Why Deere (DE) Is Up 9.5% After Tightening 2026 Guidance And Boosting Capital Returns – And What's Next

Deere & Company DE | 0.00 |

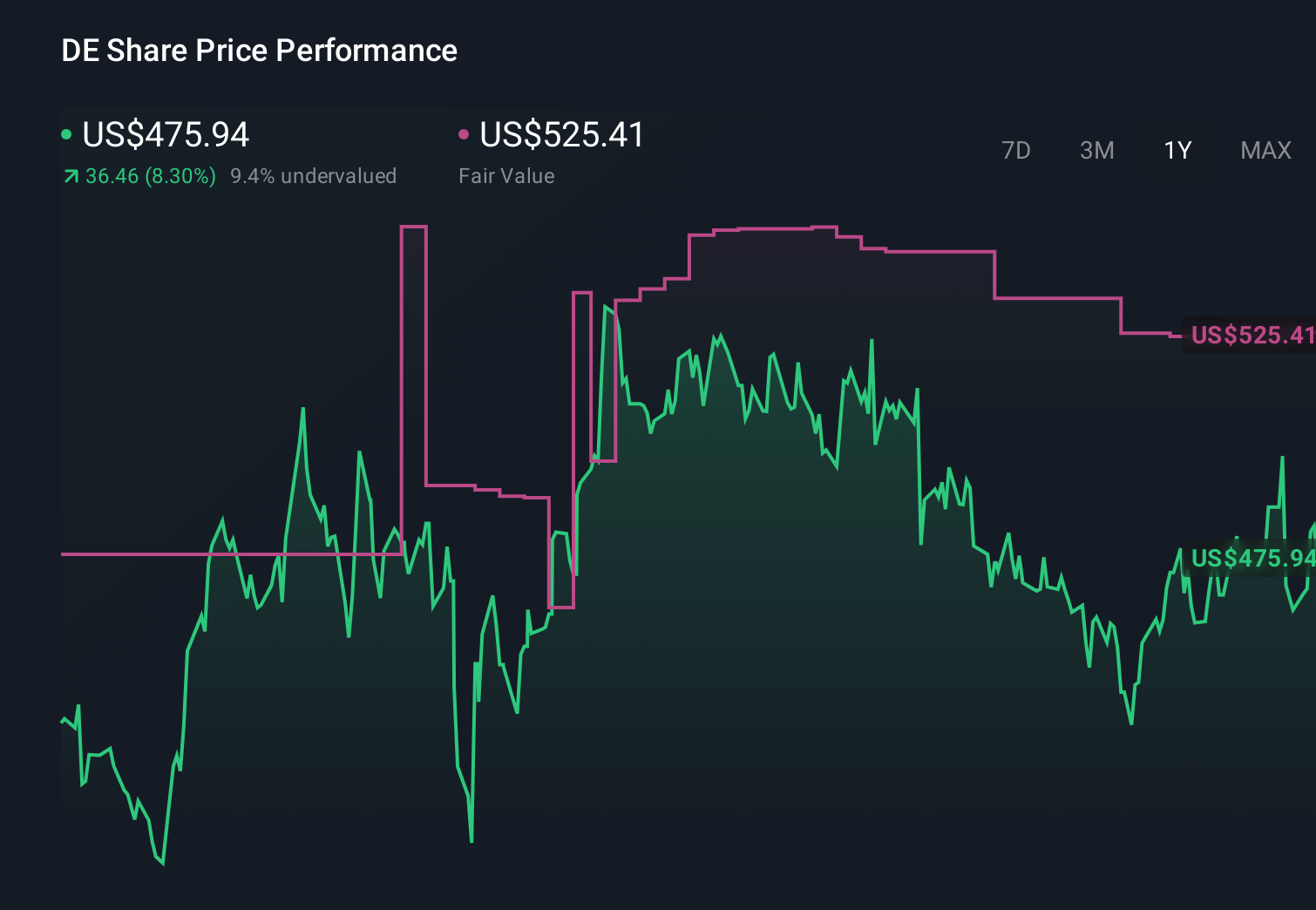

- Deere & Company recently reported second-quarter 2026 results showing sales of US$11,778 million and revenue of US$13,369 million, alongside fiscal 2026 net income guidance of US$4.5 billion to US$5.0 billion and a quarterly dividend of US$1.62 per share payable on August 10, 2026.

- While net income for the quarter was slightly lower than a year earlier and director Dmitri Stockton plans to step down after his current term, Deere’s updated earnings outlook and ongoing capital returns give investors fresh information on how the business is currently performing and being overseen.

- With Deere tightening its fiscal 2026 net income outlook to US$4.5–5.0 billion, we’ll examine how this affects the existing investment narrative.

Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

Deere Investment Narrative Recap

To own Deere, you generally need to believe its technology focused farm and construction equipment can earn solid returns despite cyclical swings in demand, tariffs and financing costs. The latest quarter shows slightly lower net income alongside firmer sales, while the tightened fiscal 2026 net income outlook and steady dividend do not materially change the near term picture. The key catalyst remains adoption of higher margin precision solutions, with a major risk that weak North American large ag demand and pricing pressure persist.

The most relevant update here is Deere’s reaffirmed fiscal 2026 net income guidance of US$4.5 billion to US$5.0 billion. That range gives you a clearer yardstick against the current headwinds of tariffs, input costs and intense pricing competition, and helps frame how much room Deere has to keep investing in precision agriculture, automation and financing tools that management hopes will offset margin pressure if equipment demand stays choppy.

Yet against this, investors should be aware that if North American large ag weakness drags on and Deere leans harder on incentives and financing tools...

Deere's narrative projects $47.4 billion revenue and $8.4 billion earnings by 2029. This requires fairly flat yearly revenue growth and an earnings increase of about $3.6 billion from $4.8 billion today.

Uncover how Deere's forecasts yield a $665.10 fair value, a 15% upside to its current price.

Exploring Other Perspectives

Before this update, the most optimistic analysts were penciling in about US$53.5 billion of revenue and US$10.3 billion of earnings by 2029, a far more upbeat story than consensus. As you look at the softer recent net income and tighter 2026 guidance, it is worth asking whether that aggressive path still fits, or if the assumptions around margins, tariffs and demand might need to shift.

Explore 3 other fair value estimates on Deere - why the stock might be worth as much as 15% more than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Deere research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Deere research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Deere's overall financial health at a glance.

Interested In Other Possibilities?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Capitalize on the AI infrastructure supercycle with our selection of the 47 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Explore 29 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.