Why Varonis Systems (VRNS) Is Up 13.2% After AI Deal, SaaS Outlook And Buybacks - And What's Next

Varonis Systems, Inc. VRNS | 22.53 | +3.63% |

- In recent days, Varonis Systems reported fourth-quarter and full-year 2025 results showing higher revenue year over year but wider losses, completed a US$14.99 million share repurchase of 448,000 shares announced in October 2025, and issued 2026 guidance pointing to continued SaaS ARR and revenue growth.

- At the same time, Varonis advanced its AI and SaaS ambitions by agreeing to acquire AllTrue.ai for US$125 million in cash, while facing securities class action lawsuits alleging earlier misstatements about the pace of its SaaS customer conversions.

- We’ll now examine how the AllTrue.ai acquisition and SaaS-focused guidance may reshape Varonis’ investment narrative around growth and risk.

This technology could replace computers: discover 23 stocks that are working to make quantum computing a reality.

Varonis Systems Investment Narrative Recap

To own Varonis, you need to believe its pivot to SaaS data security and AI-focused protection will eventually outweigh today’s widening losses and execution questions. Right now, the key near term catalyst is whether SaaS ARR keeps rising in line with 2026 guidance, while the biggest risk is that conversion challenges and legal overhang from the securities class actions further unsettle confidence in that transition. The latest results and AllTrue.ai deal directly touch both sides of this equation.

The most relevant update here is Varonis’ 2026 guidance, which calls for SaaS ARR of US$805.0 million to US$840.0 million and total revenue of US$722.0 million to US$730.0 million. This outlook frames how investors might view the AllTrue.ai acquisition: as an attempt to deepen AI related data security capabilities around that growing SaaS base at a time when reported losses are still widening and the market is watching conversion and churn metrics closely.

Yet against this push into AI and SaaS, investors should also be aware that...

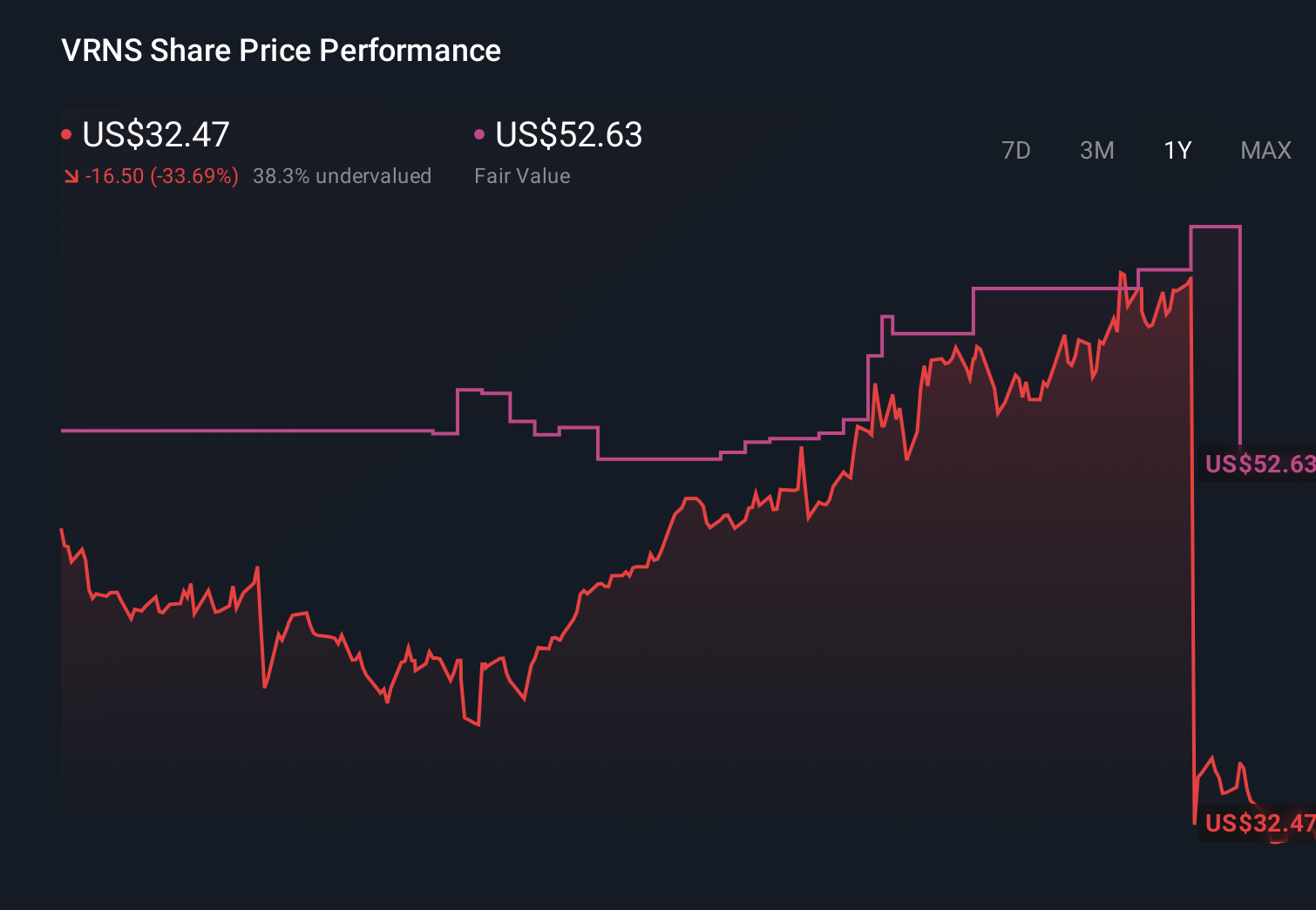

Varonis Systems' narrative projects $911.4 million revenue and $119.3 million earnings by 2028. This requires 15.3% yearly revenue growth and a $222.2 million earnings increase from $-102.9 million today.

Uncover how Varonis Systems' forecasts yield a $34.20 fair value, a 36% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were already cautious, penciling in about US$979 million of revenue and just US$32 million of earnings by 2029, and the latest AI acquisition plus SaaS guidance could either ease or reinforce that more pessimistic view depending on how you think the remaining on prem customers and new AI products will actually respond.

Explore 3 other fair value estimates on Varonis Systems - why the stock might be worth over 2x more than the current price!

Build Your Own Varonis Systems Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Varonis Systems research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Varonis Systems research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Varonis Systems' overall financial health at a glance.

Searching For A Fresh Perspective?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Uncover the next big thing with 27 elite penny stocks that balance risk and reward.

- Find 55 companies with promising cash flow potential yet trading below their fair value.

- Capitalize on the AI infrastructure supercycle with our selection of the 34 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.