Why Westlake (WLK) Is Up 5.4% After Analyst Upgrades And Polyethylene Supply Optimism – And What's Next

Westlake Corporation WLK | 119.53 119.60 | +0.11% +0.06% Pre |

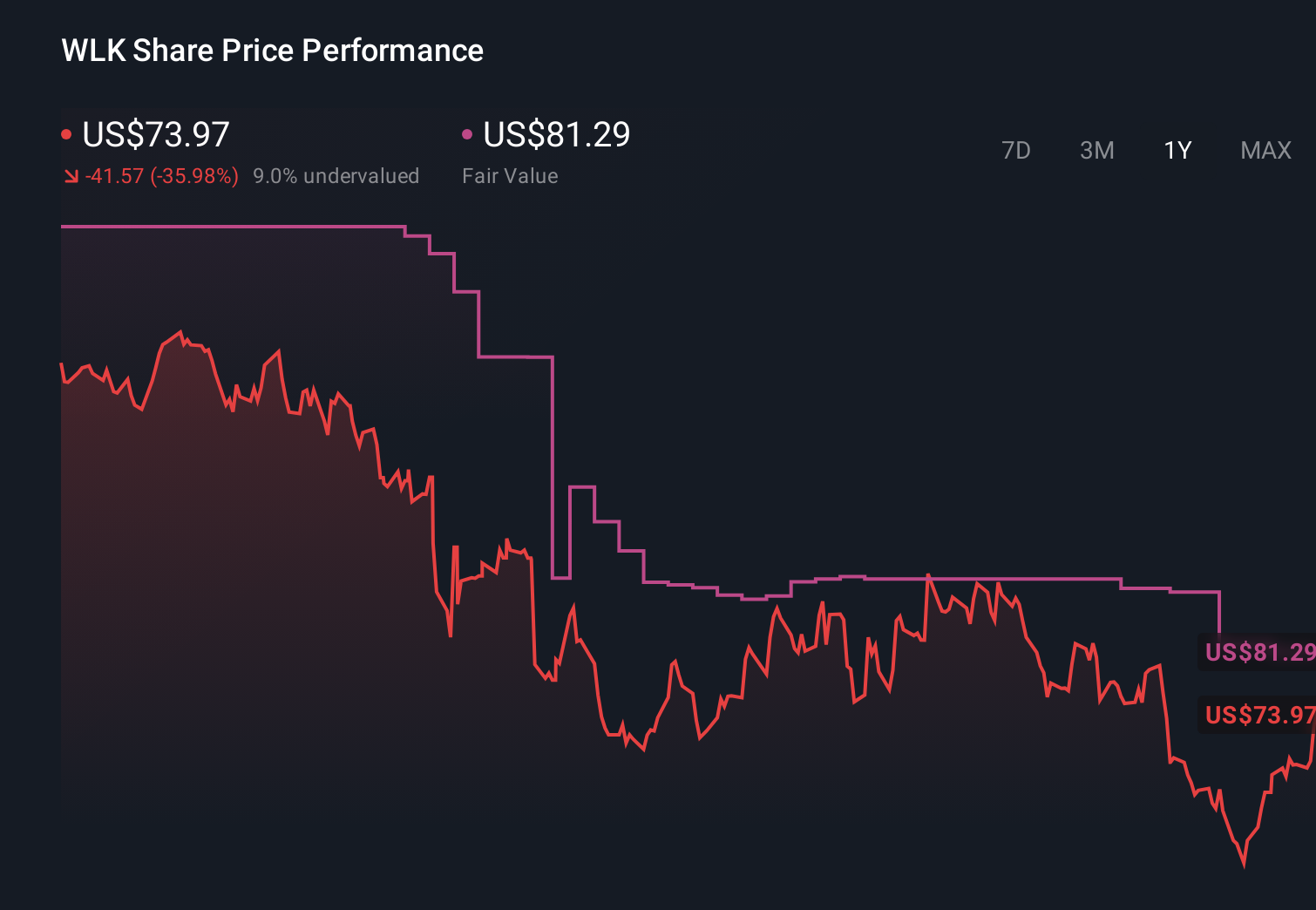

- In recent days, Westlake Corporation has attracted attention as analysts upgraded their views, technical indicators pointed to strong upward momentum, and an executive sold shares while the company worked through an earlier earnings miss and supply-side headwinds.

- Commentary from investors and asset managers has highlighted how favorable polyethylene supply conditions and a gradually recovering housing market could support Westlake’s performance across both its commodity and building-products businesses over time.

- We’ll now examine how this renewed analyst optimism around polyethylene supply dynamics could influence Westlake’s existing investment narrative and risk profile.

AI is about to change healthcare. These 36 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Westlake Investment Narrative Recap

To own Westlake today, you need to be comfortable with a cyclical chemicals and building-products company that is currently unprofitable but benefiting from strong share-price momentum and improving sentiment around polyethylene supply and housing. The key short term catalyst is whether tighter polyethylene supply and a firmer housing backdrop translate into better margins, while the biggest risk is that global overcapacity and cost inflation keep PEM profitability under pressure. Recent upgrades and price strength do not materially change those core dynamics.

The most relevant recent development is the post earnings analyst response. Despite a large Q4 2025 earnings miss and a full year net loss of about US$1.5 billion, several firms raised ratings and targets, citing favorable polyethylene supply conditions driven by global shutdowns. That optimism aligns directly with the current focus on supply tightening as a potential support for Westlake’s margins, even as the company continues to absorb the impact of weaker pricing and earlier supply side headwinds.

Yet behind the upbeat talk on polyethylene, investors should be aware that sustained global overcapacity in PEM products could still...

Westlake’s narrative projects $12.5 billion revenue and $364.4 million earnings by 2029. This requires 3.8% yearly revenue growth and an earnings increase of about $1.9 billion from -$1.5 billion today.

Uncover how Westlake's forecasts yield a $113.00 fair value, a 5% downside to its current price.

Exploring Other Perspectives

While the consensus narrative is cautious, the most optimistic analysts once projected revenue around US$13.3 billion and earnings near US$546 million, which contrasts sharply with the risk that a US$600 million earnings uplift from the 3 pillar plan may not fully materialize if global overcapacity lingers and could look different in light of the latest polyethylene focused news.

Explore 3 other fair value estimates on Westlake - why the stock might be worth as much as $113.00!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Westlake research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

- Our free Westlake research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Westlake's overall financial health at a glance.

Searching For A Fresh Perspective?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Capitalize on the AI infrastructure supercycle with our selection of the 36 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Uncover the next big thing with 33 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.