Why Carnival (CCL) Is Up 6.7% After Year-Round Europe Plans And Cheaper Fuel Inputs

Carnival Corporation Ltd. CCL | 0.00 |

- In recent days, Carnival-owned Holland America Line confirmed plans for year-round European cruising from 2027–2028, while crude oil prices dropped following progress toward a U.S.–Iran agreement affecting the Strait of Hormuz, easing a major input cost for cruise operators.

- Together, these developments highlight how both itinerary expansion and lower fuel expenses could reshape Carnival’s operating profile, especially outside the traditional summer peak season.

- We’ll now examine how the recent relief in oil costs might influence Carnival’s existing investment narrative around margins, growth, and risk.

AI is about to change healthcare. These 35 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Carnival Investment Narrative Recap

To own Carnival today, you need to believe that cruising can convert resilient travel demand into healthier margins while the company manages its large debt load. The recent drop in oil prices directly supports the key short term catalyst of margin improvement by easing a major cost line, while geopolitical tensions and index removals still leave sentiment and refinancing risk as central concerns. Overall, the crude move looks helpful but not thesis changing on its own.

Holland America’s decision to keep Nieuw Statendam in Europe year round from 2027 to 2028 ties directly into that margin story, extending capacity into shoulder and winter periods where profitable utilization has been harder to achieve. Together with lower fuel costs, this could make off season deployment more attractive and support Carnival’s effort to grow earnings without relying solely on new ships or aggressive discounting.

Yet against these positives, investors should not overlook the ongoing risk that Carnival’s sizeable debt load could...

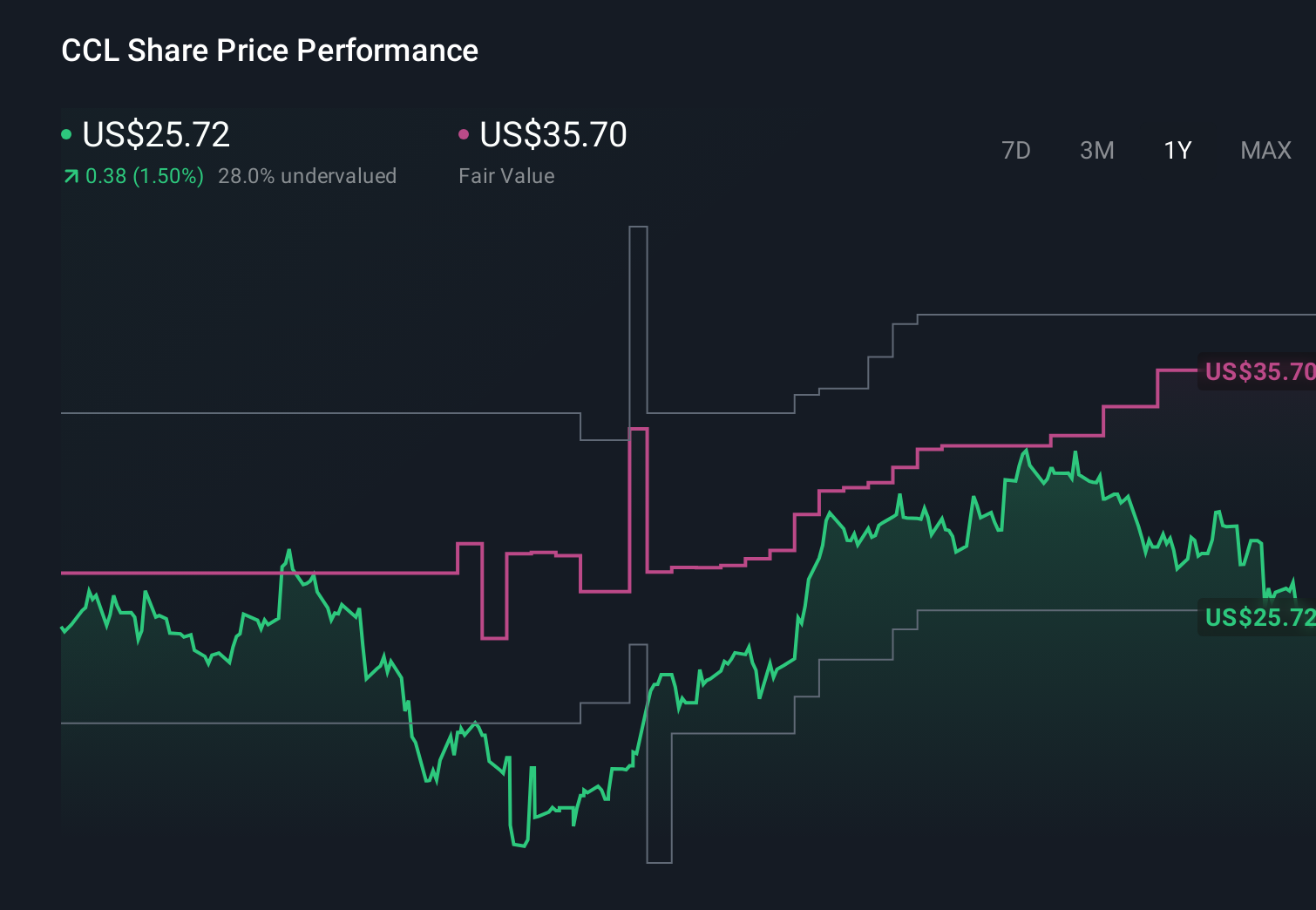

Carnival's narrative projects $29.0 billion revenue and $3.7 billion earnings by 2028. This requires 3.8% yearly revenue growth and a $1.2 billion earnings increase from $2.5 billion today.

Uncover how Carnival's forecasts yield a $37.70 fair value, a 35% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already assuming earnings could reach about US$4.3 billion by 2029, yet they still flagged persistent geopolitical instability as a key threat; this latest oil and Middle East news might either reinforce their confidence or force a rethink, reminding you that reasonable views on Carnival can diverge sharply and are worth comparing.

Explore 10 other fair value estimates on Carnival - why the stock might be worth over 2x more than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Carnival research is our analysis highlighting 5 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Carnival research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Carnival's overall financial health at a glance.

Want Some Alternatives?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Rare earth metals are the new gold rush. Find out which 31 stocks are leading the charge.

- Capitalize on the AI infrastructure supercycle with our selection of the 46 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Uncover the next big thing with 23 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.