Why Harrow (HROW) Is Down 6.5% After Raising 2026 Guidance And Advancing TRIESENCE To Phase 3

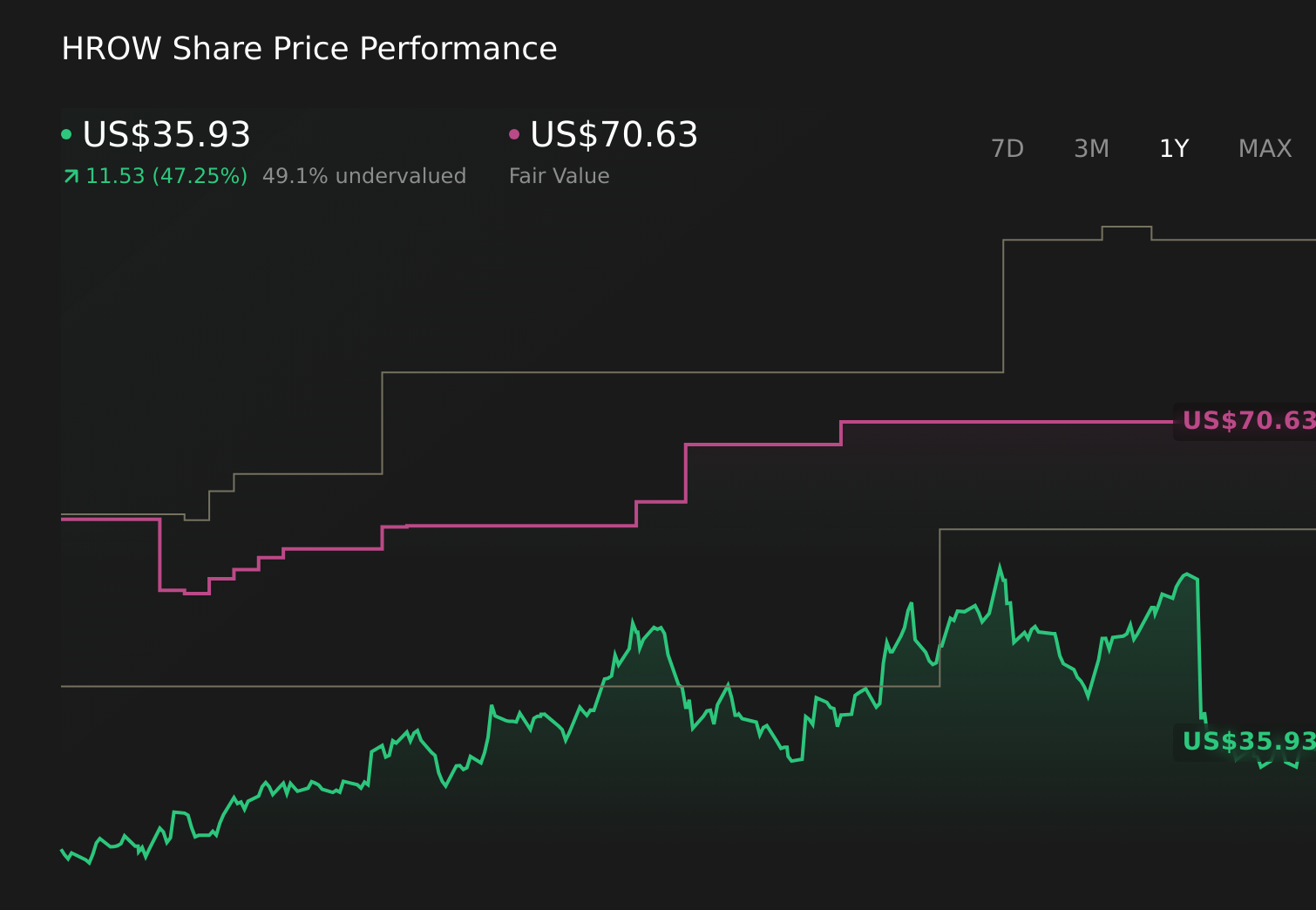

Harrow, Inc. HROW | 35.43 36.30 | +0.85% +2.44% Post |

- Harrow, Inc. recently reported fourth-quarter 2025 sales of US$89.09 million and full-year 2025 revenue of US$272.30 million, issued 2026 revenue guidance of US$350 million to US$365 million, and received FDA clearance of an IND to run a Phase 3 trial of TRIESENCE for ocular inflammation and pain after cataract surgery.

- The combination of strong recent revenue performance, ambitious 2026 guidance, and progress toward potentially broadening TRIESENCE’s on-label cataract surgery use has sharpened investor focus on Harrow’s position in the ophthalmic pharmaceutical market.

- We’ll now examine how the planned Phase 3 TRIESENCE trial for post-cataract inflammation could reshape Harrow’s investment narrative and risk profile.

AI is about to change healthcare. These 32 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Harrow Investment Narrative Recap

To own Harrow, you need to believe it can turn its ophthalmic focus and current product base into durable, profitable growth while managing its reliance on a few key drugs. The new Phase 3 TRIESENCE trial is now a central short term catalyst, because positive data could support broader cataract use, while trial failure or delay has become a prominent risk alongside execution against Harrow’s ambitious 2026 revenue guidance.

The FDA’s IND clearance for a Phase 3 trial of TRIESENCE in post cataract inflammation and pain is the announcement that most clearly ties into this catalyst. It directly tests whether Harrow can extend TRIESENCE’s on label role in one of the largest ophthalmic procedures in the US, which could influence how investors view the company’s dependence on VEVYE, IHEEZO, and TRIESENCE for future revenue concentration and reimbursement exposure.

Yet investors should also keep in mind the heightened reliance on successful TRIESENCE outcomes and what happens if the Phase 3 data or timelines do not...

Harrow's narrative projects $586.7 million revenue and $209.0 million earnings by 2028.

Uncover how Harrow's forecasts yield a $70.62 fair value, a 96% upside to its current price.

Exploring Other Perspectives

Before this news, the most optimistic analysts were modeling revenue of about US$700.7 million and earnings near US$265.1 million by 2028, so compared with the baseline focus on execution and product concentration risk, that higher bar reflects a far more optimistic view that the cataract franchise and broader portfolio could outperform, and you should recognize that your own expectations might land very differently from those extremes.

Explore 4 other fair value estimates on Harrow - why the stock might be worth just $51.17!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Harrow research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Harrow research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Harrow's overall financial health at a glance.

Looking For Alternative Opportunities?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Uncover the next big thing with 28 elite penny stocks that balance risk and reward.

- Invest in the nuclear renaissance through our list of 86 elite nuclear energy infrastructure plays powering the global AI revolution.

- Rare earth metals are the new gold rush. Find out which 29 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.