Why Southwest Airlines (LUV) Is Up 7.8% After JPMorgan’s Double Upgrade And What’s Next

Southwest Airlines Co. LUV | 37.60 | -1.65% |

- Over the past week, Southwest Airlines has drawn fresh attention as JPMorgan double-upgraded the stock to Overweight and placed it on its Positive Catalyst Watch ahead of the carrier’s late-January earnings release and 2026 guidance update.

- This shift comes as analysts reassess Southwest’s longer-term prospects in light of its planned move to assigned seating, new fare categories, and cabin changes beginning in early 2026.

- Next, we’ll explore how JPMorgan’s double-upgrade and expectations around 2026 guidance could reshape Southwest Airlines’ existing investment narrative.

We've found 11 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

Southwest Airlines Investment Narrative Recap

To own Southwest today, you need to believe its cabin overhaul, assigned seating, and new fare structure can translate its brand strength into higher quality earnings, while near term results remain under scrutiny. JPMorgan’s double-upgrade raises the stakes for the Jan. 29 earnings and 2026 guidance, which now look like the key catalyst, but margin pressure and mixed analyst views keep execution risk front and center rather than materially changing it.

The most relevant recent development here is JPMorgan’s move from Underweight to Overweight with a Street high US$60 target, explicitly tied to Southwest’s upcoming 2026 guidance and potential EPS trajectory. This sits against a broader backdrop of neutral or cautious ratings and only modest price target increases from Citi, UBS, Wells Fargo and B of A, underscoring how pivotal the forthcoming guidance could be in either validating or challenging these more optimistic expectations.

Yet, against this cautiously improving sentiment, investors should be aware of risks around volatile fuel costs and Southwest’s decision to cease fuel hedging, which could...

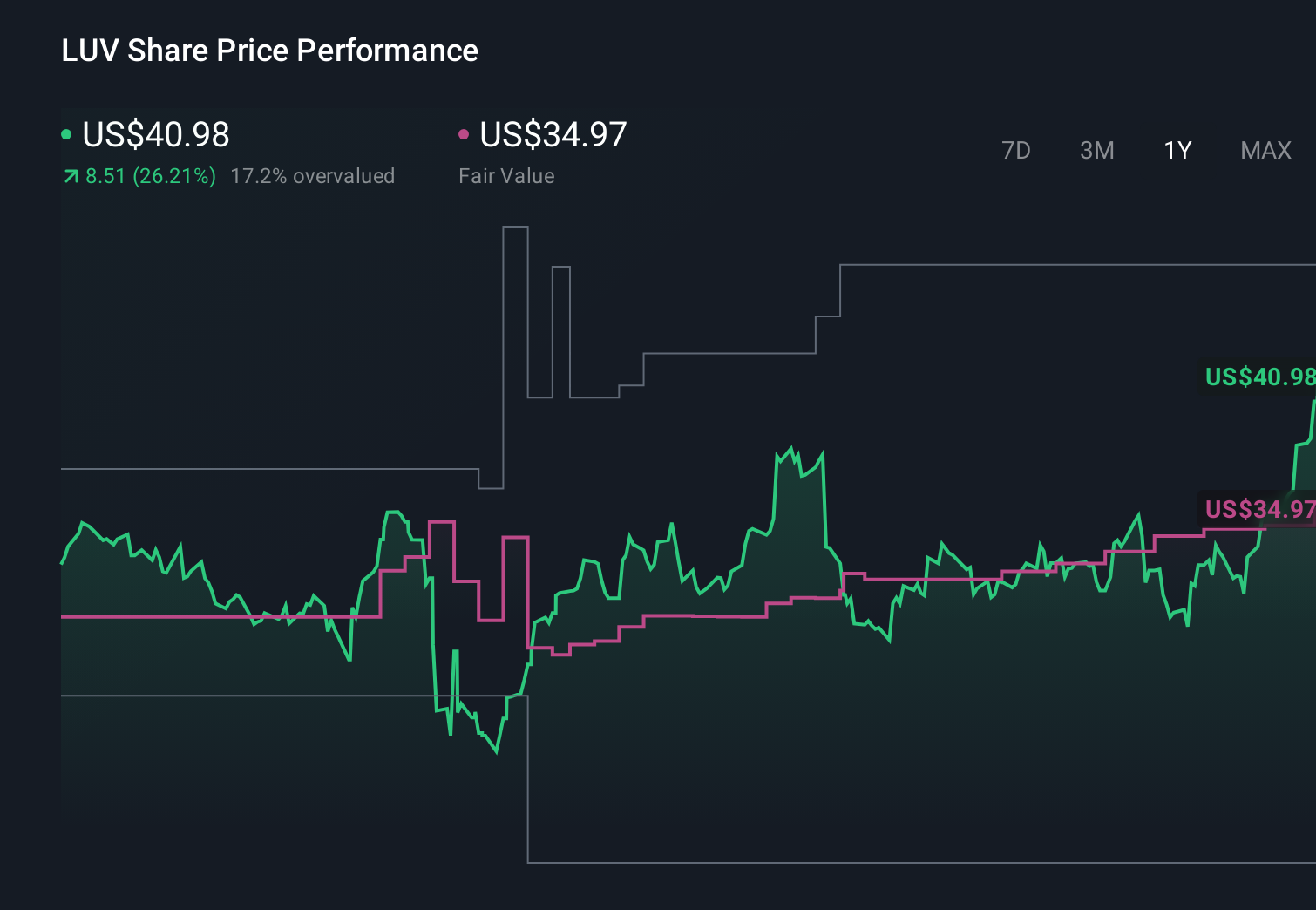

Southwest Airlines’ narrative projects $32.6 billion revenue and $1.9 billion earnings by 2028.

Uncover how Southwest Airlines' forecasts yield a $39.63 fair value, a 11% downside to its current price.

Exploring Other Perspectives

Seven fair value estimates from the Simply Wall St Community span roughly US$26.72 to US$151.24, showing how far apart individual views can be. Before leaning on any single number, it is worth weighing that dispersion against the central near term catalyst in Southwest’s story, the upcoming 2026 guidance that many see as critical for clarifying how its new fare structure and cabin changes may influence future performance.

Explore 7 other fair value estimates on Southwest Airlines - why the stock might be worth over 3x more than the current price!

Build Your Own Southwest Airlines Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Southwest Airlines research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Southwest Airlines research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Southwest Airlines' overall financial health at a glance.

Contemplating Other Strategies?

Our top stock finds are flying under the radar-for now. Get in early:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 28 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.