Why Royal Caribbean (RCL) Is Down 5.4% After Raising EPS Outlook And Expanding Its AI Strategy

Royal Caribbean Group RCL | 0.00 |

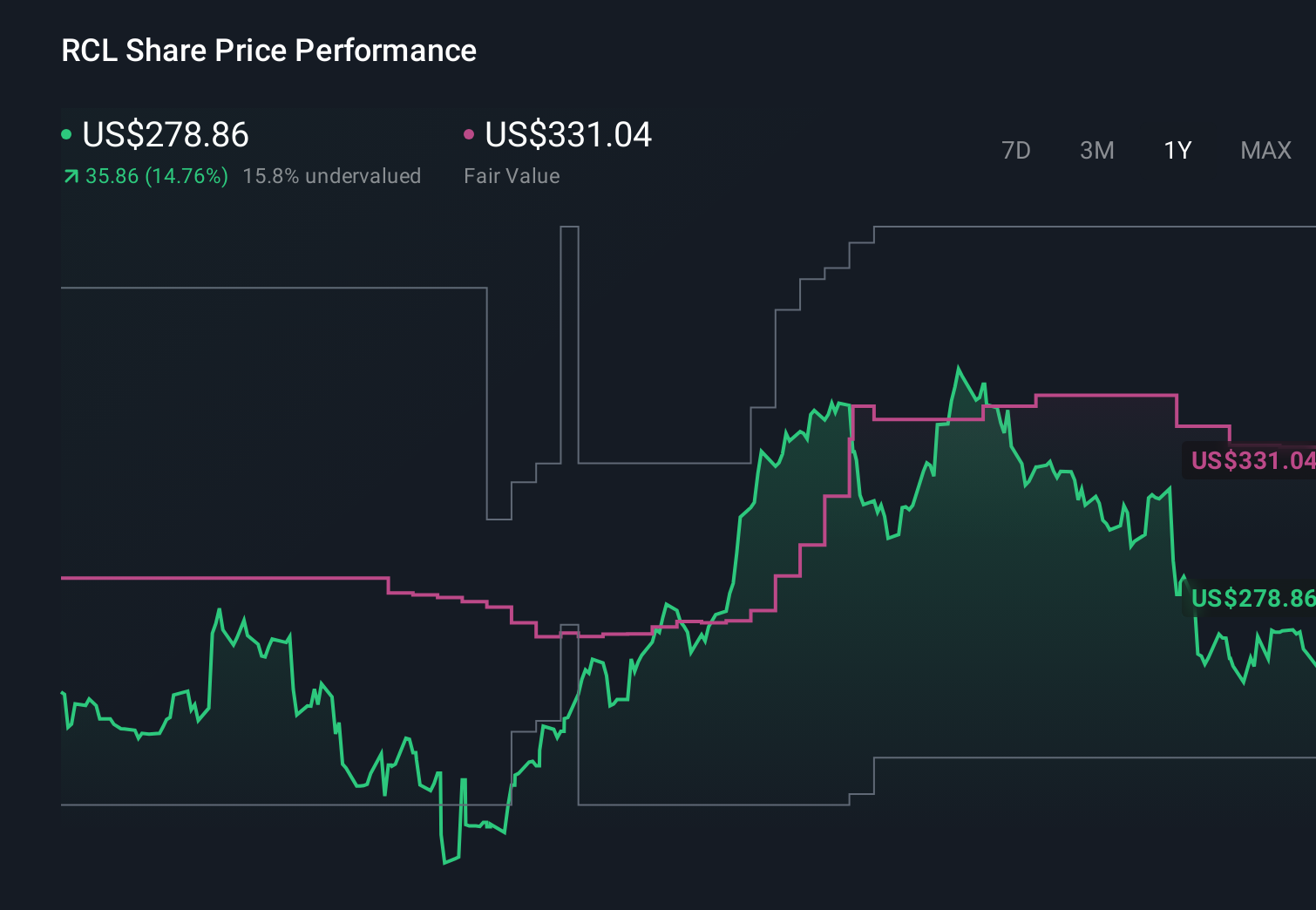

- Royal Caribbean Cruises Ltd. recently reported stronger-than-expected Q1 2026 results, raised its full-year adjusted EPS outlook, and affirmed a quarterly US$1.50 per-share dividend payable on July 2, 2026.

- The company is also embedding artificial intelligence across pricing, booking, and onboard personalization, aiming to build a unified “intelligence layer” that could meaningfully reshape how guests plan and experience its cruises.

- Next, we’ll examine how the upgraded full-year outlook may influence Royal Caribbean’s investment narrative built around margins and cash returns.

Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

Royal Caribbean Cruises Investment Narrative Recap

To own Royal Caribbean today, you need to believe that demand for cruises can remain resilient enough to support healthy margins and ongoing cash returns, even if the economic backdrop softens. The stronger-than-expected Q1 2026 results and higher full-year EPS outlook reinforce the near-term margin and cash generation story, while the main risk still centers on a pullback in consumer discretionary spending and close-in bookings that could pressure pricing, yields, and profitability.

Among the recent developments, the reaffirmed US$1.50 quarterly dividend stands out, given it follows a series of increases from US$0.55 in early 2025. Alongside the upgraded 2026 earnings outlook, this signals a continued focus on returning cash to shareholders, even as the company invests in AI and new ships. For investors, how well these cash returns hold up if macro conditions worsen or costs rise remains a key catalyst to watch.

Yet behind the upbeat earnings and rising dividend, investors should be aware of the growing tension between higher capital spending, leverage, and the risk that...

Royal Caribbean Cruises' narrative projects $23.0 billion revenue and $6.1 billion earnings by 2029. This requires 8.6% yearly revenue growth and about a $1.8 billion earnings increase from $4.3 billion today.

Uncover how Royal Caribbean Cruises' forecasts yield a $348.46 fair value, a 34% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already assuming revenue could reach about US$24.2 billion and earnings US$6.9 billion by 2029, which is a much rosier picture than the consensus view that focuses more on macro and cost risks; with Q1 2026 now in hand, you can judge for yourself whether this new information supports that stronger thesis or suggests those expectations might need to be tempered.

Explore 6 other fair value estimates on Royal Caribbean Cruises - why the stock might be worth just $268.88!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Royal Caribbean Cruises research is our analysis highlighting 5 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Royal Caribbean Cruises research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Royal Caribbean Cruises' overall financial health at a glance.

Interested In Other Possibilities?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Uncover the next big thing with 25 elite penny stocks that balance risk and reward.

- AI is about to change healthcare. These 32 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The latest GPUs need a type of rare earth metal called Terbium and there are only 31 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.