Why Sunrun (RUN) Is Up 8.4% After Q1 Earnings Beat And Record Storage Attachment Rate

Sunrun Inc. RUN | 0.00 |

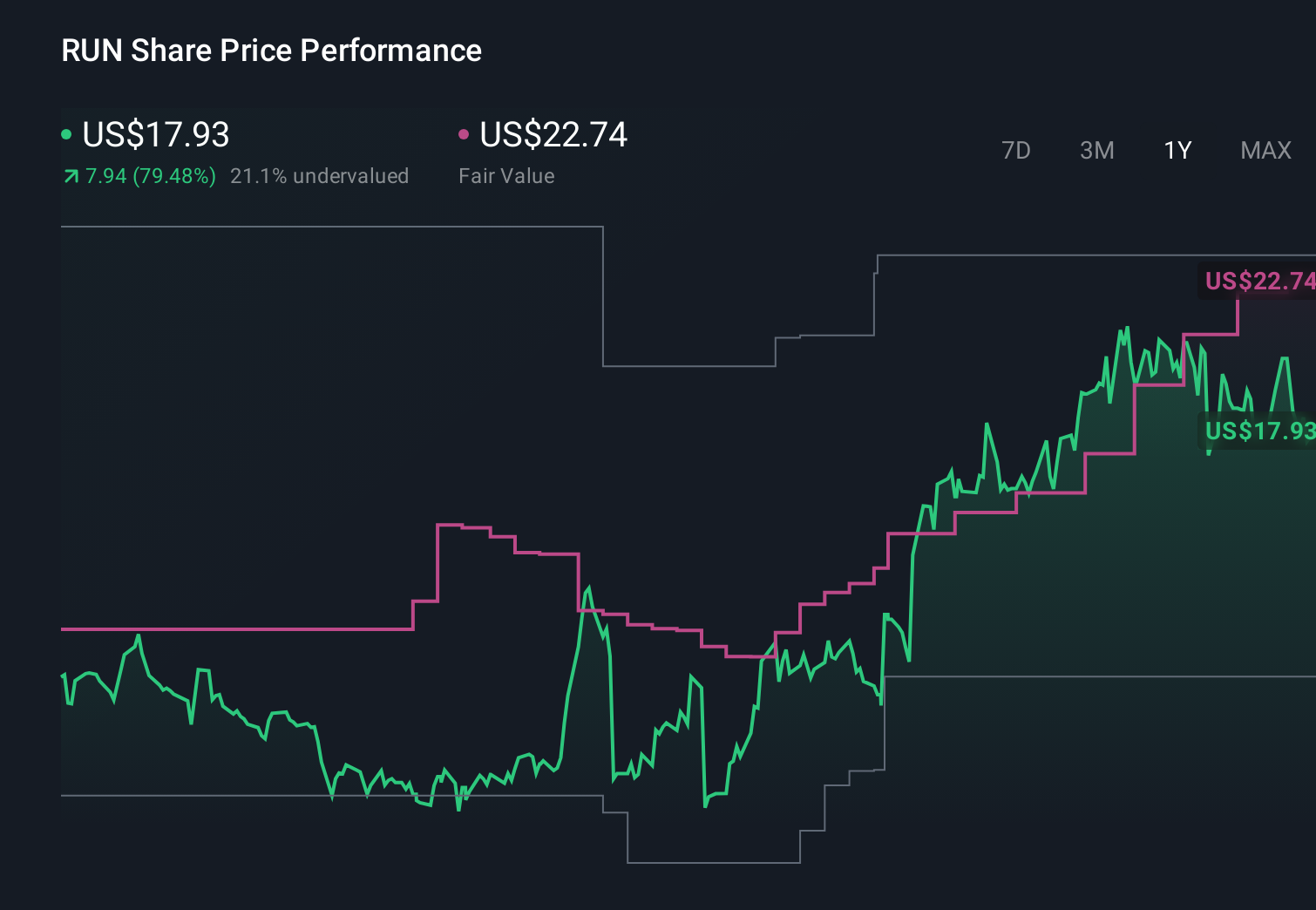

- In early May 2026, Sunrun Inc. reported first-quarter 2026 results showing total revenue of US$722.23 million and net income of US$167.64 million, with diluted earnings per share from continuing operations of US$0.62, all higher than the same period a year earlier.

- Alongside this earnings beat, Sunrun priced its sixteenth securitization since 2015 with improved credit spreads and a 73% storage attachment rate, underscoring how its storage-first model and access to financing are becoming increasingly central to its business mix.

- We will now examine how this earnings surprise and record storage attachment rate may influence Sunrun’s existing investment narrative.

Explore 27 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

Sunrun Investment Narrative Recap

To own Sunrun, you need to believe residential solar plus storage can support a durable, financing intensive business even as incentives change and capital remains available. The Q1 2026 earnings beat and 73% storage attachment rate reinforce storage led, recurring cash potential, but do not remove the key short term risk around funding costs and continued access to securitizations and tax equity on acceptable terms.

The April 2026 securitization, Sunrun’s sixteenth since 2015, matters here because tighter credit spreads and a roughly 79% advance rate indicate capital markets are still absorbing Sunrun’s assets. For investors focused on catalysts, this improved pricing and the company’s plan to raise additional non recourse financing support the idea that securitization capacity remains a crucial enabler of its storage first growth model.

But against the upbeat quarter, investors should still be aware of how rising funding costs or weaker securitization appetite could...

Sunrun's narrative projects $3.7 billion revenue and $56.5 million earnings by 2029. This requires 8.0% yearly revenue growth and a $391.1 million earnings decrease from $447.6 million today.

Uncover how Sunrun's forecasts yield a $19.67 fair value, a 43% upside to its current price.

Exploring Other Perspectives

Before this quarter, the most optimistic analysts were already penciling in around US$4.9 billion of revenue and US$1.1 billion of earnings by 2029, so if you buy into their view that storage adoption and grid service monetization could transform margins, Sunrun’s latest profit surprise and 73% storage attachment rate might strengthen that bullish case, even as the same news leaves plenty of room to question whether financing risks could still limit how much of that upside is realised.

Explore 3 other fair value estimates on Sunrun - why the stock might be worth over 2x more than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Sunrun research is our analysis highlighting 4 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Sunrun research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Sunrun's overall financial health at a glance.

Seeking Other Investments?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 33 companies in the world exploring or producing it. Find the list for free.

- Capitalize on the AI infrastructure supercycle with our selection of the 40 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Invest in the nuclear renaissance through our list of 91 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.