Why CAVA Group (CAVA) Is Up 11.4% After New COO Hire And Major Menu Overhaul

CAVA Group, Inc. CAVA | 79.63 | -0.64% |

- CAVA Group, Inc. recently appointed veteran operator Doug Thompson as Chief Operations Officer, effective March 2, 2026, and earlier this month rolled out its largest-ever nationwide Mediterranean menu update, featuring new high-protein bowls, sides, drinks, and the return of white sweet potato.

- Together, the leadership hire and expanded menu highlight CAVA’s emphasis on sharpening restaurant operations while broadening its offering to keep guests engaged as it scales.

- We’ll now examine how Thompson’s operations expertise could influence CAVA’s existing investment narrative around expansion, margins, and menu innovation.

Find companies with promising cash flow potential yet trading below their fair value.

CAVA Group Investment Narrative Recap

To own CAVA, you need to believe its fast expansion and Mediterranean focus can support sustained traffic and margins despite a rich valuation and mixed earnings expectations. The key near term catalyst remains execution on new unit openings, while the biggest risk is that slowing same restaurant traffic and high investor expectations create a wide gap between operational realities and what is already priced into the shares. Thompson’s appointment and the menu refresh do not materially change that risk, but they directly target it.

The January 2026 nationwide menu launch is most relevant here, because it shows CAVA still investing in product variety to keep guests engaged as it grows. Paired with an incoming COO whose background is in scaling restaurant operations, this reinforces the existing catalyst that hinges on successful unit growth and operational efficiency at a time when the market is closely watching traffic trends and margins.

But investors should also be aware that if aggressive expansion leads to cannibalization and weaker returns on new locations...

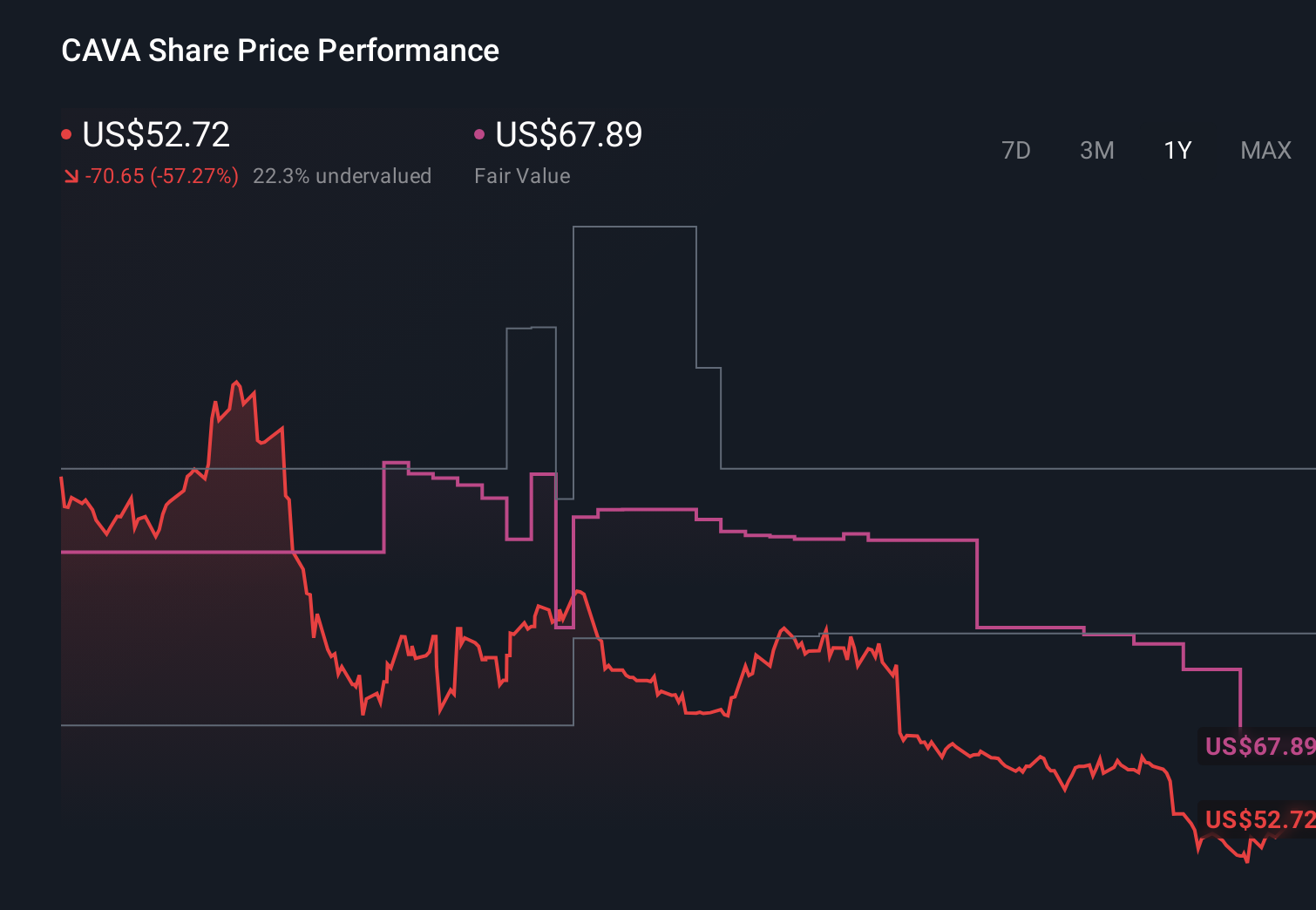

CAVA Group's narrative projects $1.9 billion revenue and $126.2 million earnings by 2028. This requires 20.4% yearly revenue growth and a $14.5 million earnings decrease from $140.7 million today.

Uncover how CAVA Group's forecasts yield a $69.63 fair value, in line with its current price.

Exploring Other Perspectives

Ten fair value estimates from the Simply Wall St Community span roughly US$52 to US$110, showing how differently individual investors are sizing up CAVA. Against that backdrop, CAVA’s ambitious plan to reach 1,000 restaurants and the operational risk that expansion could strain returns give you plenty of reason to compare several viewpoints before deciding where you stand.

Explore 10 other fair value estimates on CAVA Group - why the stock might be worth as much as 56% more than the current price!

Build Your Own CAVA Group Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your CAVA Group research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free CAVA Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate CAVA Group's overall financial health at a glance.

Want Some Alternatives?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.