Why Carvana (CVNA) Is Down 7.7% After Profit Margins Tighten Amid Expansion Efforts And Financing Shifts

Carvana CVNA | 0.00 |

- In recent months, Carvana reported quarterly results where profitability fell short of expectations as gross profit per unit declined due to industry-wide car depreciation, lower shipping fees, and less efficient reconditioning at newly acquired sites, even as units and revenue rose year over year.

- Around the same time, analysts revised their views, Carvana’s securitization terms shifted, and its ADESA unit launched a new “ADESA Timed” digital auction channel, underscoring both evolving financing conditions and continued efforts to expand its wholesale and retail reach.

- We’ll now examine how this recent profitability shortfall, driven by lower gross profit per unit, may influence Carvana’s existing investment narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 48 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Carvana Investment Narrative Recap

To own Carvana, you generally have to believe its online, vertically integrated model can keep scaling profitably despite a complex used car market and heavy past investment. The recent gross profit per unit shortfall and weaker securitization terms sharpen the near term focus on unit economics and financing costs, but do not yet appear to fundamentally change the story. The key short term catalyst remains operational execution at ADESA sites, while the biggest risk is margin pressure from inefficiencies and industry pricing.

Among recent developments, the launch of ADESA Timed looks most connected to this earnings miss. It extends Carvana’s digital wholesale reach, which could matter for future gross profit per unit if it supports faster inventory turns and better remarketing of vehicles. However, with analysts still updating their models after weaker retail unit margins and evolving securitization terms, it is not yet clear how much this new channel will influence the near term catalyst of improving profitability.

Yet investors should also be aware that Carvana’s shifting securitization terms could eventually affect its ability to fund growth at current economics…

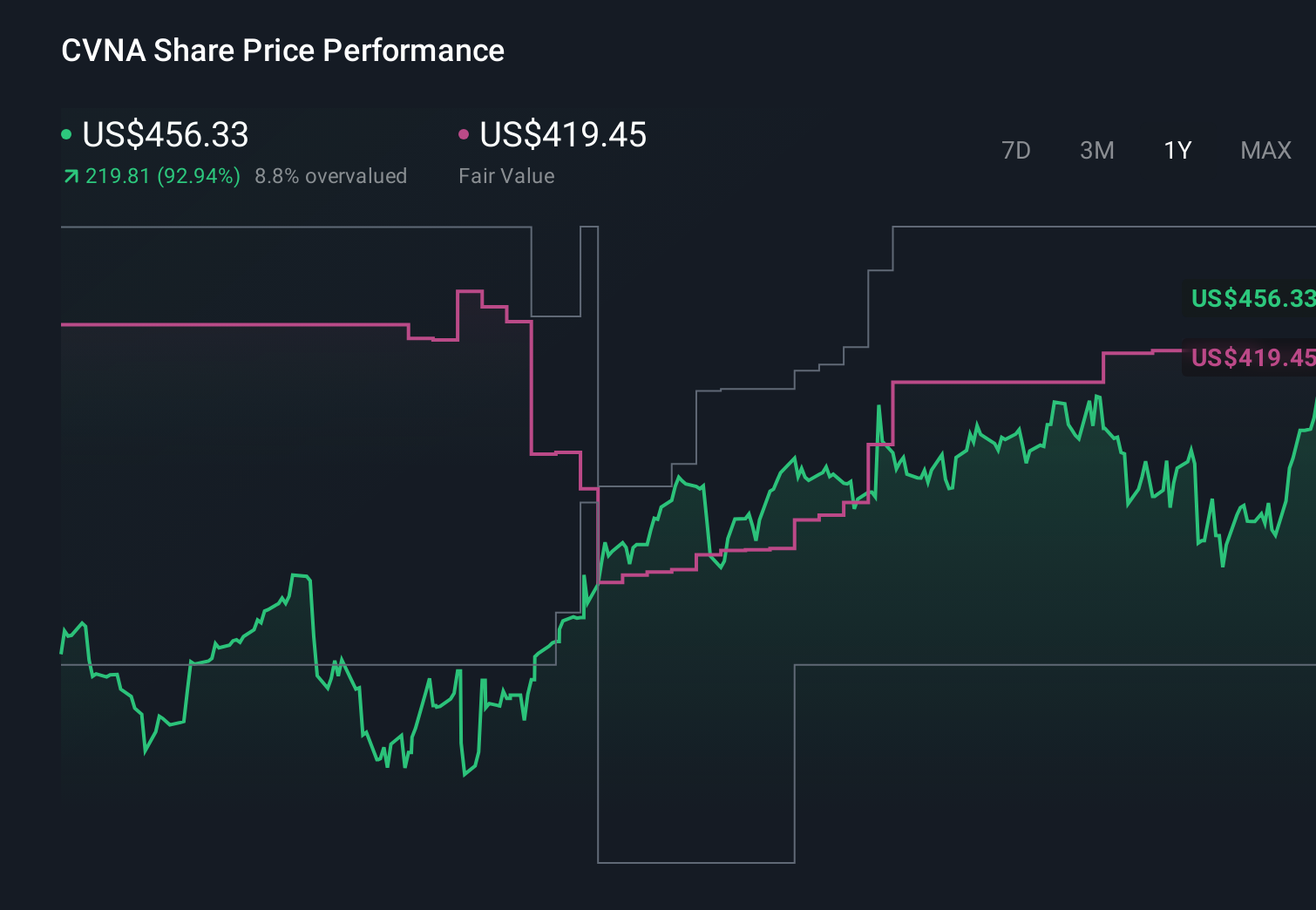

Carvana’s narrative projects $44.1 billion revenue and $2.9 billion earnings by 2029. This requires 25.1% yearly revenue growth and roughly a doubling in earnings from $1.4 billion today.

Uncover how Carvana's forecasts yield a $92.90 fair value, a 45% upside to its current price.

Exploring Other Perspectives

While consensus focuses on execution risk, the most optimistic analysts were previously modeling revenue of about US$50,000,000,000 and earnings of roughly US$3,700,000,000, so this profit shortfall and financing shift may prompt you to reconsider whether that upside story or a more cautious view feels closer to your own.

Explore 9 other fair value estimates on Carvana - why the stock might be worth over 5x more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Carvana research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Carvana research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Carvana's overall financial health at a glance.

Curious About Other Options?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- The latest GPUs need a type of rare earth metal called Terbium and there are only 31 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.