Why General Dynamics (GD) Is Up 10.4% After Raising 2026 EPS Outlook On Record Defense Backlog

General Dynamics Corporation GD | 0.00 |

- General Dynamics Corporation has already reported first-quarter 2026 results, posting revenue of US$13.48 billion and net income of US$1.13 billion, with diluted EPS from continuing operations of US$4.10, all higher than a year earlier.

- The company paired this earnings beat with a raised full-year EPS outlook and record backlog underpinned by strong order intake and heightened global defense demand.

- We’ll now examine how this combination of raised earnings guidance and record backlog reshapes General Dynamics’ existing investment narrative and risk balance.

AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

General Dynamics Investment Narrative Recap

To own General Dynamics, you need to believe in sustained demand for defense platforms and Gulfstream jets, with record backlog and raised EPS guidance reinforcing that visibility. The key near term catalyst remains converting the US$130.8 billion backlog into profitable revenue, especially in Marine and Aerospace. The biggest current risk is execution and supply chain reliability in shipyards and key programs; this quarter’s strength does not remove that operational exposure, but it does not materially increase it either.

The first quarter 2026 earnings release is the most relevant update here, with revenue of US$13.48 billion, diluted EPS of US$4.10, and a consolidated 2 to 1 book to bill driving record backlog. This order momentum directly supports the backlog driven catalyst in Marine Systems and Aerospace, but also raises the stakes on the company’s ability to stabilize suppliers and facilities so that these long term contracts translate into consistent margins.

Yet against this strong order momentum, investors should still be aware of ongoing supply chain and shipyard execution risks that could...

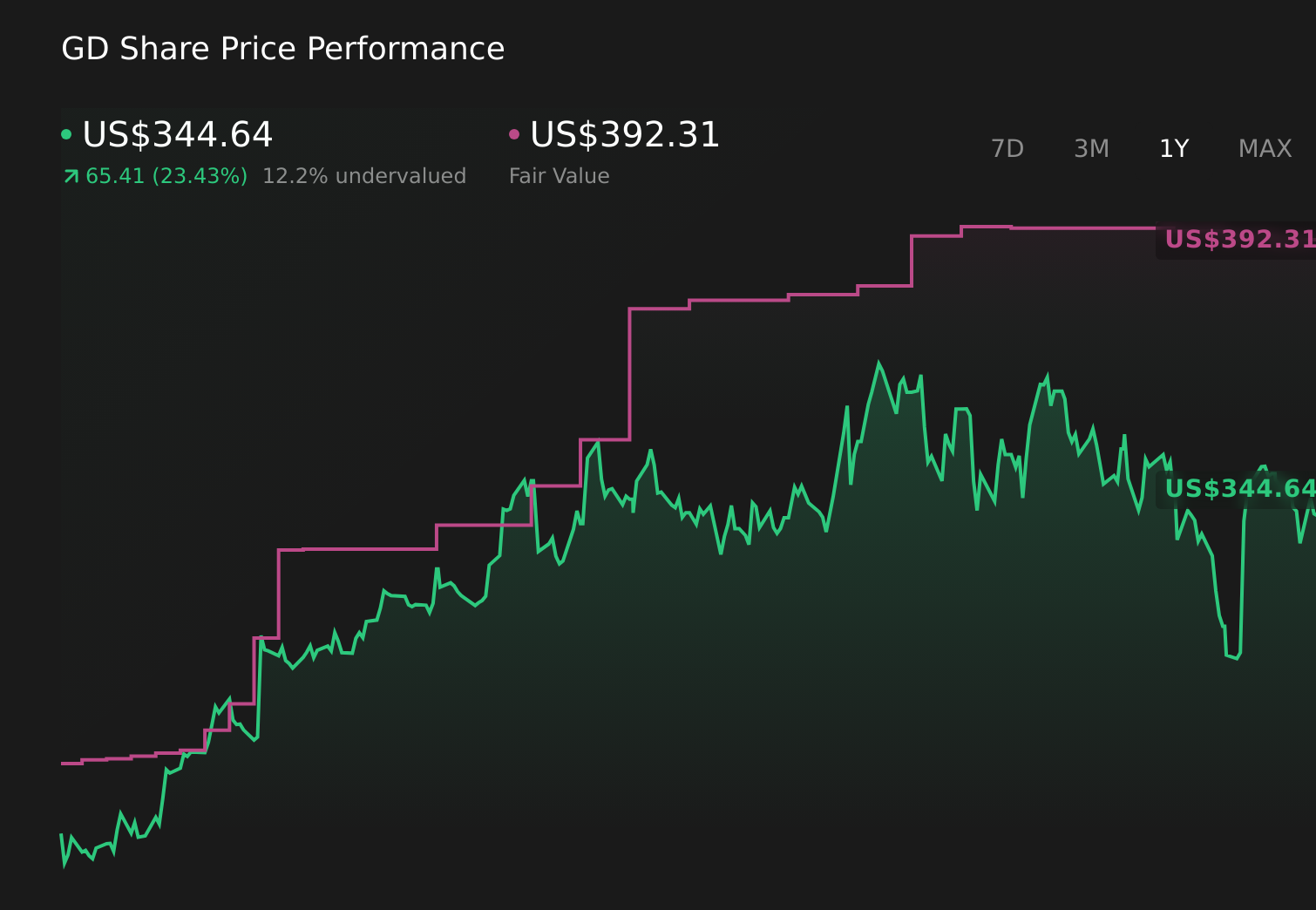

General Dynamics' narrative projects $59.7 billion revenue and $5.2 billion earnings by 2029. This requires 4.3% yearly revenue growth and about a $1.0 billion earnings increase from $4.2 billion today.

Uncover how General Dynamics' forecasts yield a $393.07 fair value, a 14% upside to its current price.

Exploring Other Perspectives

Three fair value estimates from the Simply Wall St Community cluster between US$393.07 and US$404.62, suggesting a relatively tight band of individual views. You should weigh this against the record US$130.8 billion backlog and raised EPS outlook, which together underline how strongly future performance may depend on General Dynamics converting orders into reliable, timely deliveries.

Explore 3 other fair value estimates on General Dynamics - why the stock might be worth just $393.07!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your General Dynamics research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

- Our free General Dynamics research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate General Dynamics' overall financial health at a glance.

Ready For A Different Approach?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 17 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.