Why Teradyne (TER) Is Up 6.6% After Surging Q1 Earnings And Fresh Q2 Guidance

Teradyne, Inc. TER | 0.00 |

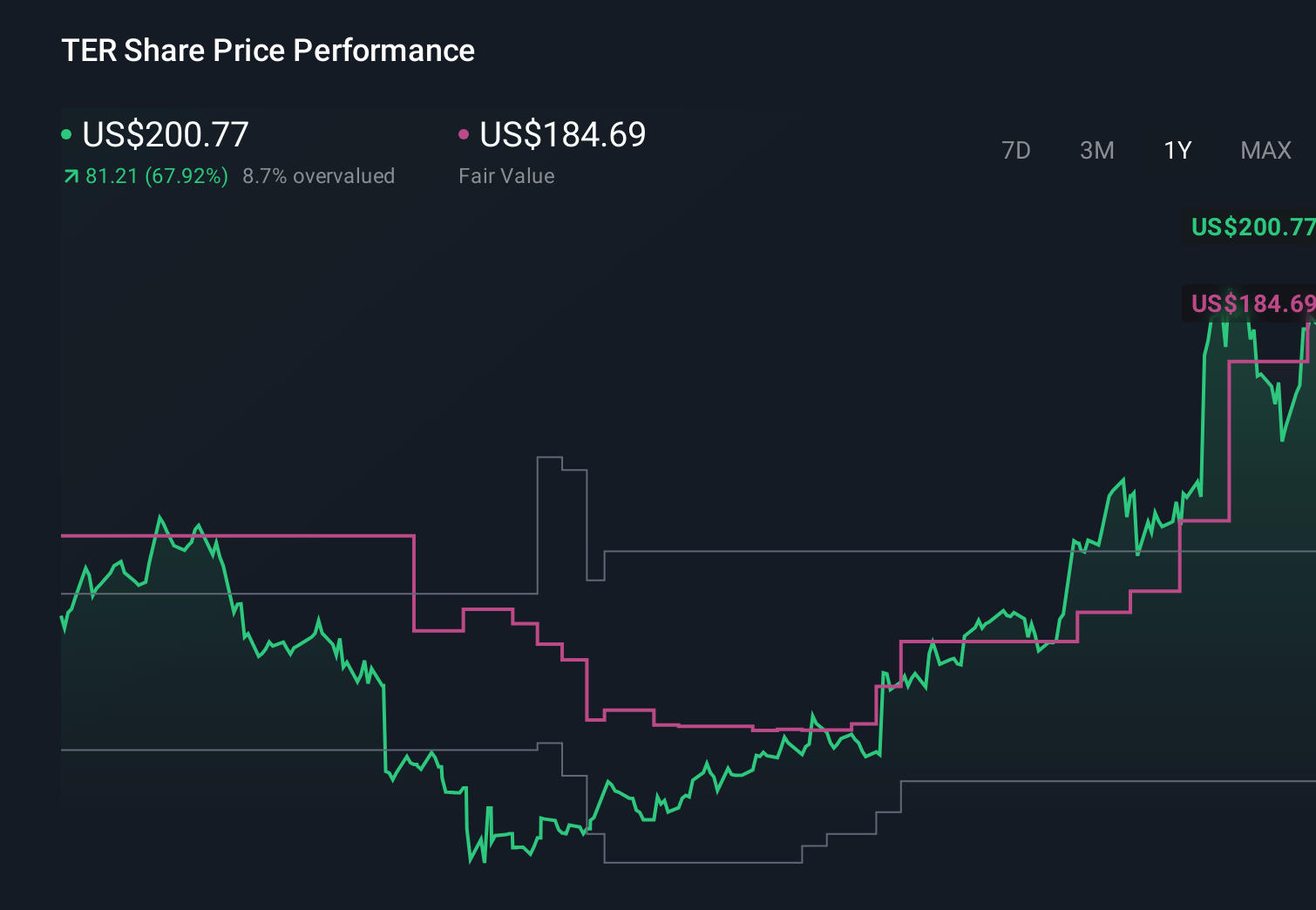

- Teradyne, Inc. reported first-quarter 2026 results showing sales of US$1,282.49 million and net income of US$398.91 million, with basic earnings per share from continuing operations of US$2.55, and announced a quarterly dividend of US$0.13 per share payable on June 12, 2026 to shareholders of record on May 21, 2026.

- Alongside this strong year-over-year improvement in profitability, Teradyne also issued second-quarter 2026 guidance calling for revenue of US$1,150 million to US$1,250 million and GAAP diluted earnings of US$1.83 to US$2.12 per share, giving investors a clearer view of near-term performance.

- We will now examine how Teradyne’s substantially higher first-quarter earnings and fresh second-quarter guidance influence its existing investment narrative.

Outshine the giants: these 14 early-stage AI stocks could fund your retirement.

Teradyne Investment Narrative Recap

To own Teradyne, you need to believe its test and automation products can benefit from long-term themes like AI, chip complexity, and factory automation, while managing cyclical swings and tariff uncertainty. The sharp first quarter earnings jump and solid second quarter guidance help near term confidence, but they do not remove key risks around trade policy, mix driven margin volatility, or the still pressured robotics segment.

The second quarter 2026 guidance for revenue of US$1,150 million to US$1,250 million and GAAP diluted EPS of US$1.83 to US$2.12 per share is the most relevant update here, because it extends the improved profitability picture into the near term and partially addresses earlier concerns about limited visibility beyond the next quarter, even as geopolitical and robotics related headwinds remain in focus.

Yet, against this strong recent profitability, investors should still be aware of how tariffs and trade policies could suddenly...

Teradyne's narrative projects $6.7 billion revenue and $2.0 billion earnings by 2029. This requires 20.9% yearly revenue growth and a $1.1 billion earnings increase from $854.1 million.

Uncover how Teradyne's forecasts yield a $369.53 fair value, a 3% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were assuming Teradyne would reach about US$3.7 billion of revenue and US$761 million of earnings by 2028, which is far more cautious than the consensus growth story tied to AI test demand, so if you are looking at this quarter’s strong results and fresh guidance, it is worth remembering that reasonable people can read the same numbers very differently and that these expectations may shift as the new information is absorbed.

Explore 8 other fair value estimates on Teradyne - why the stock might be worth less than half the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Teradyne research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Teradyne research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Teradyne's overall financial health at a glance.

Contemplating Other Strategies?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Invest in the nuclear renaissance through our list of 91 elite nuclear energy infrastructure plays powering the global AI revolution.

- AI is about to change healthcare. These 34 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.