Why DorianG (LPG) Is Up 13.7% After Surging FY 2026 Earnings And Irregular Dividend

Dorian LPG LPG | 0.00 |

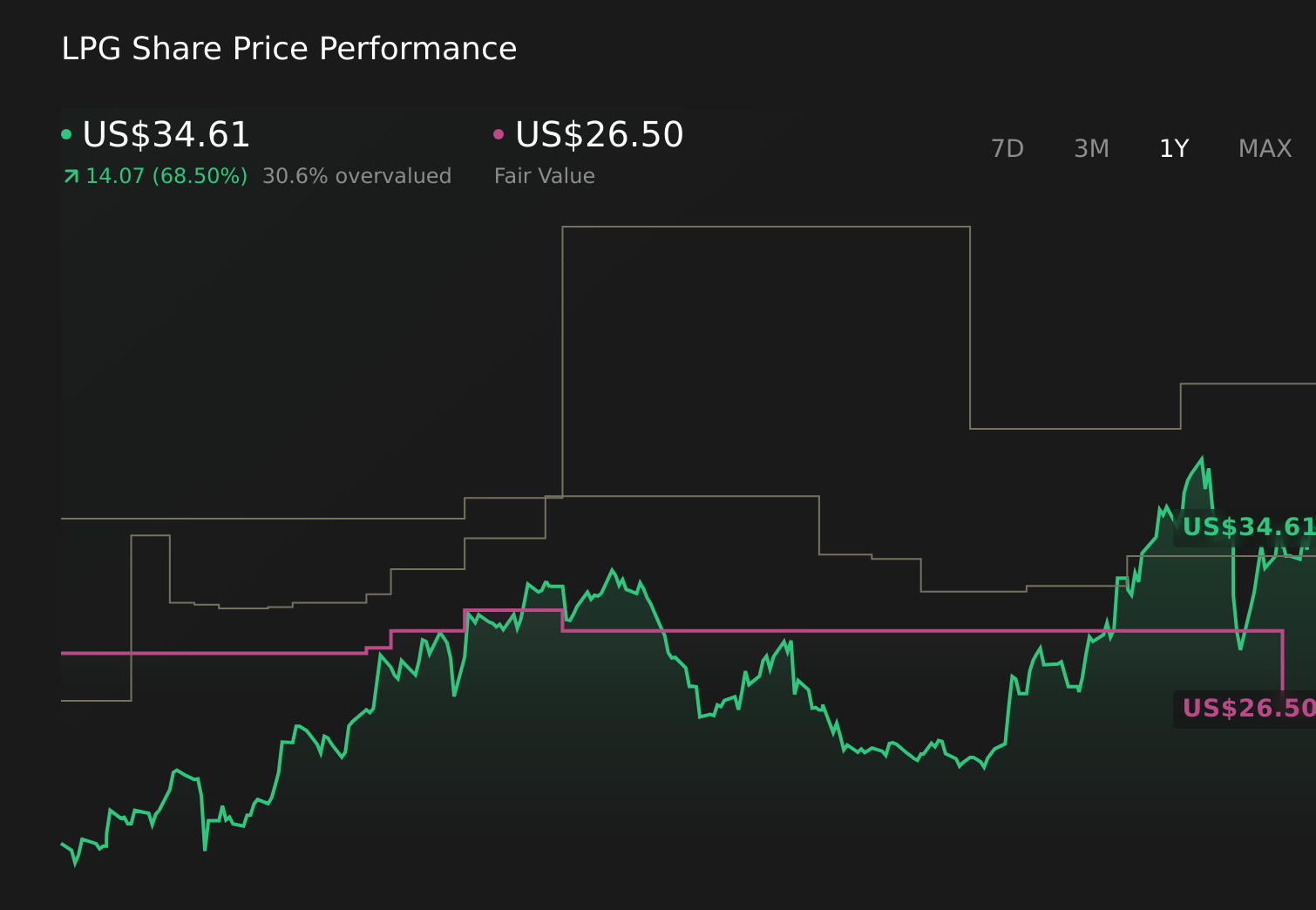

- Dorian LPG Ltd. has reported its fourth-quarter and full-year 2026 results, with quarterly sales rising to US$153.27 million and net income to US$81.01 million, while full-year sales reached US$481.51 million and net income US$193.67 million, all significantly higher than a year earlier.

- The sharp improvement in earnings, alongside vessel sale and sale-leaseback activity and an irregular dividend, highlights how Dorian LPG is using strong LPG shipping conditions to strengthen its balance sheet and reward shareholders.

- We’ll now examine how this earnings surge and irregular dividend shape Dorian LPG’s pre-existing investment narrative around growth, risk, and capital returns.

AI is about to change healthcare. These 34 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

DorianG Investment Narrative Recap

To own Dorian, you need to believe that LPG will remain a relevant transition fuel and that tight VLGC markets can support healthy utilization and margins. The latest earnings surge and irregular dividend underline that strong spot conditions are still the main short term catalyst, while exposure to freight rate swings and evolving environmental rules remains the key risk. This quarter’s results reinforce that tension but do not remove it.

The most relevant recent announcement is the irregular US$1.00 per share dividend alongside Q4 results, following other special payouts this year. It ties directly into the catalyst of robust cash generation enabling capital returns, while also raising questions about how sustainable such distributions are if freight markets soften or regulatory costs rise.

Yet investors should also be aware that growing regulatory and decarbonization pressures could eventually reshape LPG demand and vessel economics...

DorianG's narrative projects $370.1 million revenue and $90.4 million earnings by 2028.

Uncover how DorianG's forecasts yield a $33.33 fair value, a 28% downside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were assuming revenue of about US$378.4 million and earnings near US$31.9 million by 2029, so this earnings jump and dividend may either strengthen that upbeat view or prompt a rethink of how reliable such long term forecasts really are.

Explore 2 other fair value estimates on DorianG - why the stock might be worth as much as $33.33!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your DorianG research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free DorianG research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate DorianG's overall financial health at a glance.

Searching For A Fresh Perspective?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- The latest GPUs need a type of rare earth metal called Terbium and there are only 27 companies in the world exploring or producing it. Find the list for free.

- Find 48 companies with promising cash flow potential yet trading below their fair value.

- Capitalize on the AI infrastructure supercycle with our selection of the 46 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.