Why Royal Caribbean Cruises (RCL) Is Up 14.0% After Record Bookings, New Ships And Buybacks

Royal Caribbean Group RCL | 273.59 | -3.00% |

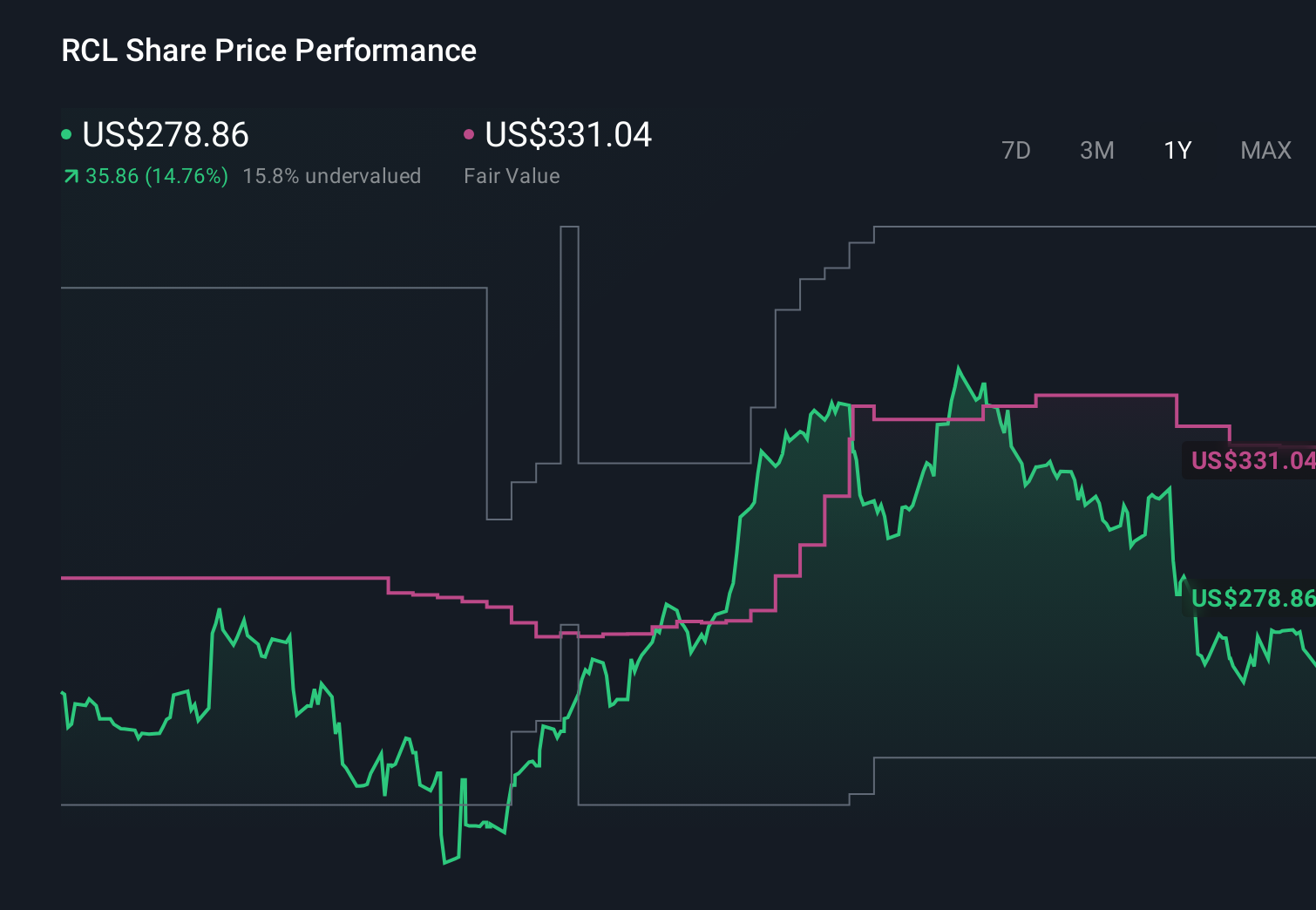

- Royal Caribbean Group reported past fourth-quarter 2025 revenue of US$4.26 billion and net income of US$754 million, alongside full-year revenue of US$17.94 billion and net income of US$4.27 billion, as it issued upbeat 2026 guidance and completed a US$200 million share buyback.

- The company also unveiled long-term growth plans, including ordering two new Discovery Class ocean ships with options for four more and expanding its Celebrity River Cruises fleet, underpinned by what management described as the strongest booking weeks in its history.

- With the shares rising over the past week, we’ll examine how record bookings and Discovery Class expansion shape Royal Caribbean’s investment narrative.

The latest GPUs need a type of rare earth metal called Terbium and there are only 30 companies in the world exploring or producing it. Find the list for free.

What Is Royal Caribbean Cruises' Investment Narrative?

To own Royal Caribbean today, you need to believe that demand for cruise and broader vacation experiences can stay resilient enough to support ongoing debt service, steady earnings growth and heavy investment in new ships and destinations. The latest quarter delivered higher revenue and net income, record booking weeks and guidance for double-digit 2026 revenue growth, which together reinforce near-term catalysts around pricing, occupancy and margin efficiency. The Discovery Class orders and plans to expand Celebrity River Cruises deepen the long-term growth story, but also add to capital intensity and execution risk at a time when the balance sheet is still highly leveraged. The recent US$200 million buyback and dividend signal confidence, yet the sharp share price jump suggests a lot of this good news may now be reflected in the stock.

But against those record bookings sits a financial risk investors should keep front of mind. Royal Caribbean Cruises' shares have been on the rise but are still potentially undervalued. Find out how large the opportunity might be.Exploring Other Perspectives

Simply Wall St Community members’ fair value estimates span roughly US$220 to US$440 across 10 views, giving you a broad set of starting points. When you set that against Royal Caribbean’s debt load and the investment needed for Discovery Class and new destinations, it underlines why different investors can reach very different conclusions about the company’s future performance.

Explore 10 other fair value estimates on Royal Caribbean Cruises - why the stock might be worth 33% less than the current price!

Build Your Own Royal Caribbean Cruises Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Royal Caribbean Cruises research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Royal Caribbean Cruises research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Royal Caribbean Cruises' overall financial health at a glance.

Ready For A Different Approach?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- These 14 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Find companies with promising cash flow potential yet trading below their fair value.

- AI is about to change healthcare. These 112 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.