Why F.N.B (FNB) Is Down 7.3% After Inflation Jitters Spark Sector-Wide Credit Risk Fears

F.N.B. Corporation FNB | 16.86 | -0.24% |

- In late February 2026, F.N.B. Corporation faced pressure alongside other banks after hotter-than-expected US producer inflation data and growing credit risk concerns reduced investors’ confidence in rate-cut prospects and the sector’s loan quality.

- At the same time, F.N.B. was named to TIME’s list of America’s Best Financial Services 2026 and collected 14 Crisil Coalition Greenwich Best Bank Awards, underscoring its reputation for client-focused commercial banking despite these macroeconomic headwinds.

- We’ll now examine how worries about sticky inflation and credit risk may reshape F.N.B.’s investment narrative and medium-term outlook.

Capitalize on the AI infrastructure supercycle with our selection of the 34 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

F.N.B Investment Narrative Recap

To own F.N.B., you need to be comfortable with a regional bank whose story hinges on disciplined credit, steady earnings and controlled expansion in its Mid Atlantic and Southeast footprint. The latest inflation surprise and renewed credit worries primarily reinforce what is already the key near term swing factor for F.N.B. right now: how its loan book, especially commercial and CRE exposures, holds up if funding costs stay higher for longer. So far, the impact on that thesis looks more sentiment driven than fundamental.

Against that backdrop, F.N.B.’s recognition on TIME’s America’s Best Financial Services 2026 list and its 14 Crisil Coalition Greenwich Best Bank Awards matter because they speak directly to its core commercial banking franchise. Strong client relationships and service to small business and middle market borrowers sit at the heart of any case for F.N.B., given that relationship depth can influence both credit performance and pricing power if the rate and credit cycles stay challenging.

Yet, despite these strengths, investors should still watch how F.N.B. manages its exposure to commercial real estate and...

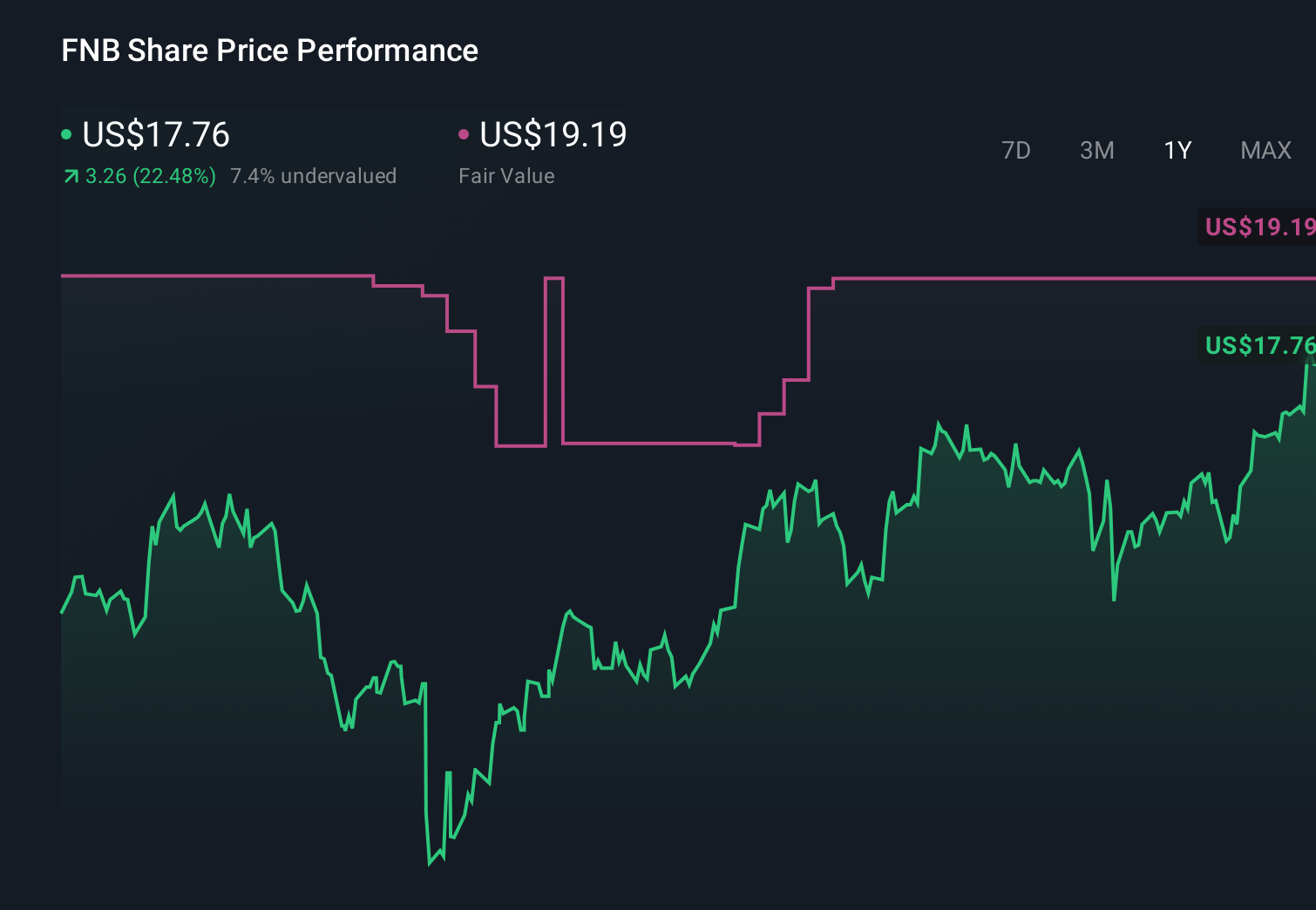

F.N.B's narrative projects $2.2 billion revenue and $775.6 million earnings by 2028. This requires 13.0% yearly revenue growth and a $308.6 million earnings increase from $467.0 million today.

Uncover how F.N.B's forecasts yield a $20.06 fair value, a 18% upside to its current price.

Exploring Other Perspectives

Four Simply Wall St Community fair value estimates for F.N.B. span from US$20.06 to US$63.31, showing how far apart individual views can be. As you weigh these opinions, remember that concerns about sticky inflation and credit risk are front and center for the bank and could prove important for how its performance evolves over time.

Explore 4 other fair value estimates on F.N.B - why the stock might be worth over 3x more than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your F.N.B research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

- Our free F.N.B research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate F.N.B's overall financial health at a glance.

Searching For A Fresh Perspective?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Uncover the next big thing with 30 elite penny stocks that balance risk and reward.

- AI is about to change healthcare. These 27 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 22 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.