Why Crocs (CROX) Is Down 5.3% After Q3 Earnings Miss and Weak Outlook for Q4

Crocs, Inc. CROX | 83.66 | +0.12% |

- On October 30, 2025, Crocs, Inc. reported that its third-quarter sales fell to US$996.3 million and net income declined to US$145.82 million, with diluted earnings per share dropping to US$2.70 compared to a year earlier.

- The company also issued guidance for the fourth quarter anticipating an 8% year-over-year revenue decrease, highlighting continued pressures following a challenging nine-month period that included a net loss of US$186.36 million.

- Given the recent quarterly earnings report revealing declining sales and income, we'll examine what this means for Crocs' previously optimistic international expansion narrative.

AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Crocs Investment Narrative Recap

For investors, owning Crocs means believing in the company's capacity to revitalize its brand and capture global growth even as headwinds persist in its core North American market. The sharp decline in Q3 sales and earnings, alongside guidance for a further revenue drop, raises immediate questions about the strength of Crocs' international expansion story and increases the spotlight on North America’s subdued consumer demand as the most important short-term catalyst, while fashion cyclicality risks intensify; the impact of Q3 results here is material. Among the recent announcements, Crocs’ completion of another tranche of its share buyback program stands out amid the profit downturn. The company repurchased over 2.4 million shares in Q3 for approximately US$202.87 million, a significant show of capital allocation given ongoing margin pressure, adding another layer for investors weighing possible catalysts and risks. Yet even with buybacks, investors should not ignore the shifting consumer preferences and shelf space competition that could ...

Crocs' narrative projects $4.0 billion revenue and $925.2 million earnings by 2028. This requires a 1.0% yearly revenue decline and a $688.7 million earnings increase from $236.5 million currently.

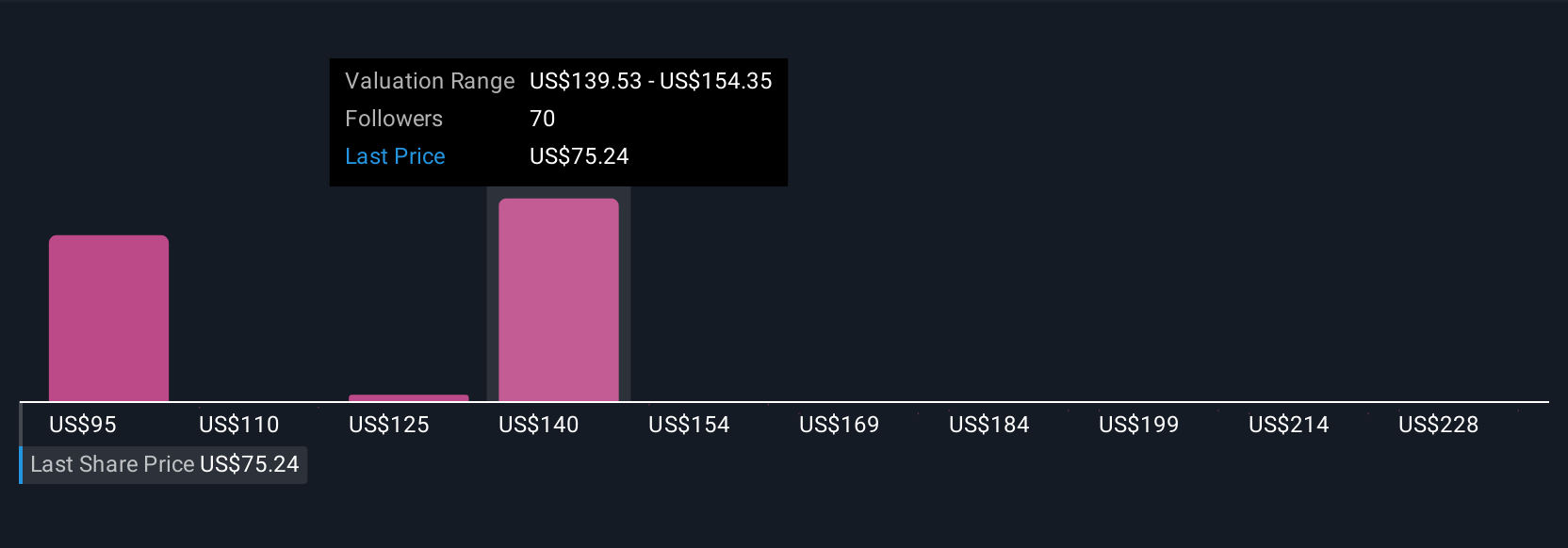

Uncover how Crocs' forecasts yield a $87.83 fair value, a 9% upside to its current price.

Exploring Other Perspectives

Fair value estimates submitted by 19 Simply Wall St Community members range widely from US$87.83 to US$168.11 per share. As expectations on international growth remain a key swing factor, it is clear that opinions on Crocs' earnings potential and risks truly vary.

Explore 19 other fair value estimates on Crocs - why the stock might be worth over 2x more than the current price!

Build Your Own Crocs Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Crocs research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Crocs research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Crocs' overall financial health at a glance.

Searching For A Fresh Perspective?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Outshine the giants: these 26 early-stage AI stocks could fund your retirement.

- Rare earth metals are the new gold rush. Find out which 38 stocks are leading the charge.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.