Why MannKind (MNKD) Is Up 8.4% After New Afrezza Pediatric Approval And ADA Data Release

MannKind Corporation MNKD | 0.00 |

- MannKind recently reported new clinical and real‑world data for its inhaled insulin Afrezza and FUROSCIX at the American Diabetes Association’s 2026 Scientific Sessions, following the U.S. FDA’s May 2026 approval of Afrezza for children and adolescents aged 6 and older with type 1 and type 2 diabetes.

- The breadth of data, spanning pediatric outcomes, gestational diabetes, use with automated insulin delivery systems, lung safety, and heart‑failure‑related fluid overload, adds fresh clinical context to how MannKind’s Technosphere platform could be used across multiple high‑need patient groups.

- We’ll now examine how Afrezza’s new pediatric approval and supportive ADA data may influence MannKind’s investment narrative and future expectations.

Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

MannKind Investment Narrative Recap

To own MannKind, you need to believe its Technosphere inhaled platform can move from niche to broader use, with Afrezza’s pediatric label and new ADA data strengthening that case. In the near term, the key catalyst is how quickly Afrezza prescriptions respond to the expanded age group, while the biggest risk remains heavy dependence on Afrezza and Tyvaso DPI royalties in a competitive diabetes and lung disease market. The ADA data does not remove that concentration risk, but it does provide incremental clinical support.

Among recent updates, the nintedanib DPI (MNKD-201) milestones stand out, because they speak directly to MannKind’s effort to diversify beyond Afrezza. Completion of randomization in the INFLO-1 Phase 1b trial and first patient dosing in the global Phase 2 INFLO-2 IPF study show the Technosphere platform is being pushed into another serious lung indication, which could eventually balance today’s reliance on Afrezza and Tyvaso DPI related revenue.

Yet, for all the promise in pediatrics and IPF, investors still need to be aware of how concentrated MannKind remains in just a few revenue drivers and...

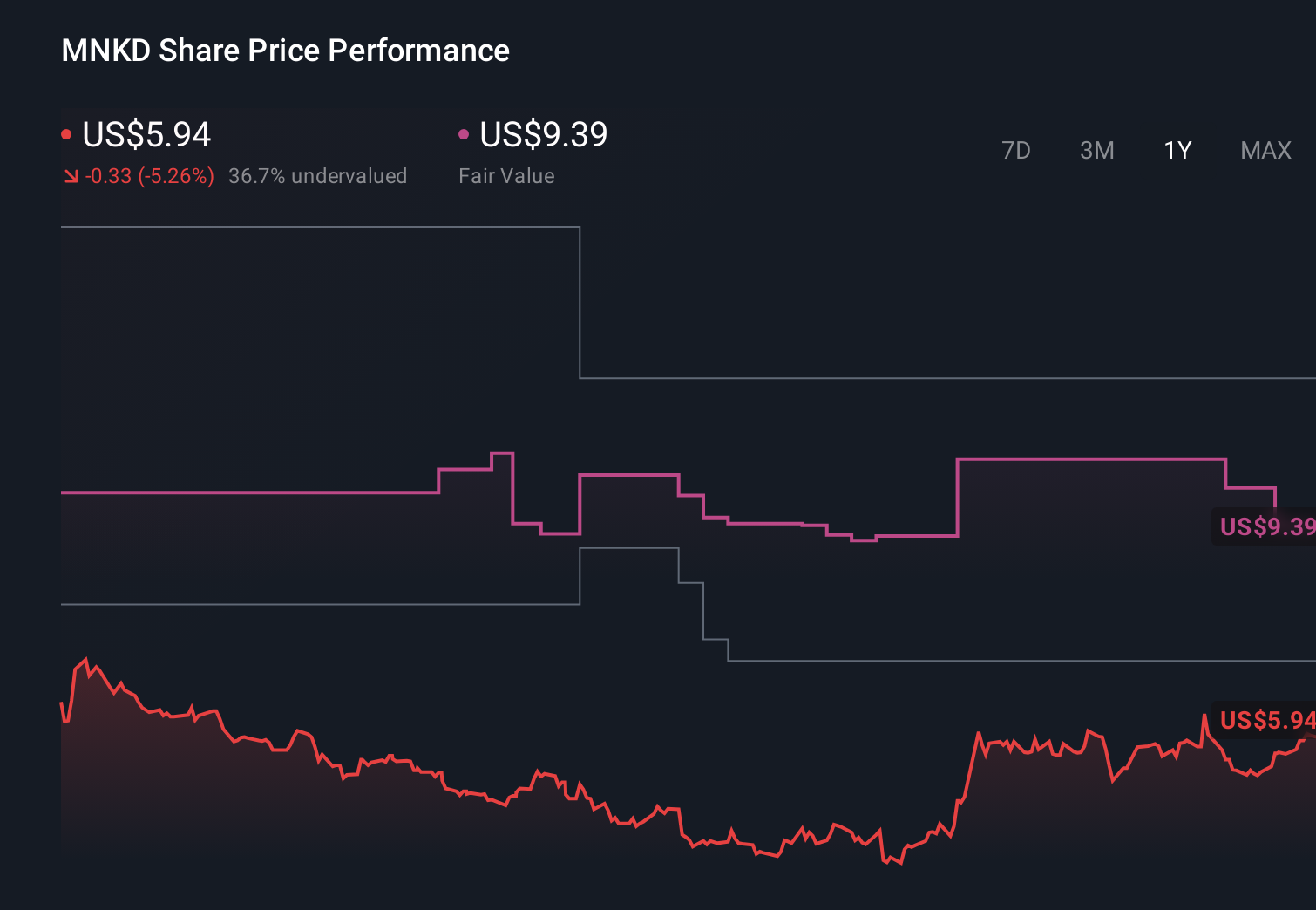

MannKind's narrative projects $544.8 million revenue and $62.0 million earnings by 2029. This requires 16.0% yearly revenue growth and about a $56.1 million earnings increase from $5.9 million today.

Uncover how MannKind's forecasts yield a $7.17 fair value, a 85% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts looked at MannKind much more cautiously, expecting only about US$447,000,000 in revenue and roughly US$4,700,000 in earnings by 2029, and highlighting how ongoing cash burn and dependence on a narrow product set could matter even if Afrezza’s pediatric data and IPF trials eventually gain traction, which is exactly why you may want to compare several viewpoints before deciding what you believe about this stock.

Explore 3 other fair value estimates on MannKind - why the stock might be worth over 2x more than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your MannKind research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free MannKind research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate MannKind's overall financial health at a glance.

Interested In Other Possibilities?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 32 companies in the world exploring or producing it. Find the list for free.

- Uncover the next big thing with 23 elite penny stocks that balance risk and reward.

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.