Why Hyliion Holdings (HYLN) Is Down 17.9% After Short Seller Questions Key Sales Pipeline Deal

Hyliion Holdings HYLN | 0.00 |

- Recently, Hyliion Holdings came under pressure after short seller Pelican Way Research questioned whether a US$133 million letter of intent with VFG Holdings, representing roughly one-third of Hyliion’s reported sales pipeline, is backed by a customer with sufficient operational and financial substance.

- The report also criticized Hyliion’s capital allocation and relatively high executive pay against weak revenue performance, raising concerns about how much of its projected growth is supported by durable commercial relationships.

- We’ll now examine how allegations around the VFG letter of intent and Hyliion’s sales pipeline may reshape the company’s investment narrative.

AI is about to change healthcare. These 38 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Hyliion Holdings Investment Narrative Recap

To own Hyliion, you have to believe that KARNO power modules can move from R&D projects to meaningful commercial orders, especially in data centers and defense, before the current cash burn becomes problematic. The Pelican Way report goes straight at that belief by questioning whether a US$133 million VFG letter of intent, about one third of the pipeline, rests on a solid counterparty, making pipeline conversion the key near term catalyst and validation of commercial demand the central risk.

Against that backdrop, Hyliion’s May 2026 guidance reaffirming about US$10 million of 2026 revenue, mainly from R&D services and initial KARNO sales, is important context. It underlines how early the commercial ramp still is and how reliant the story remains on moving letters of intent like VFG’s into firm orders. If the VFG concerns weaken confidence in that US$400 million pipeline, investors may focus even more on smaller but better documented agreements and government programs as proof points.

Yet beneath the excitement around KARNO’s potential, concerns over whether key letters of intent will truly convert into durable revenue are information investors should be aware of...

Hyliion Holdings' narrative projects $154.7 million revenue and $18.3 million earnings by 2028. This requires 230.8% yearly revenue growth and a $76.7 million earnings increase from -$58.4 million today.

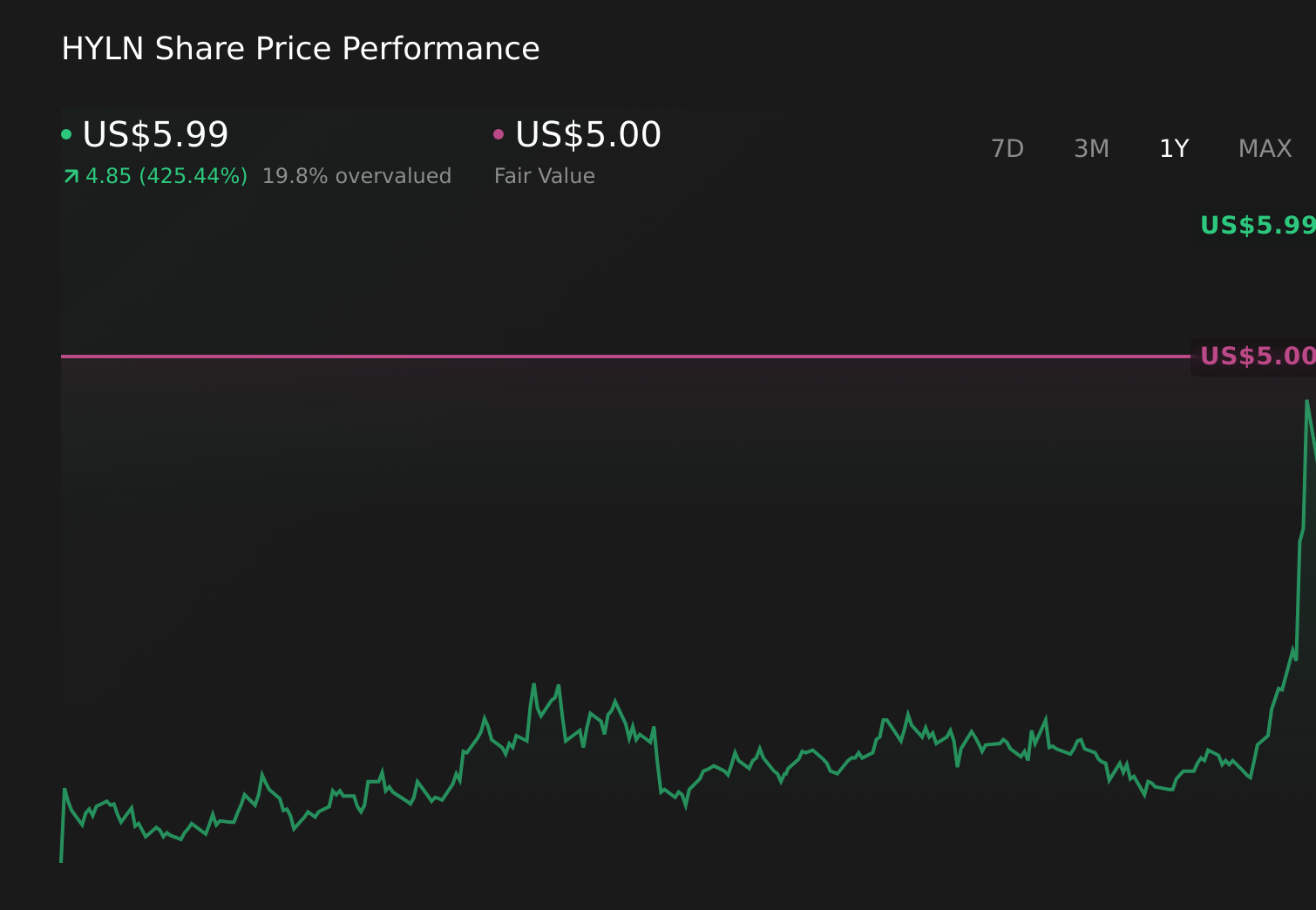

Uncover how Hyliion Holdings' forecasts yield a $5.00 fair value, a 18% downside to its current price.

Exploring Other Perspectives

Before this short seller report, the most pessimistic analysts already assumed rapid revenue growth to about US$104.7 million by 2029 but still no near term profitability, so if VFG’s 250 core letter of intent proves shakier than hoped, that more cautious view of contract risk and concentration might start to look closer to the mark.

Explore 4 other fair value estimates on Hyliion Holdings - why the stock might be worth 44% less than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Hyliion Holdings research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

- Our free Hyliion Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Hyliion Holdings' overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- The latest GPUs need a type of rare earth metal called Terbium and there are only 29 companies in the world exploring or producing it. Find the list for free.

- Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

- Find 44 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.