Why CAVA Group (CAVA) Is Down 8.6% After CEO Share Sale And Estimate Cuts - And What's Next

CAVA Group, Inc. CAVA | 79.63 | -0.64% |

- CAVA Group recently drew heightened investor attention after CEO Brett Schulman sold a substantial block of company shares, coinciding with analyst earnings estimate revisions and a Zacks Rank #4 (Sell) rating ahead of its upcoming earnings report.

- The tension between ongoing revenue growth expectations, rapid restaurant expansion plans, and softer near-term earnings forecasts has become a central focus for investors reassessing CAVA’s risk‑reward profile.

- With recent earnings estimate cuts and concerns about rapid expansion in focus, we’ll examine how this news reshapes CAVA Group’s investment narrative.

Find companies with promising cash flow potential yet trading below their fair value.

What Is CAVA Group's Investment Narrative?

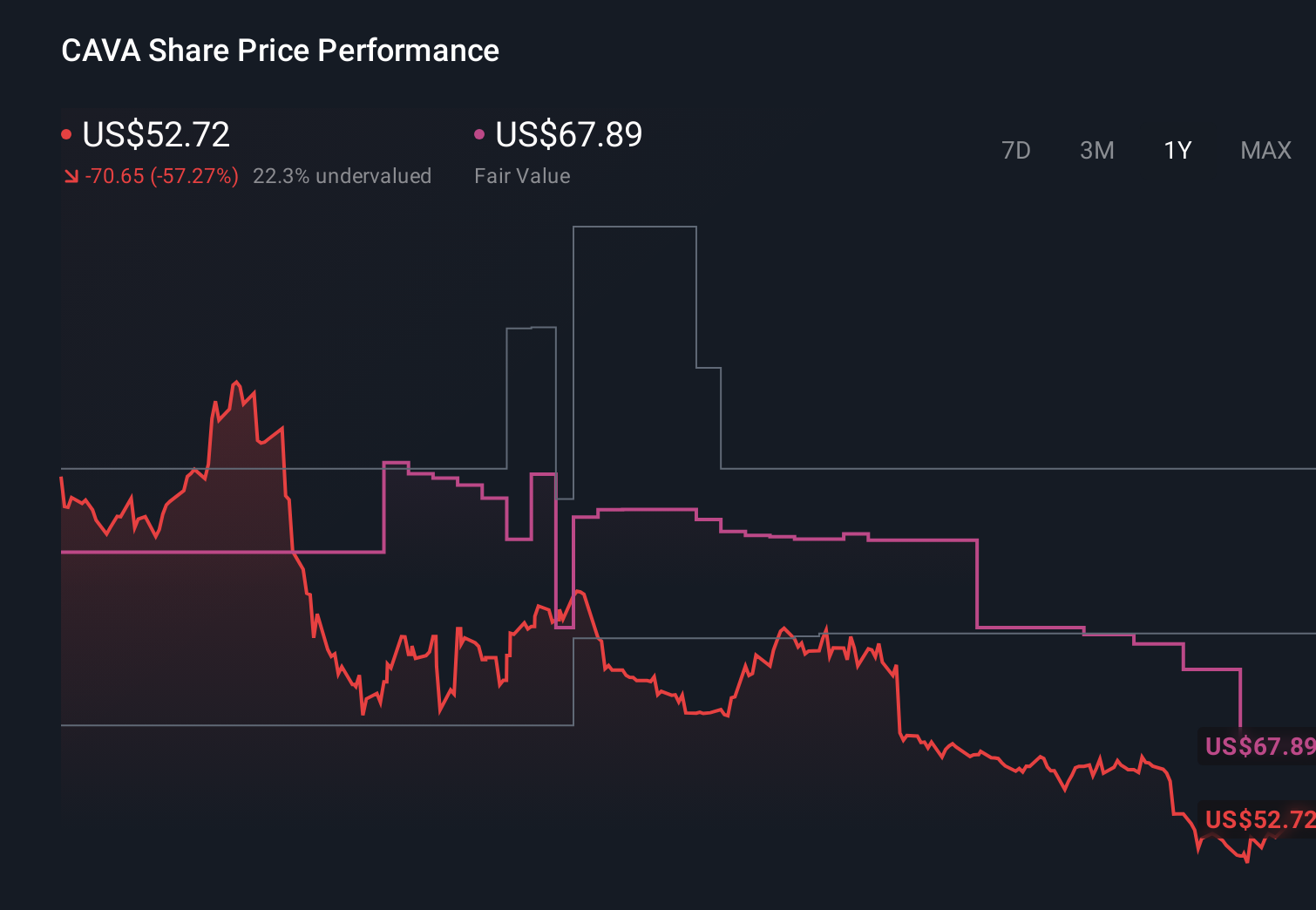

To own CAVA today, you have to believe the brand can keep scaling profitably while justifying a premium valuation in a competitive fast‑casual space. The story is still about converting rapid unit growth and mid‑teens revenue expansion into durable earnings, despite forecasts that profits grow slower than the broader market and returns on equity stay only moderate. That makes execution in new markets and at the Verona production facility central short term catalysts. The recent CEO share sale and a Zacks Rank #4 (Sell), alongside trimmed earnings estimates and a sharp pullback after strong gains, push sentiment risk and valuation risk closer to the forefront, even as long term expansion targets remain unchanged. For now, the news looks more sentiment‑shaping than thesis‑breaking.

But one risk in particular could matter more than the recent insider selling. CAVA Group's share price has been on the slide but might be up to 18% below fair value. Find out if it's a bargain.Exploring Other Perspectives

Explore 10 other fair value estimates on CAVA Group - why the stock might be worth 15% less than the current price!

Build Your Own CAVA Group Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your CAVA Group research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free CAVA Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate CAVA Group's overall financial health at a glance.

No Opportunity In CAVA Group?

Our top stock finds are flying under the radar-for now. Get in early:

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- Outshine the giants: these 24 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.