Why Photronics (PLAB) Is Down 10.8% After Margin-Squeezing Q3 Guide And New Legal Scrutiny - And What's Next

Photronics PLAB | 0.00 |

- Photronics recently reported second-quarter 2026 results showing broadly flat sales at US$209.94 million year-on-year but significantly higher net income of US$31.43 million, while also issuing third-quarter guidance that points to operating margin pressures and participating in the Bank of America 2026 Global Technology Conference.

- The earnings release has also prompted a securities-law investigation and sharp criticism from market commentators, highlighting growing scrutiny of how Photronics communicates its outlook and manages industry headwinds.

- We’ll now explore how the combination of weaker guidance and a securities-law investigation could reshape Photronics’ previously optimistic investment narrative.

The future of work is here. Discover the 34 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Photronics Investment Narrative Recap

To hold Photronics today, you need to believe that its photomask technology will keep it relevant in semiconductor and display manufacturing, despite near term volatility. The sharp share price drop, weaker guidance, and new securities law investigation all focus attention on the biggest current risk: that cyclical slowdowns and scrutiny of its disclosures could compound existing pressure from geopolitical and industry uncertainty.

The Q3 2026 guidance for revenue of US$207 million to US$215 million and operating margins of 18% to 20% is the key announcement here, because it directly affects how investors weigh recent operational headwinds against ongoing heavy investment in advanced tools and capacity. This guidance frames whether current capital spending ultimately supports earnings resilience or heightens the risk of compressed free cash flow if industry demand softens further.

Yet behind the headline moves in the share price, the real issue investors need to be aware of is how limited order visibility, combined with...

Photronics' narrative projects $930.0 million revenue and $81.2 million earnings by 2029. This implies 2.6% yearly revenue growth but a decline of $77.9 million in earnings from $159.1 million today.

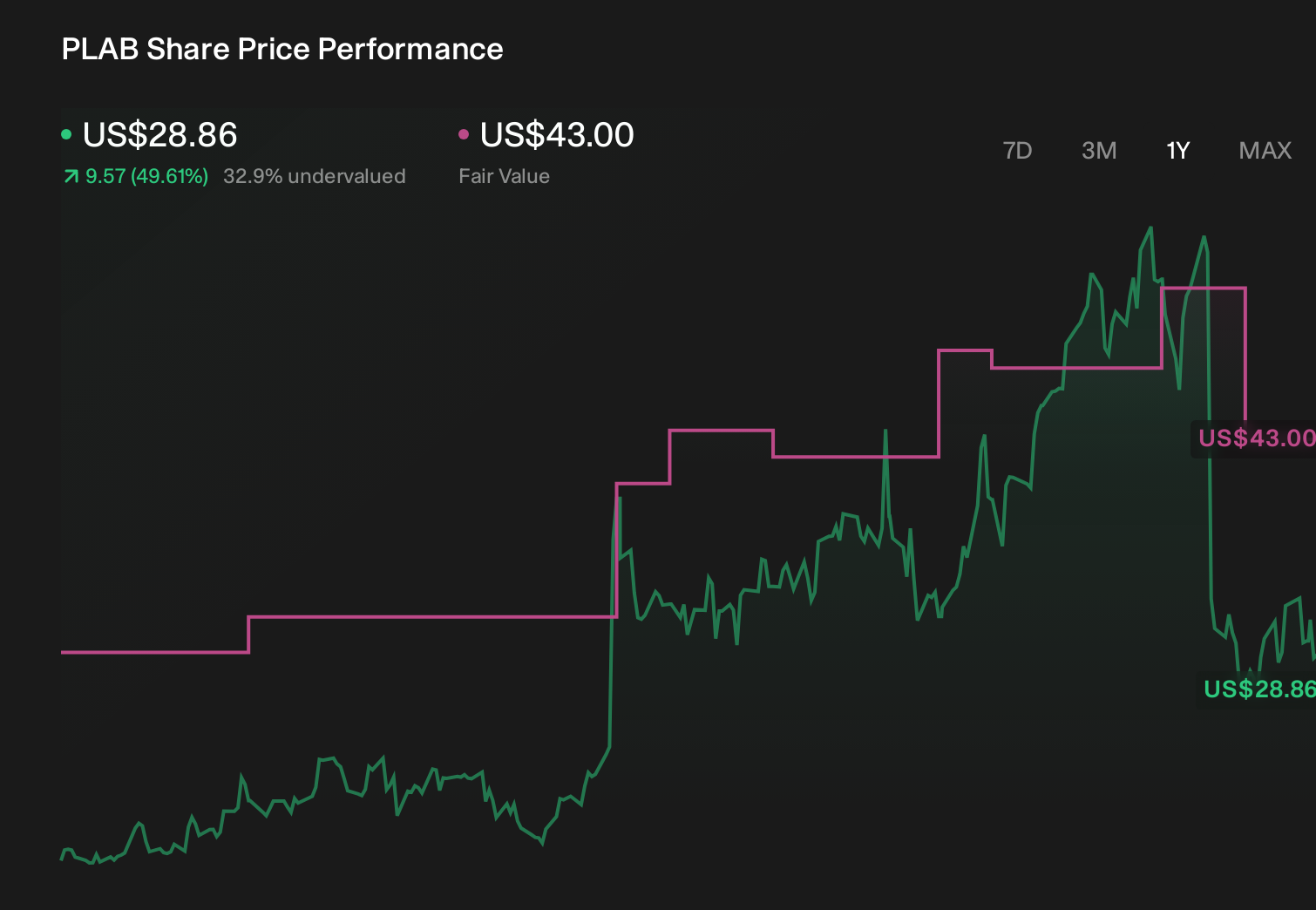

Uncover how Photronics' forecasts yield a $43.00 fair value, a 50% upside to its current price.

Exploring Other Perspectives

Five members of the Simply Wall St Community currently place Photronics’ fair value between US$21.80 and US$43.00, showing how differently people read the same numbers. Set that against the recent margin guidance and investigation risk, and it becomes clear why you may want to compare several independent views before deciding how much of Photronics’ earnings volatility you are comfortable with.

Explore 5 other fair value estimates on Photronics - why the stock might be worth as much as 50% more than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Photronics research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Photronics research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Photronics' overall financial health at a glance.

Looking For Alternative Opportunities?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Find 48 companies with promising cash flow potential yet trading below their fair value.

- We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Uncover the next big thing with 25 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.