Why Harrow (HROW) Is Down 25.9% After Q1 Miss And Reaffirmed 2026 Guidance – And What's Next

Harrow, Inc. HROW | 0.00 |

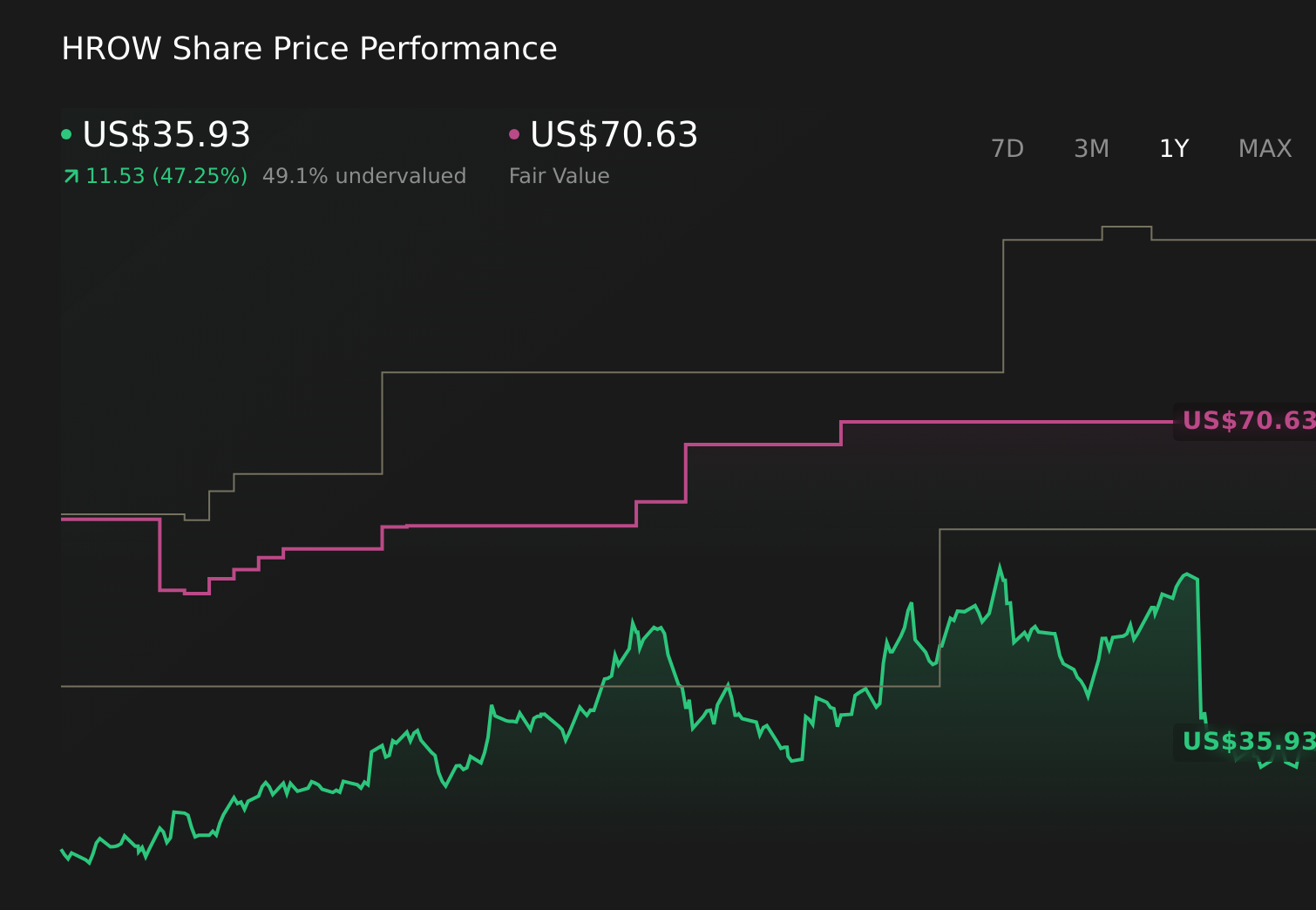

- Harrow, Inc. reported past first-quarter 2026 results with revenue of US$44.2 million versus US$47.83 million a year earlier and a wider net loss of US$27.6 million, missing analyst expectations on both revenue and earnings.

- Management attributed much of the revenue pressure to an US$8 million non-recurring VEVYE gross-to-net adjustment while highlighting record VEVYE prescriptions and reaffirming full-year 2026 revenue guidance of US$350 million to US$365 million.

- We’ll now examine how reaffirmed full-year guidance despite the VEVYE-related earnings miss may influence Harrow’s existing investment narrative.

This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

Harrow Investment Narrative Recap

To own Harrow, you need to believe its ophthalmic portfolio, led by VEVYE, can translate strong prescription trends into sustainable revenue while narrowing losses. The key near term catalyst is execution against reaffirmed 2026 revenue guidance after a weak first quarter. The biggest current risk is that heavy dependence on a few flagship products amplifies the impact of any pricing, reimbursement, or volume hiccups. The latest VEVYE gross to net hit is material to that risk, but does not yet redefine it.

The most relevant recent announcement is Harrow’s decision to reaffirm full year 2026 revenue guidance of US$350 million to US$365 million and provide Q2 guidance of US$71 million to US$81 million, despite the Q1 miss. This keeps the spotlight firmly on whether accelerating demand for VEVYE, IHEEZO, and TRIESENCE can offset reimbursement and mix pressures highlighted in Q1, and whether management can deliver the step up implied for the second half of the year.

Yet beneath the reaffirmed guidance, there is an important risk around pricing and reimbursement that investors should be aware of...

Harrow’s narrative projects $586.7 million revenue and $209.0 million earnings by 2028.

Uncover how Harrow's forecasts yield a $70.62 fair value, a 137% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were already more cautious, assuming revenue near US$694.2 million and earnings of about US$136.6 million by 2029, and Q1’s VEVYE driven shortfall may reinforce their concern that heavy dependence on a few ophthalmic launches could make Harrow’s path to those numbers bumpier than consensus expects.

Explore 3 other fair value estimates on Harrow - why the stock might be worth over 10x more than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Harrow research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Harrow research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Harrow's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Uncover the next big thing with 28 elite penny stocks that balance risk and reward.

- Capitalize on the AI infrastructure supercycle with our selection of the 39 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- We've uncovered the 14 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.