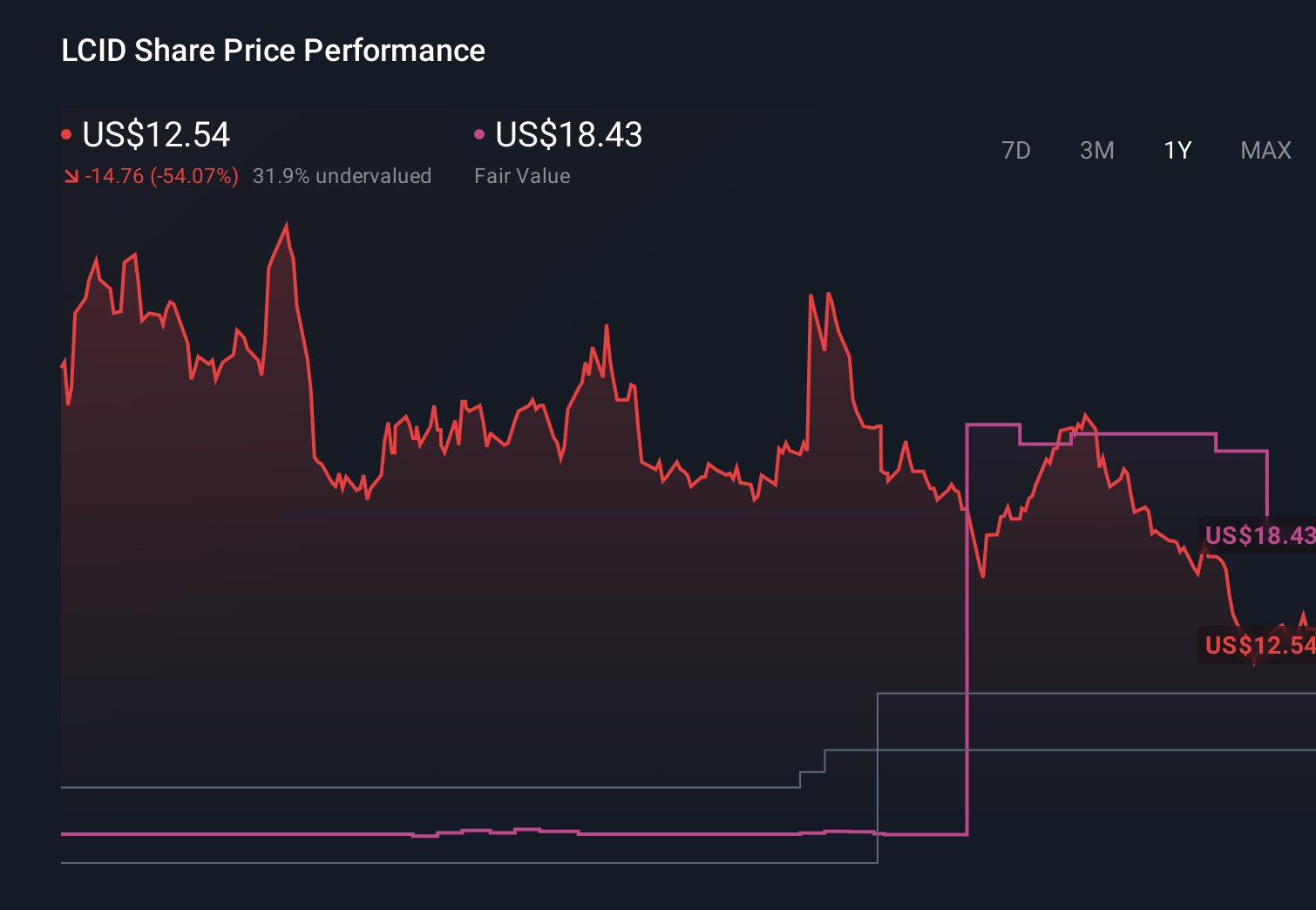

Why Lucid Group (LCID) Is Down 8.6% After CEO Shift And New Lawsuits Hit Gravity Shipments

Lucid LCID | 0.00 |

- Lucid Group has completed its CEO transition with Silvio Napoli now in charge and is facing multiple shareholder class action lawsuits alleging misleading disclosures about supplier quality and delivery issues that affected Lucid Gravity SUV shipments and financial results.

- Alongside this leadership change, Lucid is under legal scrutiny just as it pursues capital raises and operational improvements to address production challenges and ongoing losses.

- We’ll now examine how this leadership transition and legal uncertainty could influence Lucid’s investment narrative built around technology partnerships and scaling.

Find 47 companies with promising cash flow potential yet trading below their fair value.

Lucid Group Investment Narrative Recap

To own Lucid today, you have to believe that its technology, Gravity SUV ramp, and Uber/Nuro partnerships can eventually turn heavy losses into a viable, scaled EV and tech platform. The most important near term catalyst remains consistent Gravity production and delivery into those fleet commitments, while the biggest current risk is operational execution now compounded by securities class actions around alleged supplier and disclosure failures.

The CEO transition to Silvio Napoli is especially relevant here. Lucid’s board is explicitly tying his mandate to better execution, cost competitiveness, and organizational streamlining at the same time the company is raising more than US$1.0 billion of fresh capital and working through supplier quality issues on Gravity. How effectively this new leadership team stabilizes operations will feed directly into whether the Uber/Nuro robotaxi commitments become a real volume and margin driver.

Yet behind the technology story, investors should be aware that ongoing lawsuits over alleged Gravity delivery disclosures could still...

Lucid Group’s narrative projects $6.9 billion revenue and $157.5 million earnings by 2029.

Uncover how Lucid Group's forecasts yield a $12.77 fair value, a 123% upside to its current price.

Exploring Other Perspectives

Before this news, the most optimistic analysts were banking on about 94 percent annual revenue growth and future earnings of roughly US$229 million, but the new lawsuits and Gravity delivery issues show how quickly that upbeat story can be challenged, so you should compare these bullish assumptions with more cautious views and decide where you sit on that spectrum.

Explore 6 other fair value estimates on Lucid Group - why the stock might be worth 13% less than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Lucid Group research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

- Our free Lucid Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Lucid Group's overall financial health at a glance.

Contemplating Other Strategies?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Capitalize on the AI infrastructure supercycle with our selection of the 48 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 13 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.