Why Lucid Group (LCID) Is Down 6.6% After Deep Job Cuts And Leadership Shake-Up – And What's Next

Lucid LCID | 0.00 |

- In early July 2026, Lucid Group reported second-quarter production of 4,774 vehicles and deliveries of 3,953, while simultaneously announcing an 18% U.S. workforce reduction, a shift to single-shift manufacturing, and a sweeping leadership overhaul including a new Chief Financial Officer and multiple new C-suite roles.

- Beneath the headlines, Lucid is reshaping its operating model by tightening cost controls, simplifying reporting lines, and carving out a dedicated Lucid Technologies unit focused on robotaxis, AI, autonomy, and ADAS.

- We’ll now examine how this cost-cutting, leadership reset, and Lucid Technologies focus may reshape Lucid’s existing investment narrative and risks.

Explore 27 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

Lucid Group Investment Narrative Recap

To own Lucid today, you need to believe it can convert premium EV technology and the Uber/Nuro robotaxi opportunity into scale, while narrowing heavy losses and managing dilution. The latest Q2 data, headcount cuts, and shift to single-shift production all put near term focus squarely on cost control and demand health. The most important short term catalyst remains execution on high volume fleet and midsize plans, while the biggest risk is still prolonged cash burn and funding needs.

The creation of Lucid Technologies, led by a new Chief Digital Officer and focused on robotaxis, AI, autonomy, and ADAS, is especially relevant here. It ties directly into the Uber and Nuro partnership that underpins much of the long term growth case, but it also raises execution risk if the company stretches limited financial and operational resources across both capital intensive vehicle manufacturing and software heavy autonomous programs at the same time.

Yet behind Lucid’s cost cuts and tech push, there is a critical funding and dilution risk that investors should be aware of...

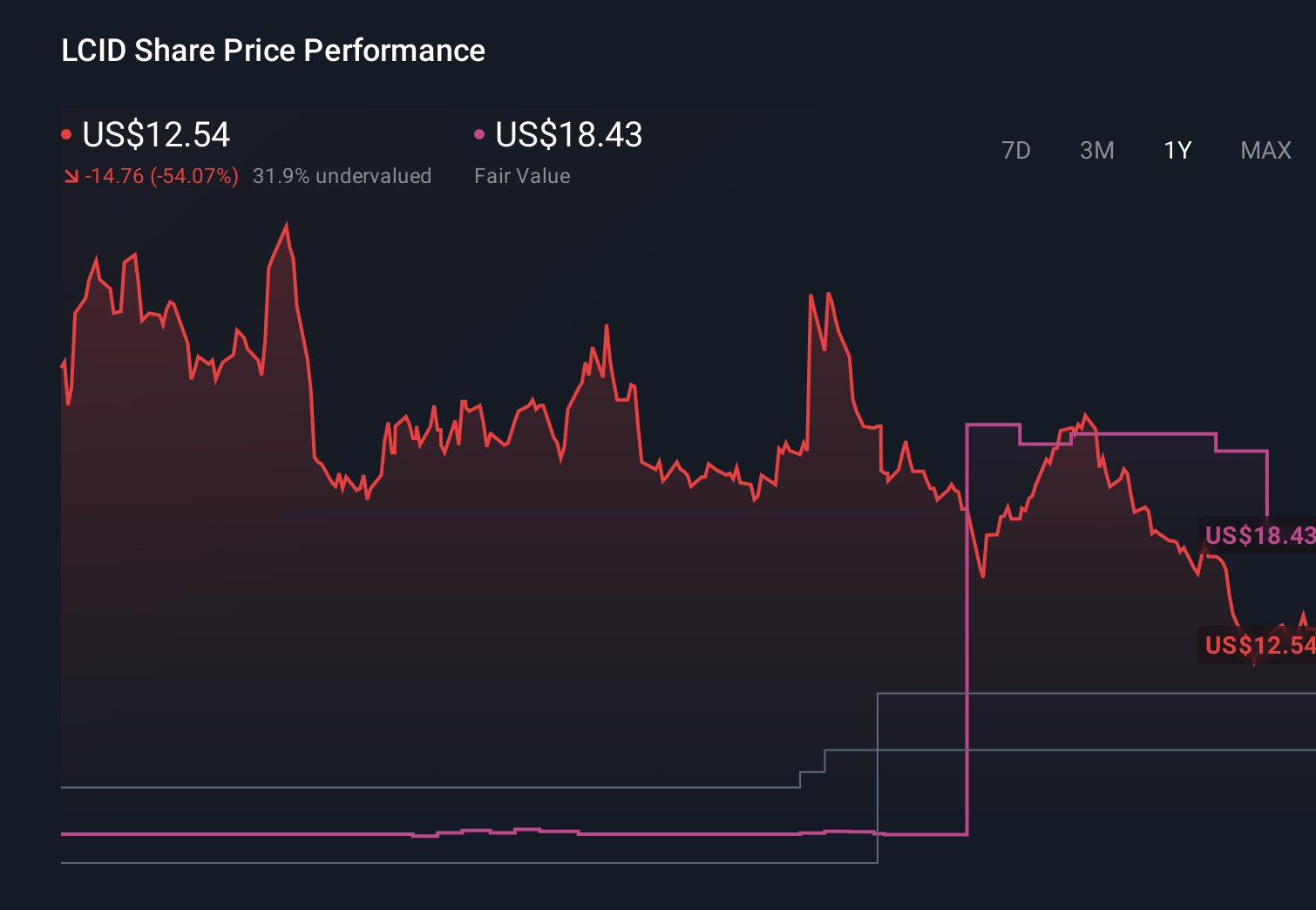

Lucid Group’s narrative projects $7.2 billion in revenue and $167.8 million in earnings by 2029.

Uncover how Lucid Group's forecasts yield a $8.40 fair value, a 38% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts paint a far tougher picture, assuming Lucid stays unprofitable and needs revenue to reach about US$4.3 billion by 2029, highlighting that while one narrative leans on robotaxi upside and tech leadership, another warns that continued cash burn and heavy dilution could still dominate the story once the latest restructuring is fully reflected.

Explore 5 other fair value estimates on Lucid Group - why the stock might be worth over 2x more than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Lucid Group research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

- Our free Lucid Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Lucid Group's overall financial health at a glance.

Curious About Other Options?

Our top stock finds are flying under the radar-for now. Get in early:

- Find 44 companies with promising cash flow potential yet trading below their fair value.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 16 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Uncover the next big thing with 20 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.