Why GoDaddy (GDDY) Is Down 13.5% After Analyst Downgrade On AI, Growth And Leverage Concerns

GoDaddy, Inc. Class A GDDY | 83.43 | +0.74% |

- Recently, an analyst downgraded GoDaddy, citing accelerating disruption in its core markets, slowing revenue and bookings growth, limited visible benefits from its AI products, and rising leverage linked to aggressive share repurchases.

- The downgrade also highlighted that some competitors, such as Wix, appear better positioned in terms of growth and AI adoption, sharpening questions about GoDaddy’s competitive standing in key segments.

- Next, we’ll explore how concerns about slowing growth and rising leverage could reshape GoDaddy’s previously optimistic investment narrative built around AI and SaaS expansion.

We've uncovered the 14 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

GoDaddy Investment Narrative Recap

To own GoDaddy today, you need to believe its domain, hosting and SaaS tools can stay relevant despite growing competition and slowing growth. The recent downgrade directly targets that belief, arguing that weaker bookings, limited visible AI traction and higher leverage from buybacks now make execution on AI and SaaS the key near term catalyst, while rising debt levels and relative underperformance versus peers are the most important risk to watch in the short term.

Against this backdrop, GoDaddy’s sizeable share repurchase program is particularly relevant. The company has bought back more than 5.8 million shares for about US$832.7 million under its 2025 plan, on top of US$3.3 billion repurchased under the prior program. While these actions support per share metrics, the downgrade’s focus on higher leverage means investors may now view buybacks less as a simple capital return catalyst and more as part of the risk discussion.

Yet, investors should also be aware of how rising debt and weaker growth trends could interact with intensifying competition from AI enabled rivals in ways that...

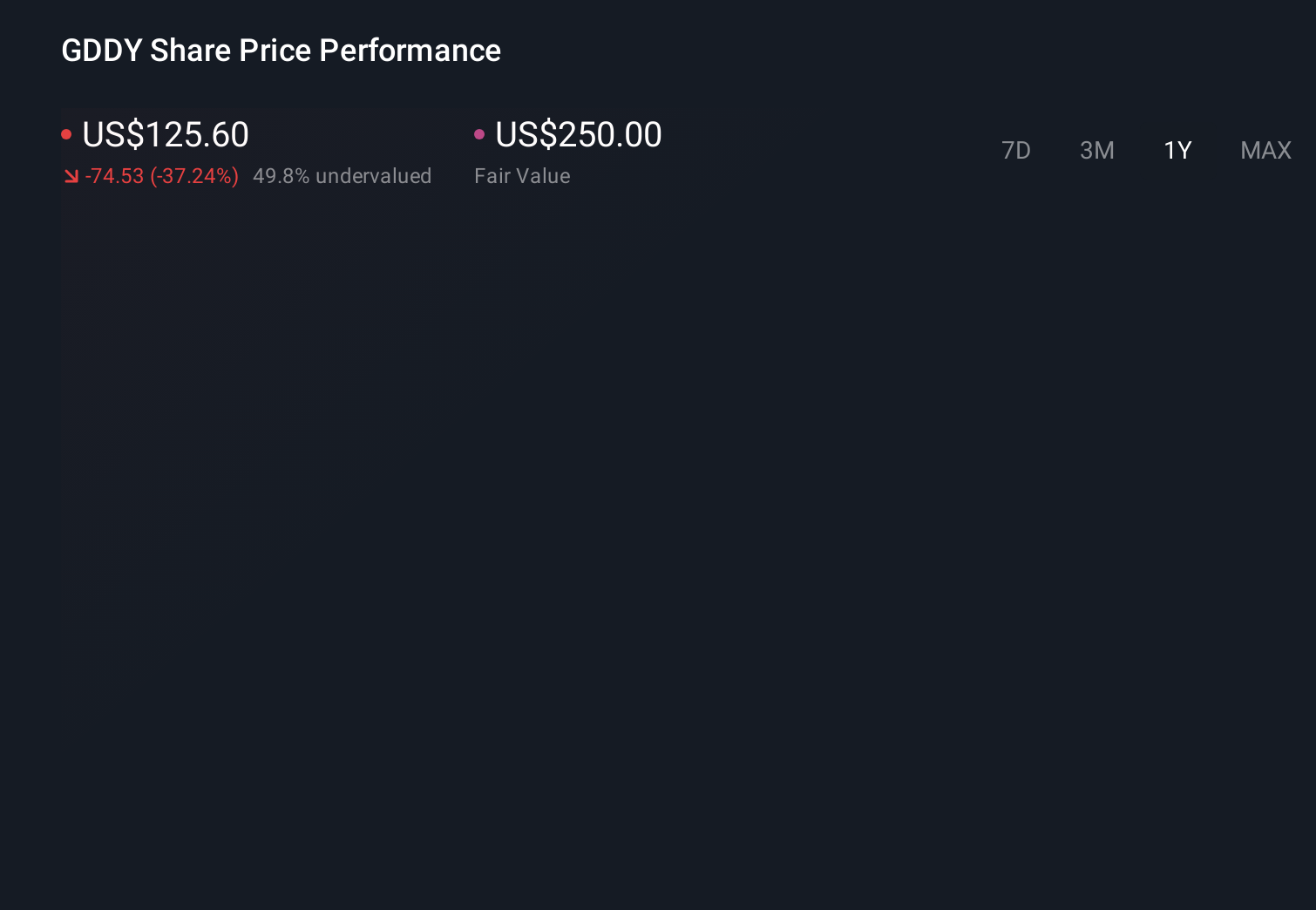

GoDaddy's narrative projects $5.9 billion revenue and $1.3 billion earnings by 2028. This requires 7.7% yearly revenue growth and roughly a $0.5 billion earnings increase from $808.5 million today.

Uncover how GoDaddy's forecasts yield a $119.43 fair value, a 47% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were expecting GoDaddy to reach about US$6.2 billion of revenue and US$1.5 billion of earnings by 2028, yet these fresh concerns about disruption and leverage show how far expectations can swing and why you should compare this bullish view with the risk that advanced AI tools outside GoDaddy’s ecosystem could steadily chip away at its traditional domain and hosting franchise.

Explore 4 other fair value estimates on GoDaddy - why the stock might be worth just $119.43!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your GoDaddy research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free GoDaddy research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate GoDaddy's overall financial health at a glance.

Ready For A Different Approach?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Capitalize on the AI infrastructure supercycle with our selection of the 35 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Find 48 companies with promising cash flow potential yet trading below their fair value.

- AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.