narrative projects $3.2 billion revenue and $349.8 million earnings by 2029.

Uncover how Boot Barn Holdings' forecasts yield a $237.14 fair value, a 75% upside to its current price.

Exploring Other Perspectives

Some analysts were already far more optimistic, assuming revenue could reach about US$2.8 billion and earnings US$300 million, yet this quarter’s stronger results and cautious tone may push those projections, and concerns about rapid store expansion, in very different directions depending on how you read the risks.

Explore 4 other fair value estimates on Boot Barn Holdings - why the stock might be worth over 2x more than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Boot Barn Holdings research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Boot Barn Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Boot Barn Holdings' overall financial health at a glance.

Ready For A Different Approach?

Our top stock finds are flying under the radar-for now. Get in early:

- We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Find 59 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.