Why Element Solutions (ESI) Is Up 9.7% After Specialty Demand And Integrations Bolster Margins

Element Solutions Inc ESI | 0.00 |

- In recent months, Element Solutions Inc reported solid quarterly results, with strong demand for its specialty chemicals across electronics and industrial coatings and benefits from recent integrations and investments that broadened its product offerings and supported margin expansion.

- An interesting angle is how investor commentary highlights these integrations as unlocking incremental earnings from higher-growth specialty businesses, suggesting the business mix is shifting toward areas with potentially stronger profitability.

- We’ll now examine how this progress on specialty chemicals demand and product integrations could reshape Element Solutions’ existing investment narrative.

Explore 29 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

Element Solutions Investment Narrative Recap

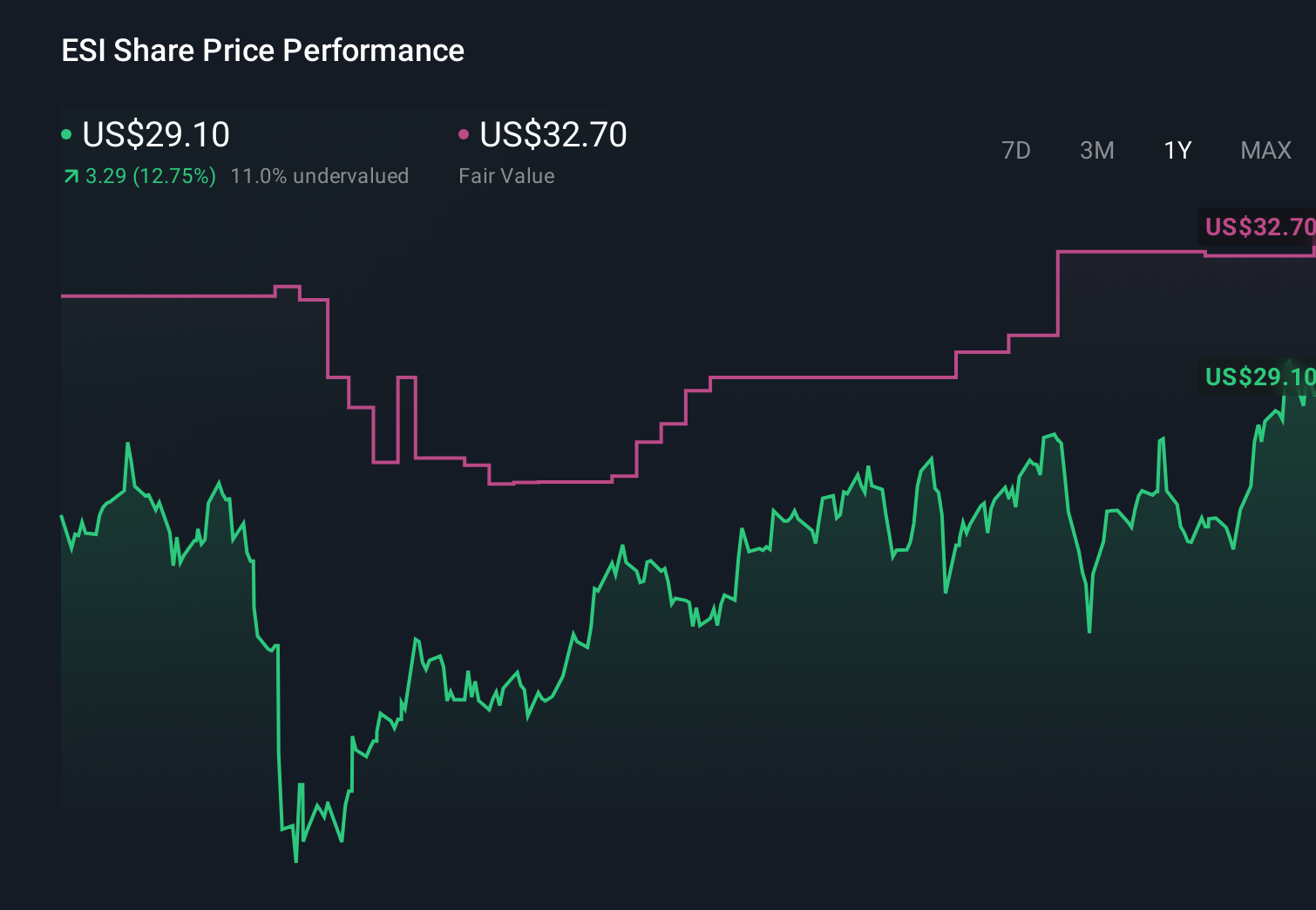

To own Element Solutions, you need to believe in its shift toward higher value specialty chemicals in electronics and industrial coatings, while accepting exposure to cyclical end markets and margin pressure from global competitors. The latest strong quarter supports the near term catalyst of mix improvement and integration benefits, but the share price pullback and valuation concerns highlight that execution risk and end market volatility remain central issues rather than being materially changed by this update.

The Q1 2026 earnings release, showing solid sales of US$840.0 million and healthy electronics demand, ties directly to the story of portfolio optimization and margin expansion through integrations. At the same time, the recent share price weakness and premium valuation multiples keep the focus on how much of this integration progress is already reflected in expectations and what happens if cyclical electronics demand softens.

Yet investors should also weigh how quickly intensifying competition in specialty chemicals could blunt Element Solutions’ pricing power and...

Element Solutions’ narrative projects $4.2 billion revenue and $549.5 million earnings by 2029. This requires 14.5% yearly revenue growth and about a $400.8 million earnings increase from $148.7 million today.

Uncover how Element Solutions' forecasts yield a $47.30 fair value, a 8% upside to its current price.

Exploring Other Perspectives

Two fair value estimates from the Simply Wall St Community span roughly US$41.07 to US$47.30 per share, showing how far apart individual views can be. You can compare these with the current focus on integration driven margin expansion and decide how much cyclical end market risk you are comfortable with.

Explore 2 other fair value estimates on Element Solutions - why the stock might be worth 6% less than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Element Solutions research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

- Our free Element Solutions research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Element Solutions' overall financial health at a glance.

Seeking Other Investments?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Capitalize on the AI infrastructure supercycle with our selection of the 48 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

- We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.