Why Williams Companies (WMB) Is Up 8.0% After Stronger 2025 Earnings And What’s Next

Williams Companies, Inc. WMB | 72.00 | +0.24% |

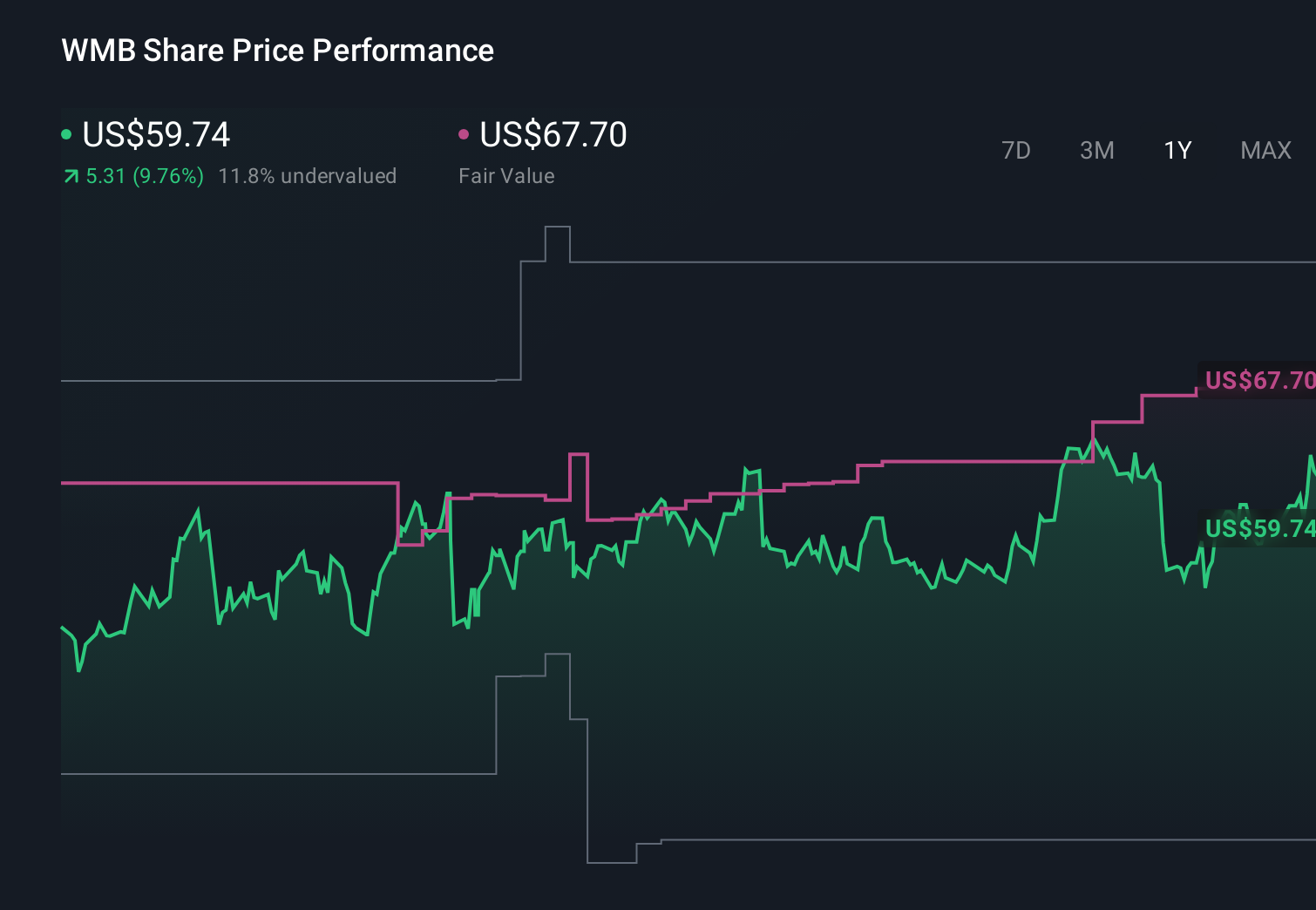

- In February 2026, The Williams Companies, Inc. reported full-year 2025 results showing revenue of US$11.95 billion and net income of US$2.62 billion, both higher than the prior year.

- The improvement in basic and diluted earnings per share from continuing operations to US$2.14 suggests stronger profitability across Williams’ core infrastructure business.

- Next, we’ll explore how this stronger earnings performance may influence Williams Companies’ investment narrative built around growth in gas infrastructure and LNG.

Invest in the nuclear renaissance through our list of 85 elite nuclear energy infrastructure plays powering the global AI revolution.

Williams Companies Investment Narrative Recap

To own Williams Companies, you need to believe that demand for its natural gas infrastructure and LNG-linked assets will stay resilient enough to support its heavy capital spending and debt. The stronger 2025 earnings confirm that existing assets are producing higher revenue and profits, but they do not materially change the near term balance between the key catalyst of gas infrastructure growth and the major risk from long term decarbonization and potential policy shifts.

Among recent developments, the 5% dividend increase to US$0.525 per share in January 2026 stands out alongside the 2025 earnings beat. Together, they suggest management’s confidence in cash flow from Williams’ expanding pipeline and LNG connected network, which many see as the core short term catalyst. At the same time, higher dividends and ongoing capital projects can heighten sensitivity to any future slowdown in natural gas demand or tougher permitting conditions.

Yet behind these stronger numbers, investors should also be aware of the growing risk that long term climate policy and electrification trends could...

Williams Companies' narrative projects $14.5 billion revenue and $3.3 billion earnings by 2028. This requires 8.6% yearly revenue growth and an earnings increase of about $0.9 billion from $2.4 billion today.

Uncover how Williams Companies' forecasts yield a $68.22 fair value, a 6% downside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were assuming revenues of about US$10.6 billion and earnings of roughly US$3.3 billion by 2028, which contrasts sharply with the cleaner energy execution risk you just read about and shows how differently you and others might interpret this latest earnings news.

Explore 6 other fair value estimates on Williams Companies - why the stock might be worth 21% less than the current price!

Build Your Own Williams Companies Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Williams Companies research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Williams Companies research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Williams Companies' overall financial health at a glance.

Searching For A Fresh Perspective?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Capitalize on the AI infrastructure supercycle with our selection of the 34 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- AI is about to change healthcare. These 25 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.