Why NovoCure (NVCR) Is Up 33.2% After FDA Clears Optune Pax And Guidance Ticks Higher

NovoCure Ltd. NVCR | 0.00 |

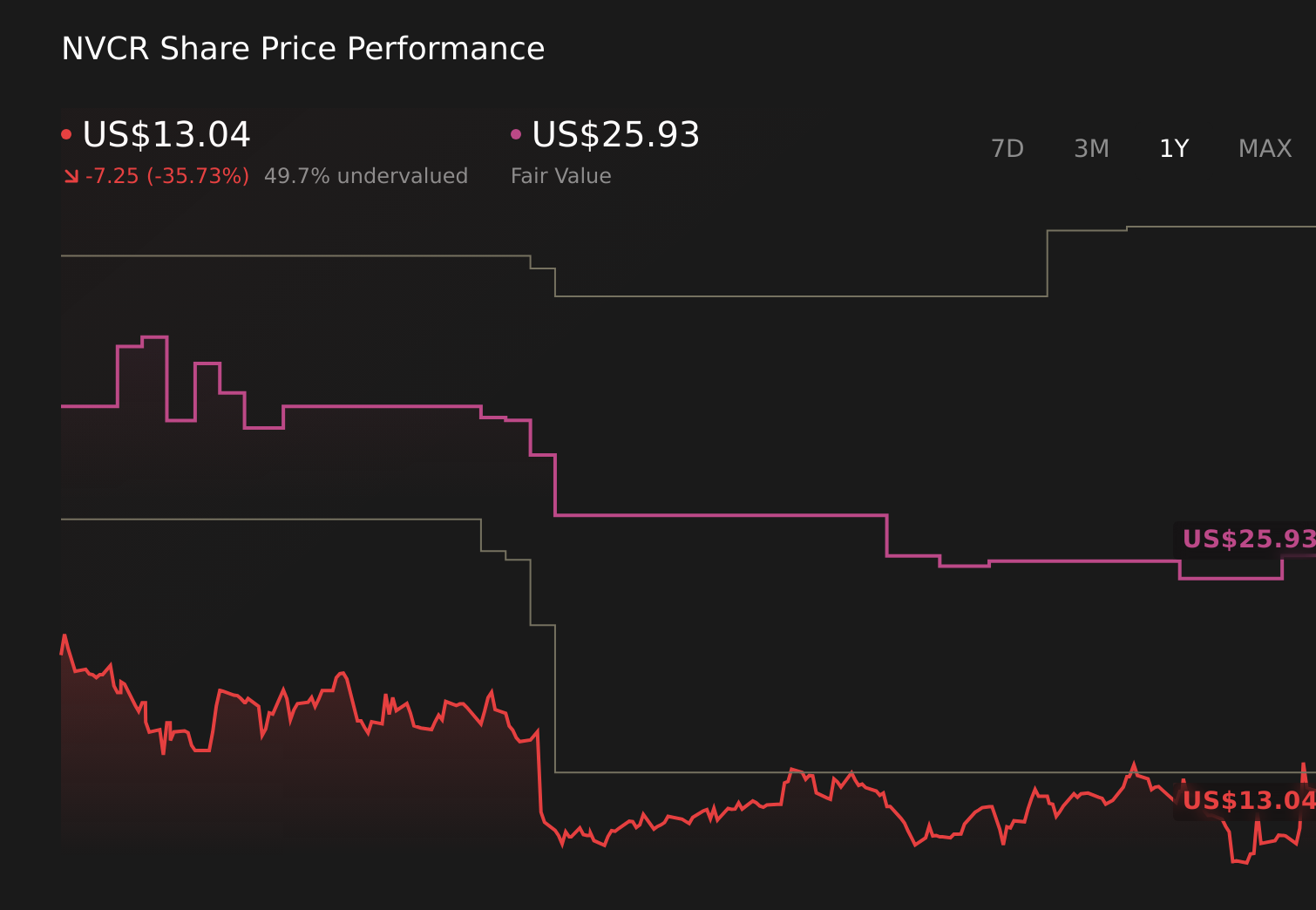

- In the first quarter of 2026, NovoCure reported net revenues of US$174.06 million, up from US$154.99 million a year earlier, while its net loss widened to US$71.14 million and it modestly raised full‑year 2026 revenue guidance to US$690 million–US$710 million.

- The quarter also marked U.S. FDA approval and an active launch of Optune Pax for locally advanced pancreatic cancer, with rapid physician certification, early payer coverage, and growing prescription activity highlighting the company’s expanding tumor treating fields footprint despite higher operating losses.

- We’ll now examine how the Optune Pax approval and raised 2026 revenue guidance affect NovoCure’s existing investment narrative and risk profile.

This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

NovoCure Investment Narrative Recap

To own NovoCure, you have to believe tumor treating fields can grow into a meaningful, multi indication oncology platform while eventually supporting a sustainable business despite continued losses. The Optune Pax launch and higher 2026 revenue guidance reinforce the near term focus on expanding pancreatic use, while the most important upcoming catalyst remains the TRIDENT Phase 3 GBM data. The widened net loss keeps the central risk intact: a long, uncertain path to profitability and consistent cash generation.

The most relevant recent development is NovoCure’s modestly raised 2026 revenue outlook to US$690 million–US$710 million following Optune Pax approval and early uptake. That higher range ties directly to management’s confidence in new indications contributing more meaningfully to the top line, just as investors are watching whether pancreatic cancer and lung cancer can offset higher operating costs and validate the broader TTFields growth story.

Yet behind the strong launch headlines, investors should also be aware of...

NovoCure’s narrative projects $915.6 million revenue and $119.8 million earnings by 2029. This requires 11.8% yearly revenue growth and a $256 million earnings increase from -$136.2 million today.

Uncover how NovoCure's forecasts yield a $26.07 fair value, a 57% upside to its current price.

Exploring Other Perspectives

Before this update, the most optimistic analysts were already modeling about US$930.1 million of revenue and US$114.6 million of earnings by 2028, a far more upbeat view that assumes reimbursement and adoption hurdles ease much faster than the slower build implied by current losses and cautious guidance ranges.

Explore 4 other fair value estimates on NovoCure - why the stock might be worth over 9x more than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your NovoCure research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free NovoCure research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate NovoCure's overall financial health at a glance.

No Opportunity In NovoCure?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- The future of work is here. Discover the 34 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.