Why Gartner (IT) Is Up 5.9% After Raising Guidance And Accelerating Share Buybacks – And What's Next

Gartner, Inc. IT | 0.00 |

- Earlier this year, Gartner reported a strong first quarter, beating analyst EPS expectations, lifting full-year adjusted EBITDA, adjusted EPS and free cash flow guidance, and repurchasing about US$535,000,000 of stock amid demand for digital transformation insights.

- Beyond the headline beat, the combination of upgraded guidance and sizeable buybacks underlines management’s conviction in the durability of Gartner’s research-focused business model.

- Next, we’ll examine how Gartner’s upgraded full-year guidance and substantial share repurchases influence its existing investment narrative and risk profile.

Capitalize on the AI infrastructure supercycle with our selection of the 51 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Gartner Investment Narrative Recap

To own Gartner, you need to believe its subscription research and advisory model can stay essential as enterprises wrestle with complex technology decisions, especially around AI and digital transformation. The latest quarter’s EPS beat and higher full year guidance support that view, but they do not erase the key near term catalyst and risk: whether contract value growth can re accelerate while generative AI tools and tighter client budgets test demand for paid insights.

Among recent announcements, the US$600,000,000 increase in the share repurchase authorization in April stands out alongside the US$535,000,000 of Q1 buybacks. Together, they frame the upgraded guidance in a capital allocation context that matters for the thesis: if Gartner can sustain strong free cash flow while investing in offerings like AskGartner, buybacks may cushion earnings per share even if contract value growth remains under pressure.

Yet beneath the upbeat guidance, investors should be aware of how rising free AI tools could undercut Gartner’s pricing power and...

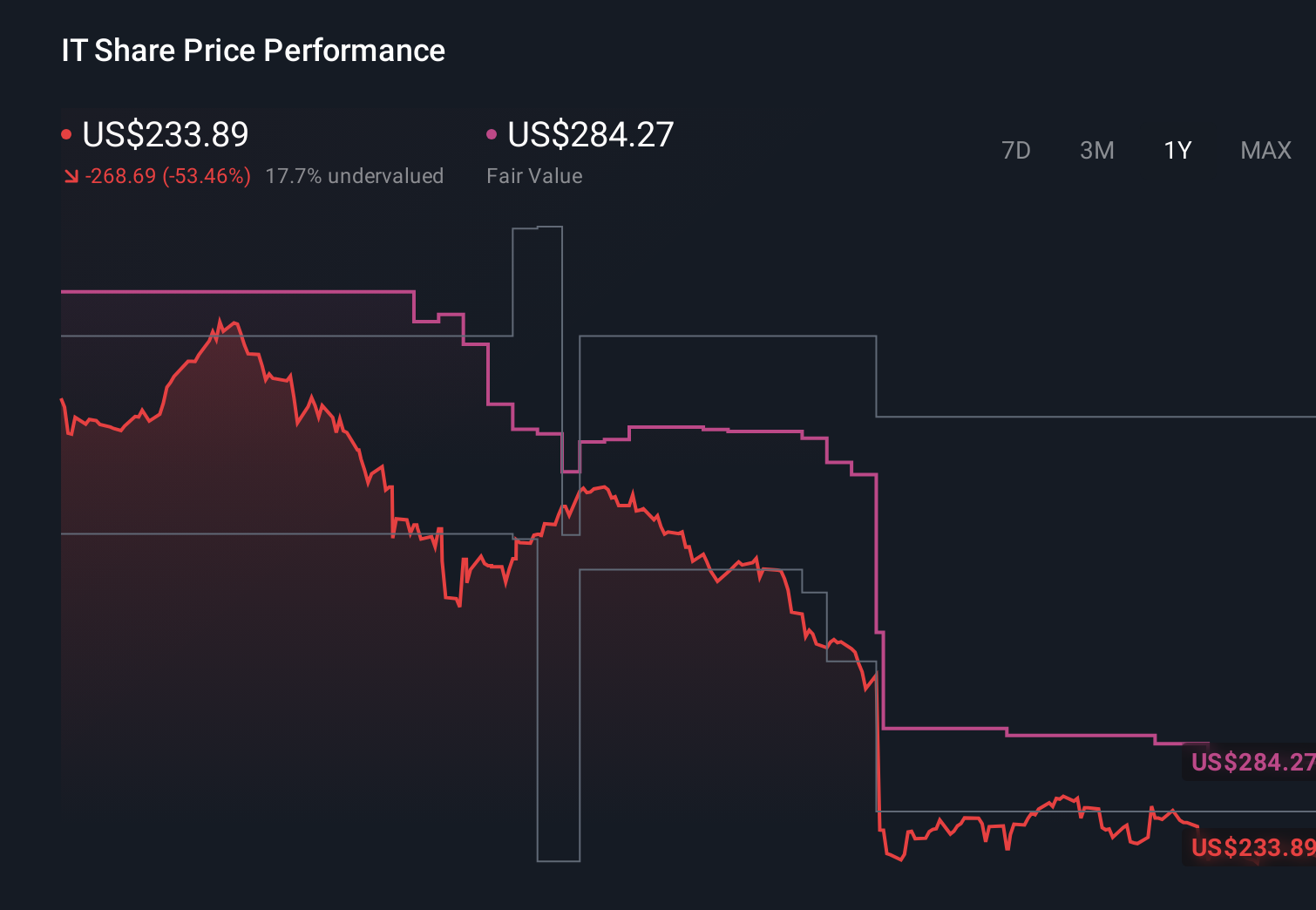

Gartner's narrative projects $7.2 billion revenue and $963.3 million earnings by 2029. This requires 3.7% yearly revenue growth and about a $234.1 million earnings increase from $729.2 million today.

Uncover how Gartner's forecasts yield a $183.69 fair value, a 36% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were already cautious, assuming revenue growth of about 1.8 percent and earnings near US$906.7 million by 2029, so this Q1 beat may prompt you to reassess how seriously you take their more pessimistic view on AI driven competitive pressure versus the more optimistic capital return story.

Explore 5 other fair value estimates on Gartner - why the stock might be worth just $140.00!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Gartner research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Gartner research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Gartner's overall financial health at a glance.

Interested In Other Possibilities?

Our top stock finds are flying under the radar-for now. Get in early:

- We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- This technology could replace computers: discover 30 stocks that are working to make quantum computing a reality.

- The future of work is here. Discover the 29 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.