Why Snowflake (SNOW) Is Up 48.4% After Deepening Its AI Partnership With AWS

Snowflake SNOW | 0.00 |

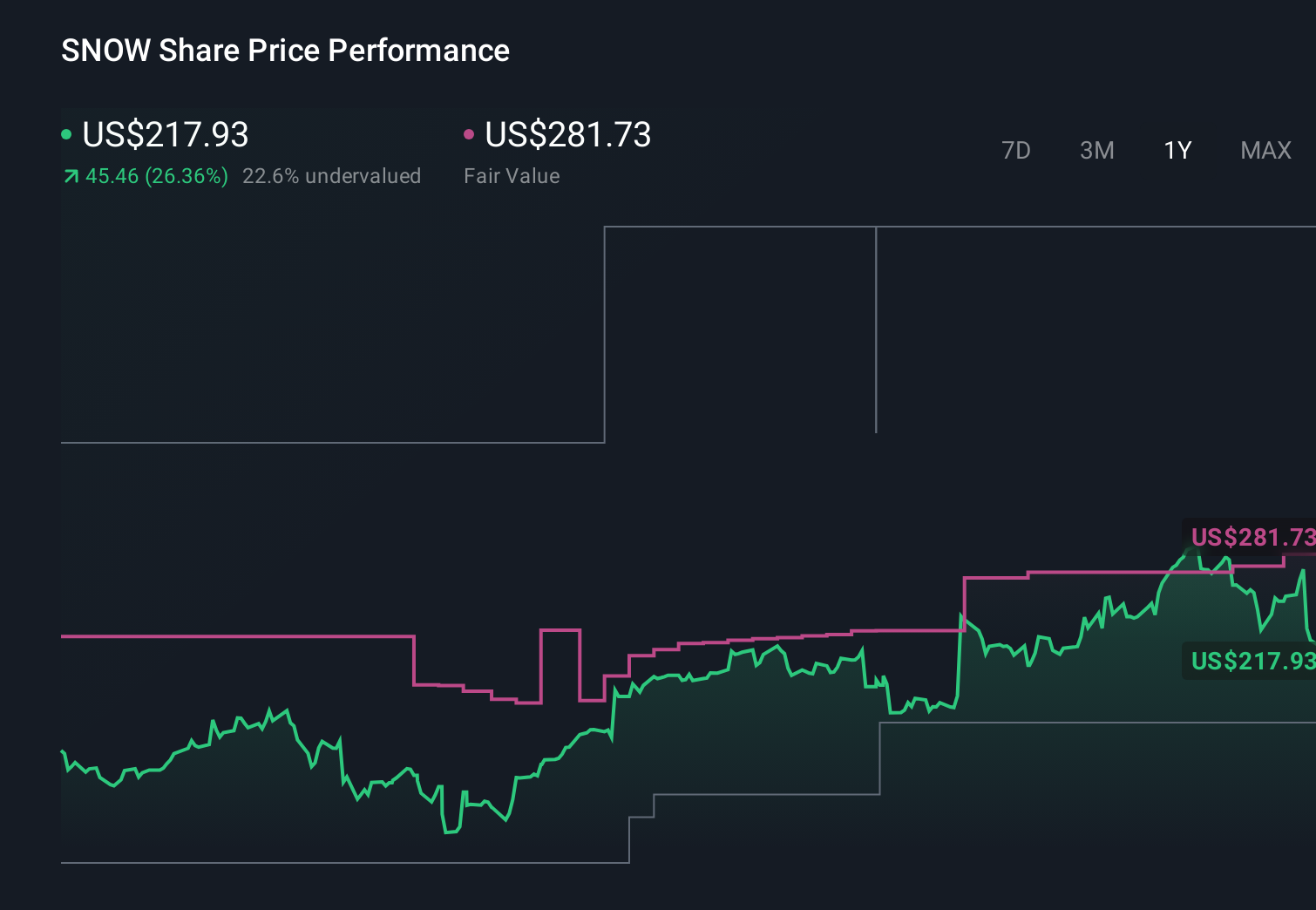

- Snowflake recently announced a multi-year collaboration agreement with Amazon Web Services (AWS), including a US$6.00 billion infrastructure commitment, deeper AI product integrations, and expanded joint go‑to‑market efforts, alongside first‑quarter fiscal 2027 results showing higher sales and a smaller net loss than a year earlier.

- The company also raised its fiscal 2027 and second‑quarter product revenue guidance, underscoring how AI‑focused partnerships and new customer workloads are becoming central to Snowflake’s growth plans.

- We’ll now examine how the expanded AWS AI partnership could reshape Snowflake’s investment narrative and long‑term earnings power assumptions.

AI is about to change healthcare. These 37 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Snowflake Investment Narrative Recap

To own Snowflake, you need to believe its AI Data Cloud can stay central to how enterprises store and analyze data, even as competition intensifies and profitability remains elusive. The new US$6.00 billion AWS agreement and raised fiscal 2027 guidance bolster the near term growth catalyst around AI workloads, but also magnify the key risk that heavy cloud spend and ongoing losses could weigh on the stock if demand or pricing weakens.

The AWS collaboration is the most relevant update here, given its focus on embedding generative and agentic AI directly on governed enterprise data. By tying Snowflake Cortex AI more tightly to AWS infrastructure and expanding into 10 new regions, the deal directly supports the AI led usage story that underpins current growth expectations, while also increasing exposure to hyperscaler competition and customer cost scrutiny.

Yet beneath the excitement, investors should be aware that Snowflake’s large AWS commitment could become a liability if...

Snowflake's narrative projects $9.0 billion revenue and $689.7 million earnings by 2029. This requires 24.5% yearly revenue growth and about a $2.0 billion earnings increase from -$1.3 billion today.

Uncover how Snowflake's forecasts yield a $232.74 fair value, a 9% downside to its current price.

Exploring Other Perspectives

Some of the lowest rated analysts were already assuming around 23 percent annual revenue growth and no profitability by 2029, which reflects a much more cautious view than the consensus and raises fair questions about whether AI partnerships alone can offset concerns about hyperscaler competition and rising compliance costs.

Explore 12 other fair value estimates on Snowflake - why the stock might be worth less than half the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Snowflake research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

- Our free Snowflake research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Snowflake's overall financial health at a glance.

Looking For Alternative Opportunities?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Capitalize on the AI infrastructure supercycle with our selection of the 47 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- The future of work is here. Discover the 35 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 31 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.