Why Millicom (TIGO) Is Down 6.6% After Reporting a Surge in 2025 Net Income

Millicom International Cellular SA TIGO | 0.00 |

- In February 2026, Millicom International Cellular S.A. reported fourth-quarter 2025 sales of US$1,652 million and net income of US$252 million, with basic earnings per share from continuing operations rising to US$1.51.

- For full-year 2025, Millicom’s net income increased to US$1.32 billions on essentially unchanged sales of US$5.82 billions, highlighting a sharp improvement in profitability relative to revenue growth.

- We will now examine how this surge in full-year profitability might reshape Millicom’s existing investment narrative and risk-reward profile.

Uncover the next big thing with 28 elite penny stocks that balance risk and reward.

Millicom International Cellular Investment Narrative Recap

To own Millicom, you need to believe in its ability to convert Latin American data and broadband demand into durable cash generation, despite currency volatility and heavy network investment needs. The sharp jump in 2025 net income to US$1.32 billion strengthens the profitability side of that story, but the presence of large one off gains and ongoing high capex means the near term risk around free cash flow remains very much in focus rather than materially reduced.

Against that backdrop, the company’s decision to resume and expand cash returns, including the US$3.00 per share recurring dividend and an additional US$1.25 special dividend approved in 2025, ties directly into the current debate about sustainability of shareholder payouts. These distributions look more credible in light of the stronger earnings base, yet they also heighten sensitivity to any setback in cash generation or leverage metrics over the next few years.

Yet even with this improved profitability, investors should be aware that Millicom’s high ongoing capex and currency exposure could still...

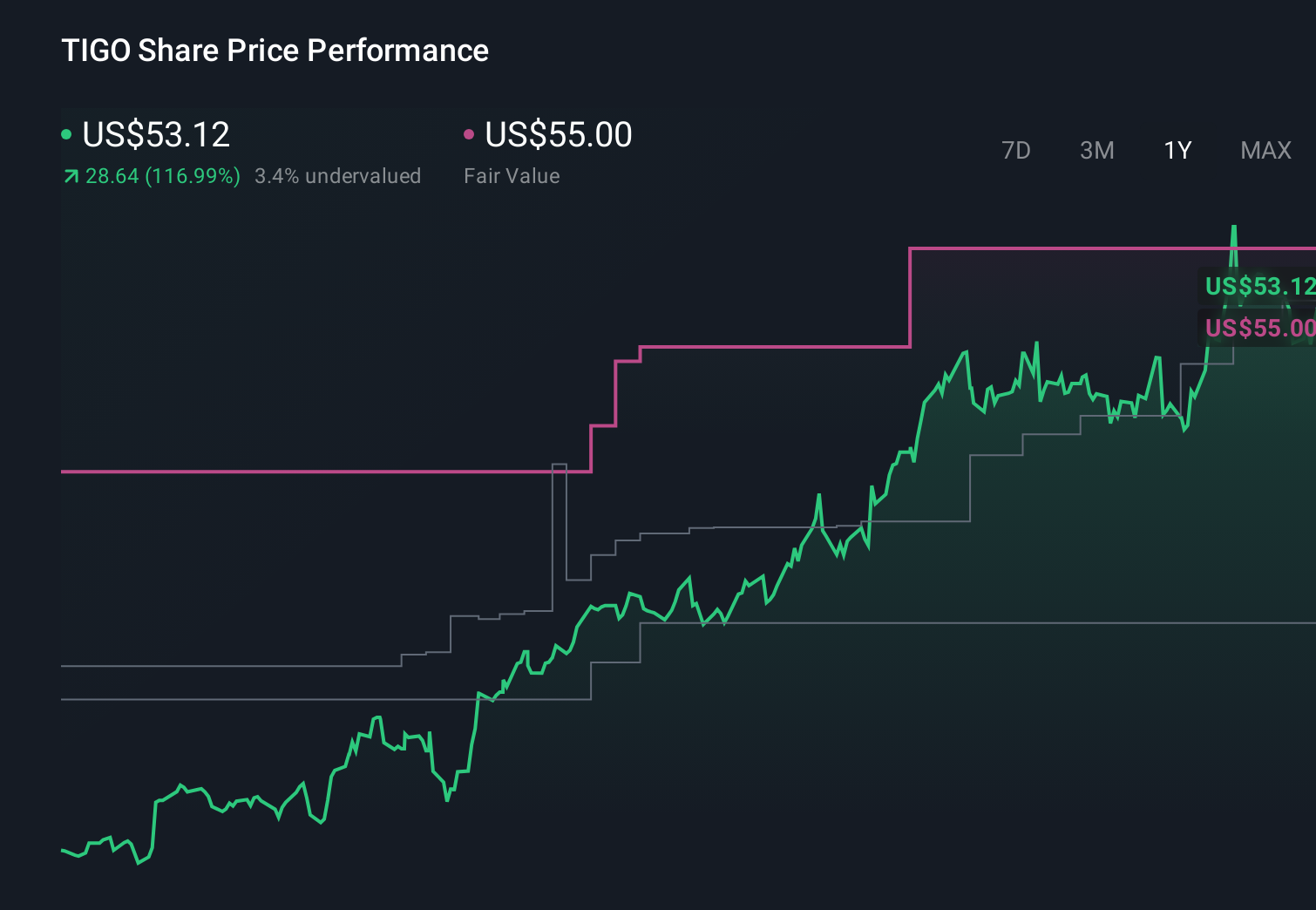

Millicom International Cellular's narrative projects $5.9 billion revenue and $628.3 million earnings by 2028. This requires 1.7% yearly revenue growth and a $326.7 million earnings decrease from $955.0 million today.

Uncover how Millicom International Cellular's forecasts yield a $52.35 fair value, a 25% downside to its current price.

Exploring Other Perspectives

The most bullish analysts were assuming around US$6.2 billion of revenue and US$662 million of earnings by 2028, so this profit beat could either reinforce their optimism or force a rethink, especially if the FX and heavy capex risks they flagged continue to clash with today’s much stronger reported margins.

Explore 7 other fair value estimates on Millicom International Cellular - why the stock might be worth over 2x more than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Millicom International Cellular research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Millicom International Cellular research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Millicom International Cellular's overall financial health at a glance.

Curious About Other Options?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- This technology could replace computers: discover 22 stocks that are working to make quantum computing a reality.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 28 best rare earth metal stocks of the very few that mine this essential strategic resource.

- Capitalize on the AI infrastructure supercycle with our selection of the 35 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.