Will Analyst Optimism on Partnerships and Products Shift Worthington Enterprises' (WOR) Investment Story?

Worthington Enterprises, Inc. WOR | 52.50 | +0.69% |

- In recent weeks, analysts highlighted Worthington Enterprises as undervalued, citing expected revenue growth from partnerships and new product launches while warning about risks from trade uncertainty and steel price fluctuations.

- An interesting takeaway is that this positive analyst sentiment persists even as operational risks are expected to challenge the company’s margins and forecasts.

- We’ll explore how increased analyst optimism regarding new partnerships and product launches may reframe Worthington Enterprises’ investment narrative.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 25 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Worthington Enterprises Investment Narrative Recap

To own shares in Worthington Enterprises, an investor needs to believe in the company’s ability to capitalize on growth from new partnerships and product launches, despite persistent risks from trade uncertainty and steel price volatility. The latest news underscores continued optimism around these catalysts, but it does not meaningfully shift the immediate risk profile tied to margin pressures from fluctuating input costs.

Among recent company developments, the September quarterly report stands out, showcasing stronger year-over-year revenue and earnings. This earnings momentum highlights the potential financial impact of both new products and expanded distribution relationships, elements analysts cite as key positive drivers, though they are not immune to the ongoing margin headwinds facing the business.

However, investors should also keep in mind that, in contrast to the upbeat sentiment, exposure to steel price swings remains a factor that could...

Worthington Enterprises is projected to reach $1.4 billion in revenue and $213.4 million in earnings by 2028. This outlook is based on an expected annual revenue growth rate of 7.6% and represents a $117.3 million increase in earnings from the current level of $96.1 million.

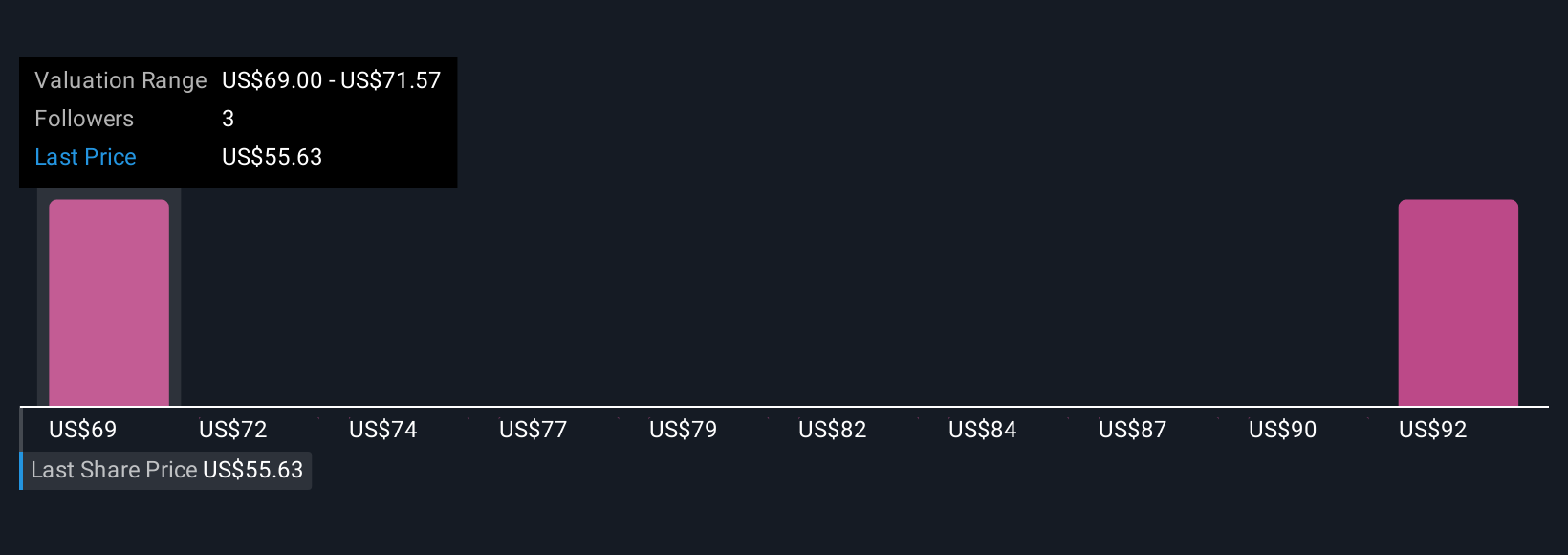

Uncover how Worthington Enterprises' forecasts yield a $69.00 fair value, a 26% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community members valued Worthington Enterprises between US$69 and US$91.87, reflecting widely varied return expectations from just two viewpoints. Even with this range, the company’s margin exposure from steel price shifts is an influential factor worth weighing as you compare these opinions.

Explore 2 other fair value estimates on Worthington Enterprises - why the stock might be worth just $69.00!

Build Your Own Worthington Enterprises Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Worthington Enterprises research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Worthington Enterprises research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Worthington Enterprises' overall financial health at a glance.

Want Some Alternatives?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.