Why Li Auto (LI) Is Up 13.0% After April Deliveries, L9 Livis Launch Plans And Buybacks

LI Auto LI | 0.00 |

- Li Auto Inc. reported that it delivered 34,085 vehicles in April 2026 and plans to release its unaudited first-quarter 2026 financial results on May 28, 2026, alongside ongoing share repurchases under its May 2025 buyback mandate.

- The company is entering a new product cycle with the upcoming Li Auto L9 Livis launch while contending with fiercer competition, shifting from its extended-range roots toward pure electric models and AI-enabled driving features.

- We’ll now examine how the upcoming Li Auto L9 Livis launch and early signs of operational recovery may alter Li Auto’s investment narrative.

AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Li Auto Investment Narrative Recap

To own Li Auto today, you need to believe it can successfully pivot from its extended range roots to competitive pure EVs with attractive AI driving features, while managing heavy R&D spend and intense Chinese EV competition. April’s 34,085 deliveries and the imminent L9 Livis launch tie directly into the key near term catalyst of a cleaner product cycle reset, but they do little to reduce the risk that high investment and pricing pressure keep margins fragile.

The most relevant update here is Li Auto’s ongoing share repurchases under its May 2025 buyback mandate, including 331,208 shares bought on Nasdaq and 8.52 million shares cumulatively. For current shareholders, this capital allocation choice sits alongside the L9 Livis launch as a meaningful short term support for per share metrics, even as upcoming Q1 2026 results on May 28 will help clarify whether operational recovery is gaining real traction.

Yet even if the new model cycle gains traction, investors should still be aware of how rising competition and price pressure could...

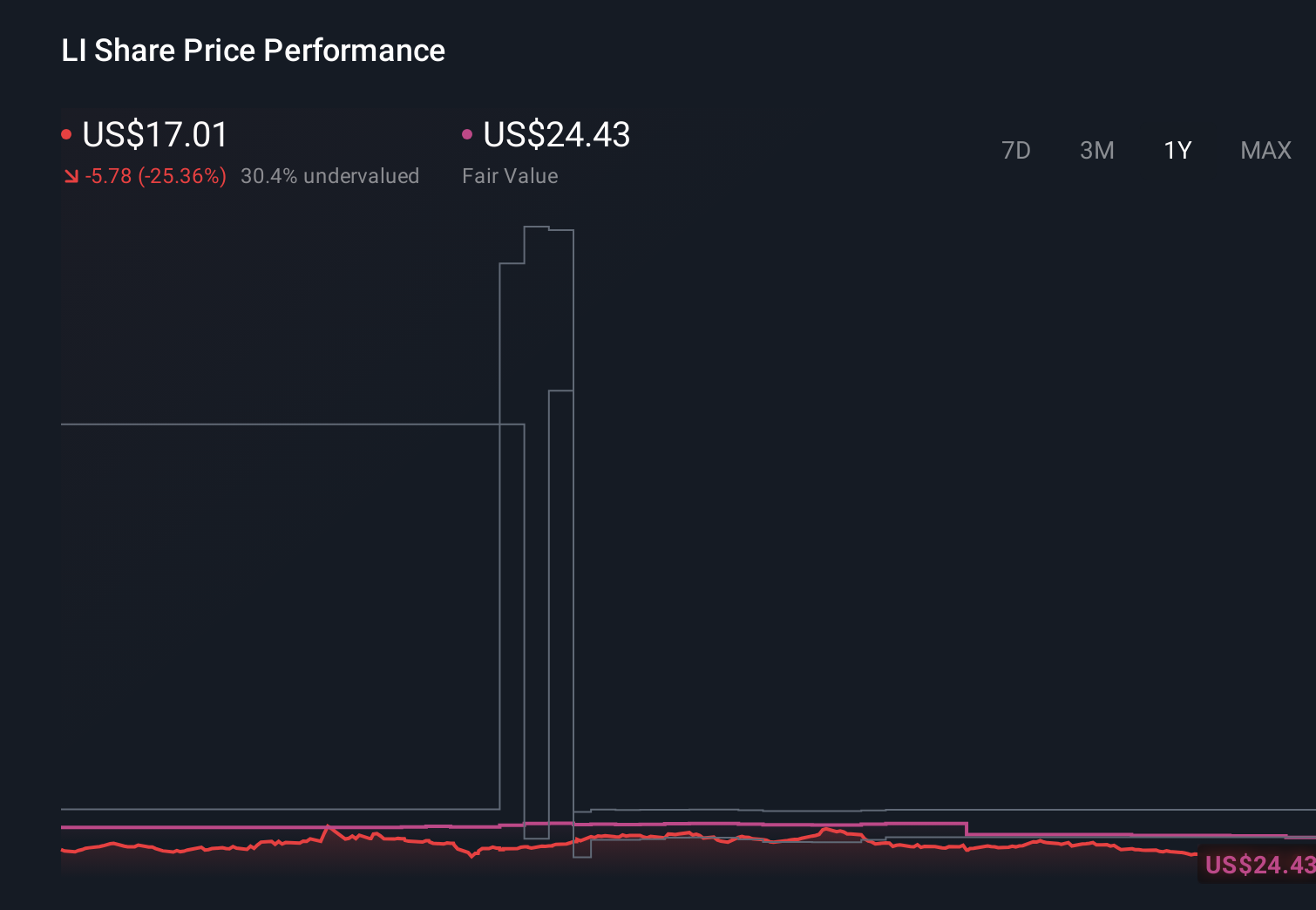

Li Auto's narrative projects CN¥167.9 billion revenue and CN¥8.1 billion earnings by 2029. This requires 14.3% yearly revenue growth and a CN¥7.0 billion earnings increase from CN¥1.1 billion today.

Uncover how Li Auto's forecasts yield a $22.16 fair value, a 11% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were already assuming only about CN¥104.3 billion in 2029 revenue and CN¥1.2 billion in earnings, painting a far more cautious picture than the consensus. Against that backdrop, April’s deliveries and the L9 Livis launch could either challenge or reinforce this pessimism, so it is worth comparing these different views before you decide which narrative fits your own expectations.

Explore 6 other fair value estimates on Li Auto - why the stock might be worth 28% less than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Li Auto research is our analysis highlighting 1 key reward and 1 important warning sign that could impact your investment decision.

- Our free Li Auto research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Li Auto's overall financial health at a glance.

Contemplating Other Strategies?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 33 best rare earth metal stocks of the very few that mine this essential strategic resource.

- Find 47 companies with promising cash flow potential yet trading below their fair value.

- The future of work is here. Discover the 31 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.