Why Lululemon (LULU) Is Down 17.0% After Lowering Guidance on Weaker U.S. Demand and Tariffs

lululemon athletica inc. LULU | 155.72 | -1.95% |

- In the past week, lululemon athletica released its second quarter results, reporting US$2.53 billion in revenue and adjusted earnings per share that exceeded expectations, but also lowered its full-year guidance due to weak U.S. demand and increased tariffs.

- Alongside these financial updates, the company announced executive leadership changes and an expanded focus on technology and AI to help reinvigorate growth and address ongoing challenges in its product lineup.

- We'll now look at how Lululemon's revised outlook and tariff concerns may influence its previously optimistic global growth and earnings narrative.

Find companies with promising cash flow potential yet trading below their fair value.

lululemon athletica Investment Narrative Recap

To be a lululemon athletica shareholder right now, you need to believe in the company’s ability to drive growth through international expansion and product innovation, even while U.S. sales and tariff pressures create short-term headwinds. The latest earnings release lowered full-year guidance, which directly impacts the company's biggest near-term catalyst, U.S. revenue stabilization, and highlights that deteriorating domestic demand remains the most immediate risk to the business.

The recent appointment of Ranju Das as Chief AI & Technology Officer stands out, as his leadership could accelerate lululemon’s push toward improved product development and personalized customer experiences. This aligns with the company's identified need for greater agility in addressing shifting consumer preferences, which is key for any rebound in the U.S. market or capturing new international opportunities.

Yet, in contrast to previous expectations, investors should be aware of the potential for elevated tariffs to significantly impact lululemon’s profit margins if mitigation efforts fall short…

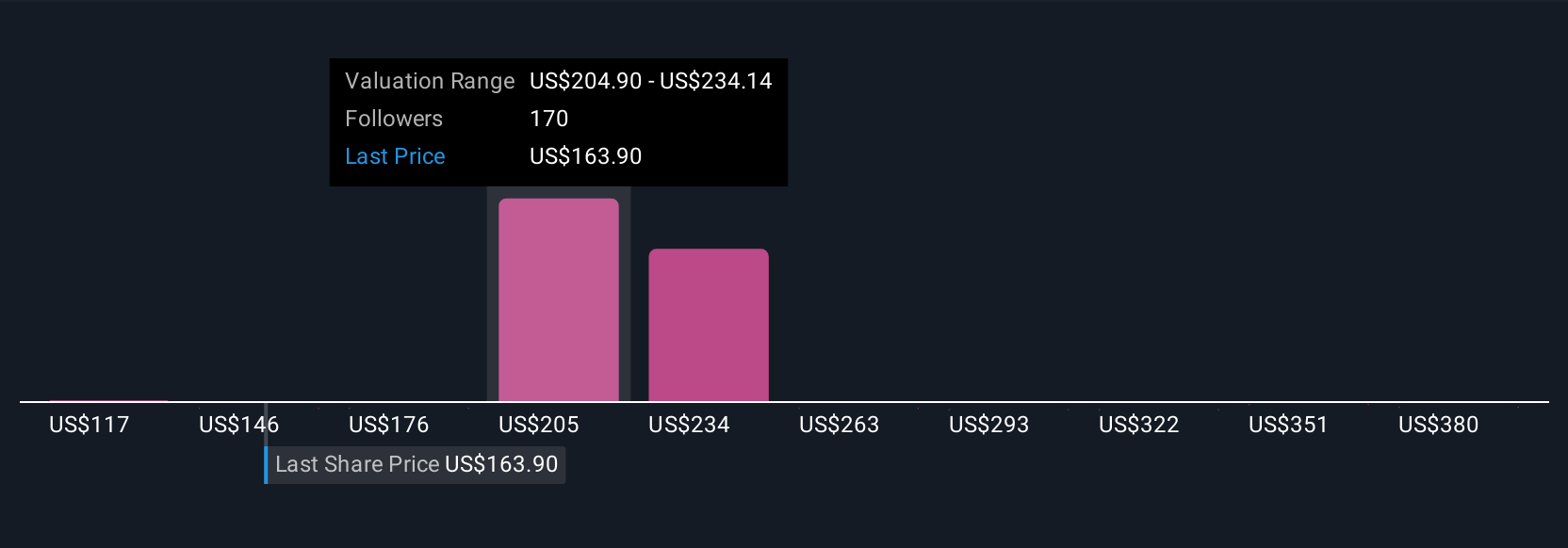

lululemon athletica's outlook anticipates $12.9 billion in revenue and $2.0 billion in earnings by 2028. Achieving these targets requires revenue to grow by 6.3% annually and a $0.2 billion increase in earnings from the current level of $1.8 billion.

Uncover how lululemon athletica's forecasts yield a $270.82 fair value, a 61% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community members have produced 47 individual fair value estimates for lululemon, ranging from US$150 to over US$409 per share. Uncertainty around U.S. demand and tariff impacts is driving these varied outlooks, investors are encouraged to explore multiple viewpoints when assessing the company’s performance.

Explore 47 other fair value estimates on lululemon athletica - why the stock might be worth 11% less than the current price!

Build Your Own lululemon athletica Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your lululemon athletica research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free lululemon athletica research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate lululemon athletica's overall financial health at a glance.

Ready For A Different Approach?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- These 11 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.