Why Life Time Group Holdings (LTH) Is Up 20.1% After Raising 2026 Guidance And Expanding Clubs

Life Time Group Holdings, Inc. LTH | 0.00 |

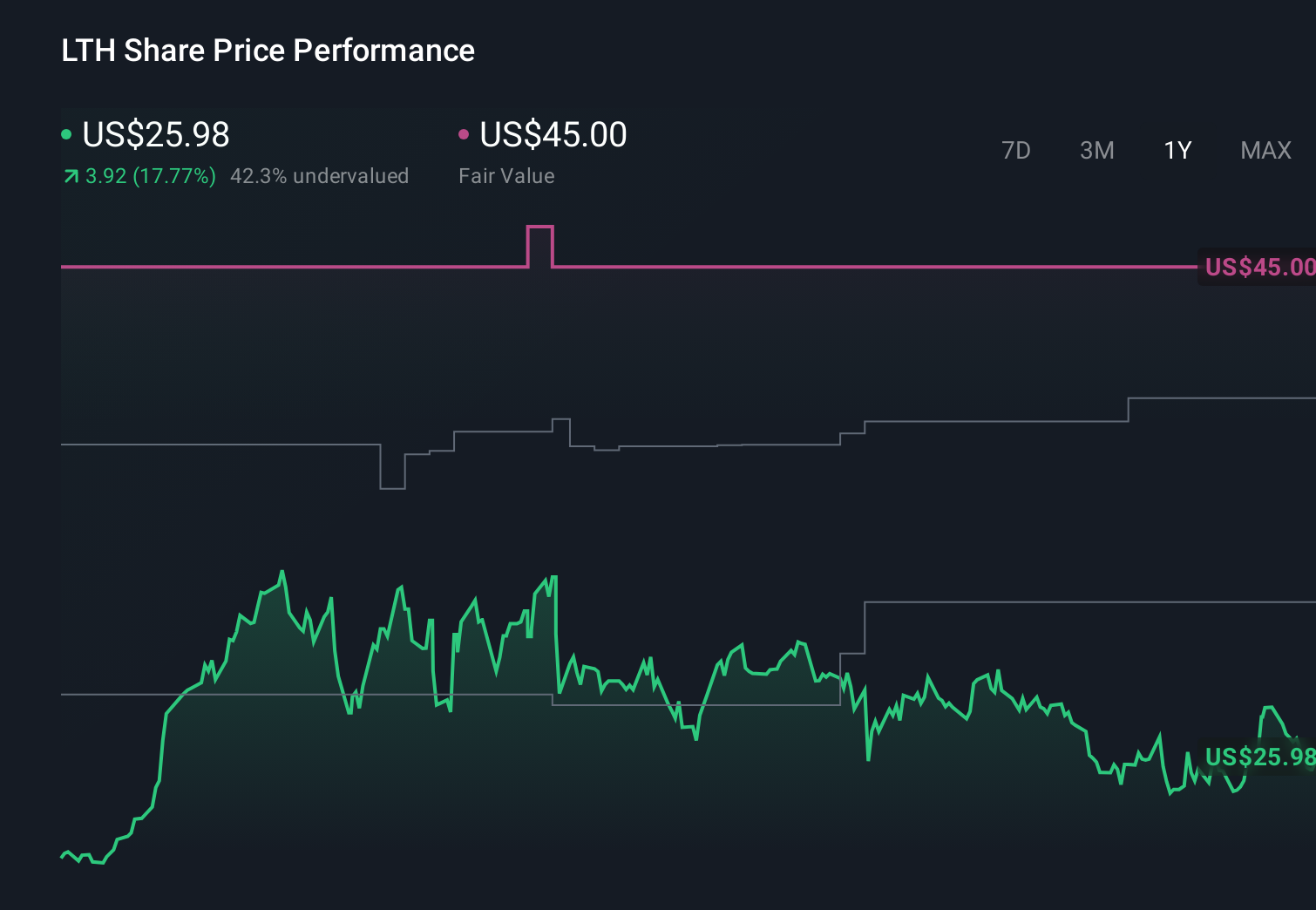

- In early May 2026, Life Time Group Holdings reported first-quarter results showing year-on-year increases in sales to US$767.57 million, total revenue to US$788.7 million, and net income to US$88.1 million, alongside higher earnings per share.

- The company also raised its full-year 2026 revenue and net income guidance, while continuing to open large-format clubs and repurchasing shares, underscoring how earnings growth, expansion, and capital allocation are moving together.

- We’ll now examine how the raised 2026 guidance, alongside accelerating large-club openings, reshapes Life Time’s previously outlined investment narrative.

AI is about to change healthcare. These 35 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Life Time Group Holdings Investment Narrative Recap

To own Life Time Group Holdings, you need to believe the company can keep filling and monetizing a growing footprint of premium, capital-intensive clubs while managing debt and real estate exposure. Right now, the key near term catalyst is execution on the 2026 club opening schedule, and the biggest risk is that heavy spending and dependence on sale leasebacks squeeze margins if financing conditions worsen. The latest results and raised guidance support the story but do not remove that funding risk.

The most relevant recent announcement is Life Time’s plan to open 12 to 14 new clubs in 2026, nearly doubling new-club square footage versus 2024 and 2025. This ties directly into both the growth catalyst and the balance sheet risk, because it raises the stakes on each project’s payback and the company’s ability to support higher rent and construction costs while still delivering on its updated US$3.32 billion to US$3.35 billion revenue outlook.

Yet investors should also weigh how quickly expansion, higher rent obligations, and any shift in sale leaseback terms could reshape that risk profile...

Life Time Group Holdings' narrative projects $4.1 billion revenue and $448.6 million earnings by 2029.

Uncover how Life Time Group Holdings' forecasts yield a $40.00 fair value, a 24% upside to its current price.

Exploring Other Perspectives

Some of the lowest estimates were already assuming revenue of about US$4.1 billion and earnings near US$419.8 million by 2029, so if you worry about expansion straining cash flow and margins, this more cautious view shows how far apart opinions can be and why fresh results like Q1 2026 may eventually shift both the bullish and bearish cases.

Explore 2 other fair value estimates on Life Time Group Holdings - why the stock might be worth less than half the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Life Time Group Holdings research is our analysis highlighting 5 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Life Time Group Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Life Time Group Holdings' overall financial health at a glance.

No Opportunity In Life Time Group Holdings?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Invest in the nuclear renaissance through our list of 91 elite nuclear energy infrastructure plays powering the global AI revolution.

- Explore 27 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Capitalize on the AI infrastructure supercycle with our selection of the 40 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.